One of the reasons that investor sentiment is currently on the floor, and it is on the floor, is simply that both of the main asset classes, bonds and equities, which investors use to construct portfolios are down for the year.

Performance of stocks and bonds in 2022

Source: FE Analytics. Total return in sterling between 1 Jan and 31 Jul 2022

Bonds tend to go up when equities fall, and vice versa. That is portfolio construction 101. When people are fearful about the future and do not want to take on risk through holding company stocks, demand for the relative safety of a fixed income increases. This is usually the case, but the fly in the ointment this year has been inflation.

If rising inflation has not historically been great for stocks, then it has been a disaster for bonds. Particularly when the starting income offered by bonds is basically non-existent, as was the case this time last year.

In 2021, we mainly had inflation in the cost of stuff – cars, garden furniture, fridges. This year, it is inflation in the cost of fun as we all emerge back into the wild after lockdown.

This inflation ravages the real value of a loan to the UK government which pays you a flat annual 0.5%, as a ten-year gilt did this time last year. That is miles behind the current inflation rate of around 9%, so it is only natural that investors need a higher return to try and get closer to the current rate of inflation – in which case the price of the bond falls.

The end of the first half of the year brings a natural opportunity to rebalance portfolios - but if the two main components of your asset allocation are down for the year, then what do you buy?

Commodities have been the standout performer year to date – should we be looking to alternatives in the current climate? I have certainly had more emails recently from fund houses landing in my inbox decrying the death of the classic ‘60/40’ equity/bond portfolio than I have in previous years.

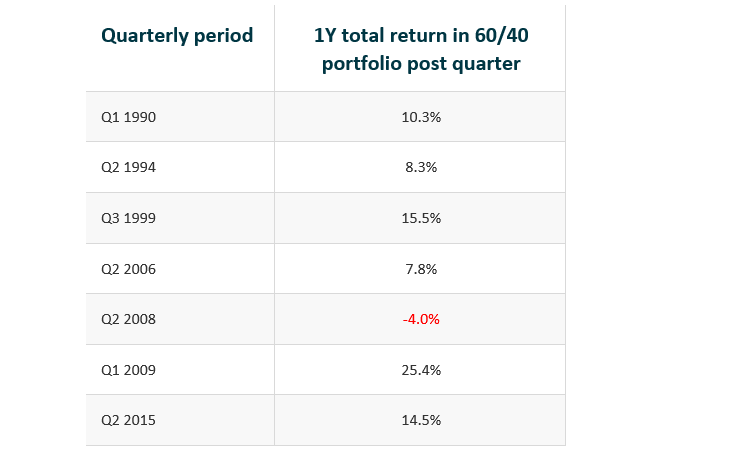

But if we look at the historical numbers, maybe the grim reaper should hold onto his horses.

Going back to 1986 we looked at quarterly returns for stocks (MSCI World, the global stock market) and bonds (gilts, loans to the UK government). While over longer periods bonds and stocks tended to move in different ways, there were nine quarters when the prices of both bonds and stocks fell in tandem. It has only happened once since 1986 in consecutive quarters - Q1 and Q2 2022. Breakdowns in diversification, like we have seen this year, are rare.

We then looked at 12-month forward returns for a 60/40 asset allocation following quarters where stocks and bonds fell together. As you can see from the below, returns were pretty healthy.

Source: Quilter Cheviot. Returns are shown for a 60% MSCI World/40% iBoxx Gilt portfolio

One of the benefits of having a disciplined approach to investing is that, in theory, it leaves you less predisposed to following narrative. Increasing enthusiasm about whatever asset class or sector is working at a given point in time means that it can feel like it is going to work forever.

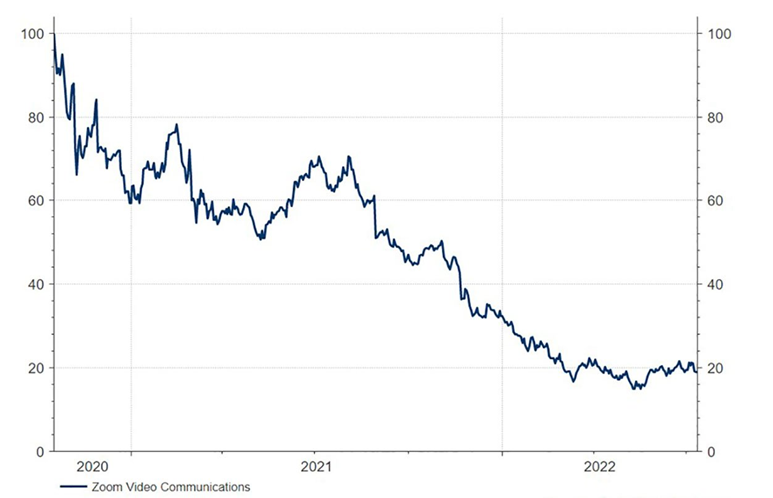

Remember when we all thought that no one was going to have a meeting in person ever again?

Performance of Zoom Video Communications

Source: Quilter Cheviot, Refinitiv Datastream

This is not to pick on Zoom or say that they are not a good company – but to observe that human nature, every time, is to get too excited about something that is working on the way up, and too despondent on its prospects on the way down.

The whole point of setting out your investment process in advance is to have some rules in place to rebalance your portfolio when it can feel uncomfortable to do so – history tells us that this is often the right approach to take.

David Henry is an investment manager at Quilter Cheviot. The views expressed above should not be taken as investment advice.