Chinese equities have been through difficult years with a crisis in the property sector, regulatory crackdowns in several sectors of the economy and increased geopolitical tensions.

Combined with a multi-year Covid lockdown, they have fallen out of favour with global investors and some do not want to go anywhere near them.

For instance, Brunner Investment Trust does not have any direct exposure to Chinese equities, with senior portfolio manager Julian Bishop saying it is unlikely to change in the future.

He said: “Equities is the longest duration asset you can buy because you're theoretically getting a cash flow stream in perpetuity. The rule of law in the country where you invest, the institutional framework and accounting audit standards are all absolutely vital.

“I find it tough to think that we would be directly involved in the Chinese market, simply because there have been repeated examples of regulation being retrospectively changed. Those sudden changes in the law have completely decimated stock market values.”

JPMorgan Global Growth & Income also has no direct exposure to China. Manager Amit Parmar explained that the potential reward does not outweigh the risks.

Scottish Mortgage has also become more cautious with Chinese equities, although they have long been a feature of Baillie Gifford’s flagship investment trust and remain the second largest country allocation in the portfolio.

The trust’s deputy manager Lawrence Burns admitted that he has been slow to recognise the geopolitical tension between the US and Chinas as well as the changes in the domestic regulatory environment.

But instead of completely divesting from China, Scottish Mortgage has been raising the bar for its Chinese investments.

Burns said: “It doesn't mean we do not invest in anything in China, but we must make sure we are sufficiently compensated for those geopolitical risks. We aim for Chinese companies that are truly swinging for the fences.”

The Global Smaller Companies Trust has also chosen not to shun Chinese equities as it is exposed to them via third-party funds. Yet manager Peter Ewins stressed that he ensured the underlying managers invest in specific types of Chinese companies.

He said: “Because there's a lot of pressure for American companies to bring their production out of China, the people that manage those funds for us are focusing on Chinese companies supplying China and not companies supplying the US out of China.”

There are, however, different ways to access the Chinese market without holding any direct exposure in the country.

JPMorgan Global Growth & Income does so via companies in developed markets with a strong exposure to China such as LVMH or Schneider Electric.

Carlos Hardenberg, manager of the Mobius Investment Trust, suggested gaining exposure to China through Korean companies.

He said: “The Chinese are obsessed with Korean brands, technology, food, music, etc. They love everything that comes from Korea. You also get less risk as well as better governance and transparency than with Chinese companies.”

Some of the managers also stressed that China risks apply to Taiwan with fears that a war may break out between the two entities.

For instance, Hardenberg said that he has started to reduce the allocation to Taiwan in his portfolio, which remains nonetheless the trust’s largest country weighting.

He is not the only professional investor that have been divesting from Taiwan in recent times. Earlier this year, Berkshire Hathaway’s Warren Buffett went a step further by selling out his holdings in Taiwan Semiconductor Manufacturing Company (TSMC), citing geopolitical risks as the reason.

Yet, Brunner’s Bishop said it is impossible to completely eliminate China risks from a portfolio, using Apple as an example.

He said: “Every single Apple product uses chips made by TSMC in Taiwan and pretty much all of their goods are manufactured in China. Apple cannot operate without Taiwan and China and that's the same for pretty much every company in the world.”

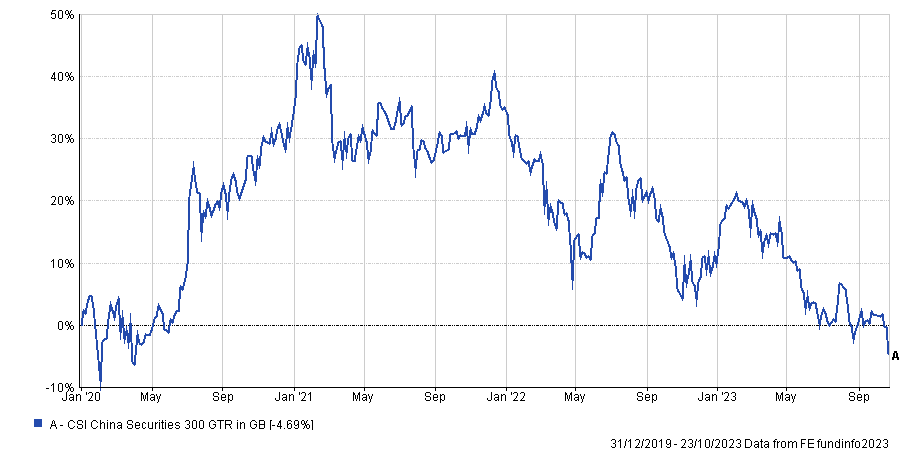

Unlike global equity managers, Asian equity managers feel more comfortable with China and have been adding to Chinese equities, which have recently fallen to their pre-pandemic level.

Performance of index since 1 January 2020

Source: FE Analytics

Ian Hargreaves, co-manager of Invesco Asia, said that this derating is justified and that China is likely to grow at a slower pace going forward.

Yet, after a disappointing recovery after the post-lockdown reopening of the country, the emphasis has increasingly been on structural rather than cyclical factors, which Hargreaves finds healthier. As a result, the trust has moved back into Chinese and Hong Kong equities.

Abrdn Asia Focus has also been adding to Chinese equities, with co-manager Gabriel Sacks citing the “extremely” attractive valuations in China, although the trust remains skewed towards India and Southeast Asia.

However, for Brunner’s Bishop, attractive valuations are not enough. He concluded: “A lot of people invested in Russia on valuation grounds, but it didn't prove to be such a good idea.”