The global economy has shifted into a new regime: interest rates and inflation will be higher going forward than since the financial crisis and growth will be more muted while volatility, uncertainty and dispersion have all increased.

This is the view of the BlackRock Investment Institute’s global chief investment strategist Wei Li, who said instead of waiting on the sidelines in cash, investors should make the most of the new regime.

“The macroeconomic environment is a lemon and we need to make lemonade instead of waiting for the lemon to go back to being a melon,” she said.

Piling into aggressive strategies could be too risky for some, while taking an ultra-defensive approach risks missing out on some strong gains. Against that backdrop, Trustnet asked fund selectors to suggest strategies for medium risk investors.

A core allocation to global bonds alongside US and UK equities

Charles Younes, deputy chief investment officer at FE Investments, suggested that medium-risk investors allocate to a global strategic bond fund paired with US and UK equity portfolios.

The US Federal Reserve is likely to start cutting rates next year but there is a gap between what policymakers are saying and what the bond market has priced in. Younes expects global strategic bond funds to exploit that disparity to generate alpha.

John Pattullo and Jenna Barnard, who manage the £2.7bn Janus Henderson Strategic Bond fund, proved they are able to do that this year, he said.

“The beauty of a global bond mandate is you can play between regional differences. The UK and Europe are probably closer to a hard landing than the US, and Japan is in a different part of the cycle,” Younes said.

He also thinks US equities should be a core part of medium-risk portfolios. “It’s really hard to bet against US equities,” he said, given that the US has led global equity markets in eight of the past 10 years.

The $4.8bn Brown Advisory US Sustainable Growth fund has a bias towards small- and mid-caps, which tend to lead in a recovery rally.

Sustainable investing has had a tough couple of years but if rates are cut, the discount rate will be lowered for high growth names that feature in a lot of sustainable funds, which should give them a share price boost, Younes said.

Meanwhile, Evenlode Income is a quality-growth strategy and “a bond proxy”, Younes continued. “It’s your sleep well at night allocation.”

The £3.1bn fund invests in multi-national companies with high free cash flows that can protect their revenues in a recession and defend their competitive advantages and high barriers to entry.

Multi-asset funds

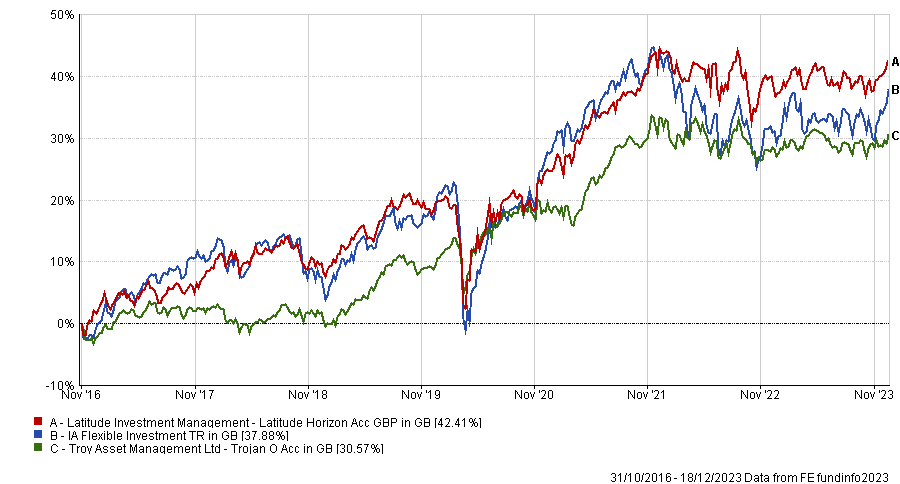

Edward Allen, private client investment director at Tyndall Investment Management, suggested two defensive multi-asset funds – Troy Trojan and Latitude Horizon.

“I’m an investor in Sebastian Lyon’s Trojan fund because he and his team have an excellent record of defensiveness in adverse markets. This has, historically, given them the dry powder to buy when other investors are running for the hills, to the benefit of their shareholders,” he said.

“Troy invests in bonds, equities, gold and cash, and does not get involved in the fancier (and more expensive) hedge side of investing beyond occasionally hedging currencies.”

Latitude Horizon is run by Freddie Lait, who invests about half the portfolio into quality-value stocks and the remainder into other assets, usually bonds, cash and gold.

“The asset allocation choice is not overly finessed, usually hovering around that 50% mark, but it provides a much more stable risk/returns structure than either outright equities or a pure alternatives fund,” Allen said.

“The non-equity side of the portfolio is selected with the aim of balancing the fundamental risks in the equity portfolio, where possible and potentially profitable to do so.”

Performance of funds vs sector over 10yrs

Source: FE Analytics

Capitalising on attractive valuations in small-caps

Daniel Lockyer, senior fund manager at Hawksmoor Fund Managers, opted for UK and Japanese small-caps with the Aberforth Smaller Companies Trust and the M&G Japan Smaller Companies fund.

“While the UK market overall trades on a price to earnings (P/E) ratio of 10x, representing one of the cheapest levels in history outside of crises, Aberforth’s portfolio trades on around 7x, a level that has only been cheaper twice since it launched in 1990: during the global financial crisis and Covid,” Lockyer said.

“Meanwhile, the quality of the portfolio is very strong, with balance sheets in the best shape since 2014 with 40% of the portfolio sitting on net cash, average dividend cover of 3.4x and an overall portfolio yield of 4%, which is 29% higher than its historic average.”

M&G Japan Smaller Companies is managed by Carl Vine and is “well placed to capture the long-term recovery of the Japanese market that has been in the doldrums for decades,” Lockyer said.

“Valuations are cheap and the yen is undervalued – with any appreciation, likely caused by the Bank of Japan responding to inflation by raising interest rates, boosting returns for sterling investors.”

A large, liquid global equity trust

Emma Bird, head of investment trusts research at Winterflood Securities, chose the £2bn JPMorgan Global Growth & Income trust – a “large, liquid, low-cost vehicle” with an ongoing charges ratio of just 0.5%.

It has been managed by FE fundinfo Alpha Manager Helge Skibeli since 2019 together with co-managers Rajesh Tana and Timothy Woodhouse. Since then, it has outperformed the MSCI AC World Index in each calendar year on both a NAV and share price total return basis.

“This degree of consistency is commendable, particularly over a period that has seen a range of market and macroeconomic conditions,” Bird said. “We believe that the disciplined application of the managers’ style-agnostic, research-driven investment approach has been a key driver of the consistency of performance, and we would expect this to continue.”

Performance of fund vs sector and benchmark over 5yrs

Source: FE Analytics

“The enhanced dividend policy, which targets an annual payment of at least 4% of the previous year-end NAV, makes good use of the investment trust structure, and the fund currently provides an historical yield of 3.6%,” Bird added.

Specialist investment trusts trading at a discount

A final option for balanced investors is to pick slightly more risky strategies at big discounts, as this should bake in some protection.

With a host of investment trusts available at wide discounts, Charlotte Cuthbertson, co-manager of the MIGO Opportunities Trust, tipped Atrato Onsite Energy and JPMorgan India.

“With companies needing to hit net-zero targets, Atrato has an interesting proposition of providing corporates with solar panels on the roofs of their industrial sites and selling the power generated to help meet corporate energy needs,” Cuthbertson said.

“It sits on a wide discount despite future output already being contracted, so investors can feel more confident about future inflation-linked revenues than many in their peer group.”

Meanwhile, JPMorgan India offers exposure to a booming economy and stock market. Alpha Manager Amit Mehta took the helm in September 2022 and is supported by co-managers Sandip Patodia and Ayaz Ebrahim.

“JPMorgan India should benefit from a new management team after lagging their peers over the past several years and still trades at a wider discount than the sector average,” Cuthbertson said.

“The shares are cheaper than they look because, unless the trust performs extremely strongly, shareholders will have the right to tender a quarter of their holding at net asset value, whereas the shares currently trade at a 17.5% discount.”