Corporate bond yields could be nearing their peak and investors should act swiftly, according to Lesley Dunn, manager of the Baillie Gifford Strategic Bond fund.

Yields have increased substantially this year as rampant inflation and rising interest rates squeeze companies’ balance sheets, adding a higher degree of risk for those lending to them.

Current yields are higher than their historical average, presenting an appealing entry point for new investors, but this window could be closing soon, according to Dunn.

She said: “We're not calling peak inflation or the peak in rates, but we do think we're close to the top of where yields can get to.”

Tighter monetary policy around the world has presented significant challenges to many businesses, but Dunn said central banks have completed much of this now, suggesting yields could begin to unravel once interest rates come down.

“I think it’s fair to say that central banks have had a very tough job,” she added. “They have moved very decisively with the pace of the inflation, but now we're at that tipping point where there's a real risk to the growth outlook.

“We think that we could be at the stage where central banks will struggle to push any further than this.”

This is because manufacturing purchasing managers indices (PMIs), which measure the direction of economic trends, are “showing some weaknesses” that could signify the start of an economic slowdown.

Employment in labour markets and services PMIs appear resilient, but Dunn said that manufacturing is “the leading indicator of where GDP is going”. Therefore, central banks could begin easing their monetary policies to protect GDP growth in their respective regions.

For the time being, corporate bonds are offering an attractive yield for those looking to invest before rates come back down.

Dunn said that this is the “first time in a long time that we’ve been in any way enthused or excited” about the corporate bond market, which has typically delivered lower, but more reliable returns.

She added: “When you're looking at a market that's offering a 7% yield, then what you're really looking at is equity-like returns with much lower volatility.

“We're looking at the potential for capital appreciation for bonds which just hasn't been around for quite some time.”

Indeed, yields have risen because the level of risk has increased, but Dunn said that markets are overestimating the danger of investing in the current climate.

“The market is pricing in more defaults than we think will actually transpire, so that's a really interesting valuation opportunity,” she said.

However, all corporate bonds, including those that are genuinely high-risk, have had similar yield hikes, meaning investors should still be observant about where they’re allocating.

Dunn said: “The scale of the sell-off we saw in spreads is unprecedented – spreads have tripled this year in all major corporate bond densities in the space of seven-to-nine months, and when that happens there's no differentiation between good companies and bad companies.”

One area that Dunn has increased exposure to is financials, which she expects will benefit from high interest rates.

For example, investors have factored in more risk in Santander’s bonds by selling and increasing the yield to 8.5% despite the firm being “a bank that has always delivered operationally and delivered good profitability over a very long-term timeframe”.

Likewise, Dunn said that other financials such as Barclays, JPMorgan and NatWest are all yielding above 6% despite being resilient businesses.

Matthew Russell, manager of the M&G UK Inflation Linked Corporate Bond fund, agreed that market volatility has led to attractively high corporate bond yields.

He said: “Credit spreads versus gilts are historically wide and at an attractive entry point. In the past 10 years they have only been wider during the Covid sell off.”

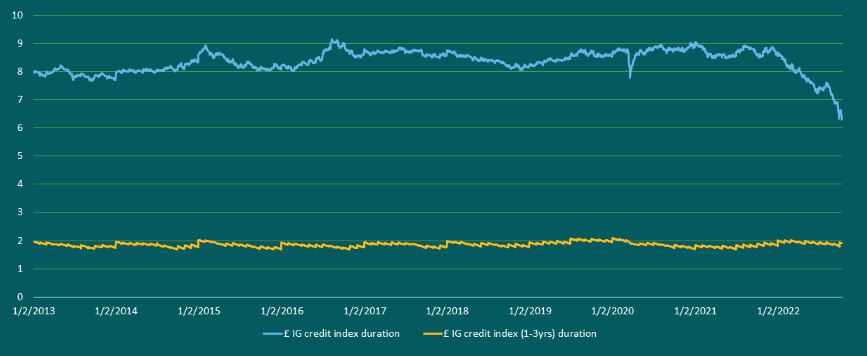

Credit spreads over the past decade

Source: M&G Investments

However, investors will have to decide on whether they want to invest in short- or long-dated bonds depending on their outlook, according to Russell.

He said that investors who expect yields to drop should buy long-dated bonds, while those anticipating higher yields should go for short-dated ones.

“Longer-dated credit is looking much better value if you think yields are likely to fall,” Russell added. “Their greater convexity – the degree to which a bond’s sensitivity to yield changes, given a change in yield – makes a compelling investment case.”

Long vs short dated credit over the past decade

Source: M&G Investments