Most investment trust shares trade on a discount, making it difficult to find the rationale in paying over the odds for an investment company sat at a premium. But there are a few reasons why, according to experts, and a few good options too.

On a simple level, investment trust discounts can be seen as a function of supply and demand – the same as price for anything else.

A premium or discount represents the difference between the estimated underlying value of the fund’s shares (the net asset value, or NAV) versus the price each share is trading at.

If that difference stays constant, the underlying NAV total return will be fully passed through in the returns that shareholders will see, Shavar Halberstadt, equity research analyst at Winterflood, explained.

“For a trust on a premium, issuing additional shares will be accretive on a NAV per share basis, while for a trust on a discount, buying back shares will be NAV accretive. Either way, the key consideration is whether you think the premium or discount rating is sustainable over time,” he said.

“Buying a trust on a significant discount can see investors reap the dual benefit of underlying performance plus discount reduction over time as the market re-assesses its rating, whereas buying a trust on a significant premium could see underlying performance (partially) offset by a falling premium if the market deems that the trust has not met its expectations.”

So investors need to weigh up buying trusts on a premium, which tend to be priced based on strong performance, versus picking up value opportunities on big discounts.

In total, there are 23 trusts whose shares trade above their NAV. Below experts highlight three worth considering.

There are times when even very valuation-conscious investors might want to make exceptions, according to Robert Fullerton, senior research analyst at Hawksmoor Investment Management.

One of such exceptions could be Odyssean, which offers a “specialised, proven track record” for a trust that is deliberately keeping the its assets under management down to suit the strategy.

It is a £214.9m strategy with an FE fundinfo Crown rating of five and was the second-best performer in the IT UK Smaller Companies sector over the past five years.

It currently trades on a small premium because “it is quite small and has a sticky long-term shareholder register”, Fullerton explained.

Performance of fund against sector over 1yr

Source: FE Analytics

“They are a small team and are not chasing or gathering assets and the investment trust structure suits the strategy very well,” he said.

“We are very conscious of value, but there are times when you might make exceptions and take a long-term view of NAV performance and the team. On top of that, Odyssean’s is not a very wide premium and it offers regular tenders as well, which support the share price.”

Halberstadt and his team are also recommending Odyssean* based on its “successful private-equity investment approach to listed companies and because it’s “a clear beneficiary of takeover interest for UK smaller companies”.

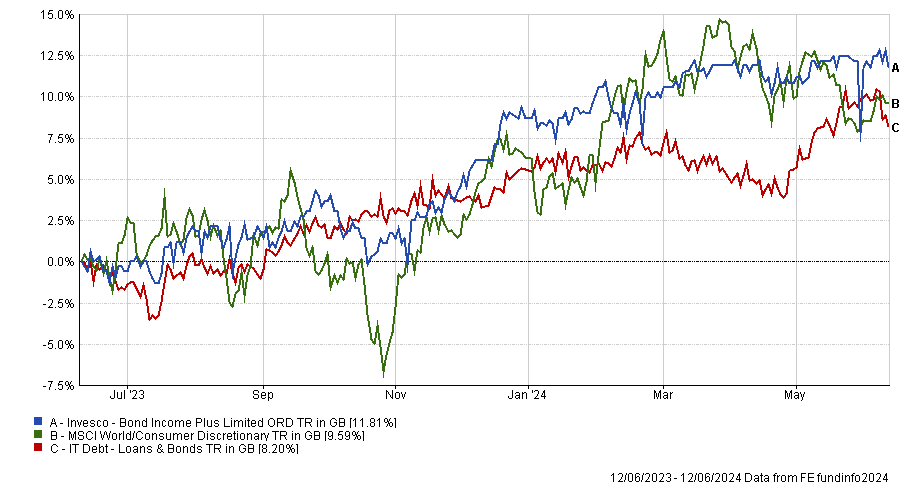

But they also highlighted Invesco Bond Income Plus*, a £330.9m strategy led by Rhys Davies, who aims to obtain both high income and capital growth by investing predominantly in high-yielding fixed-interest securities.

Performance of fund against sector and index over 1yr

Source: FE Analytics

“The trust is a potential beneficiary of a prospective downward interest rate trajectory, given its fixed rate debt exposure and careful management of credit risk,” Halberstadt said.

“Its premium rating reflects investor demand for its dividend yield, which has consistently increased over recent years, exceeds government bond rates and is based on a more selective portfolio than a passive high-yield bond index.”

Finally, Quilter Chieviot’s head of investment fund research Nick Wood said that even if two trusts trade at very different discount levels, the starting point from an investment perspective is whether the underlying investment adviser has the ability to outperform their stated objective.

“The discount and premium will come into the equation, but it is certainly not the be all and end all as some discounts are justified, just like some premiums are likewise there for a reason,” he added.

“Of the funds currently on a premium, none are positively rated by the Quilter Cheviot team at present, except 3i Infrastructure.”

Performance of fund against sector and index over 1yr

Source: FE Analytics

This £2.9bn vehicle is co-managed by Scott Moseley and Bernardo Sottomayor, whose aim is to provide a total return of 8% to 10% per annum with a progressive annual dividend per share.

Their primary focus is to acquire mid-market controlling majorities or significant minority positions and strong governance rights in infrastructure companies.

Currently, the portfolio is made up of 12 names – four in the energy transition sector, three in digitalisation and two in essential infrastructure renewal, while the remaining two are exposed to the demographic change megatrend and other critical infrastructure opportunities.

*Denotes a corporate client of Winterflood Securities