The Ruffer Investment Company has shifted its defensive positioning towards credit spread protection and yen exposure, warning that the asset class correlations investors have relied on for decades are no longer reliable.

Jasmine Yeo, co-manager of the trust, said the changes reflect a world where "the asset class correlations that investors have been able to rely on for a really long period of time are not as reliable when we think about the future”.

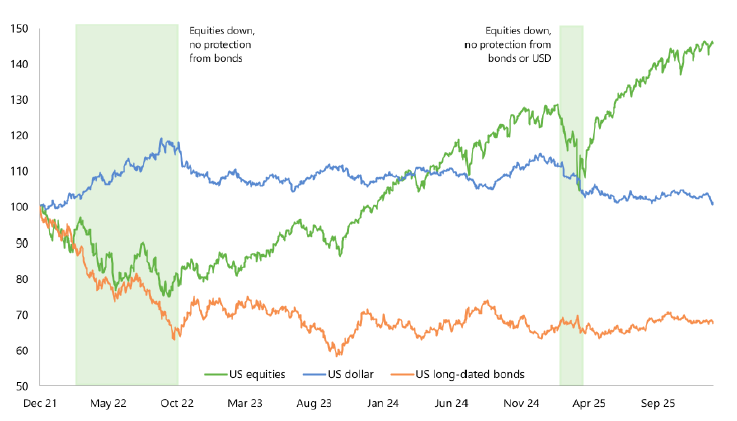

The breakdown became visible in 2022, when bonds failed to protect against equity losses, and again in April last year when US equities, the dollar and bonds all fell together. That triple decline marked a turning point. Over the previous 15 years, every double-digit fall in the S&P 500 had been accompanied by dollar strength – except in April 2025.

US bonds and dollars fell with stocks during recent market stress

Source: Ruffer

“That's another warning shot for investors, perhaps for those that didn't heed that warning in 2022,” she said. “The world is changing, volatility is rising and, as a result, asset class correlations will shift. That will force investors to reappraise diversification in their portfolios.”

The trust's response has been to look beyond conventional assets. It now holds significant positions in credit spread protection (a type of corporate bond insurance) and Japanese yen exposure, both of which the managers believe offer better risk-reward than traditional defences.

Credit spread protection has historically risen when equities fall over a reasonable period, Yeo noted. But the case has strengthened recently because the asset sits at the centre of two market risks: private credit and AI capital expenditure.

Corporate bond market insurance offering protection

Source: Ruffer

“A lot of these companies have been funded by private credit in recent years and are very AI exposed,” she said. “Some of these private credit investors are now hedging portfolios with this liquid type of credit protection. This type of protection is very exposed to a worsening or deterioration in that private credit story.”

As for the yen, it has historically acted as a safe haven during market dislocations because Japanese investors repatriate foreign assets and unwind carry trades. That dynamic played out during the financial crisis and again in August 2024. Yeo argued the risk remains acute today because Japanese investors hold vast foreign asset positions, primarily in US equities and credit markets.

Japan's net international investment position is close to 100% of GDP, she noted, making any reversal significant.

Co-manager Ian Rees added that the trust's shift away from US equities is based on valuation. US equities are expensive by their own historical standards, whether measured including or excluding the Magnificent Seven, and such starting valuations have historically locked in poor returns. “History doesn't look good for US equities today,” he said.

Instead, the trust is fishing in cheaper markets with strong fundamental stories. Japan is one example, with the trust holding more than 5% in Japanese equities.

“We are looking to exploit the ongoing improvements in corporate governance and shareholder friendliness across Japan,” he said. “This is not something that's starting from fresh today. It's been going on for the best part of a decade but valuations are still very attractive.”

The other contrarian tilt is towards UK equities, particularly domestically exposed businesses that could benefit from a pick-up in economic activity. Rees pointed to housebuilders, which trade below net asset value (NAV) and have solid balance sheets, as well as adjacent businesses such as Howden Joinery.

“Fundamentally, this country needs to build a lot more housing,” he said. “So if you can get rates coming down and affordability improving, we think that is a very attractive area.”

The UK household and corporate sector has largely deleveraged over the past decade, Rees noted, creating a set-up where demand – illustrated by private sector borrowing – could pick up as the rate-cutting cycle progresses.

“These are businesses operating in quite lean times. They just need volume to pick up.”

Roughly a third of the trust's portfolio is held in equities, split between bottom-up ideas grouped by geography and top-down macro-driven positions. From a bottom-up perspective, the trust holds more in Europe and the UK than in the US, a sharp contrast to a global equity tracker, where around 65% is typically in US equities.

Yeo stressed that the trust's flexibility is central to its approach. It has used a range of unconventional protections in recent years, including VIX index call options ahead of the pandemic in 2020, interest rate options through the rising rate environment of 2022 and index put options in 2024.

“Exactly what you'll own in the company will vary over time based on the risks we see and the best value opportunities that we can find,” she said. “That is a really important skill for investors, and perhaps crucially, one that passive strategies or quantitative strategies don't have access to.”