Credit markets are entering a more nuanced phase. While spreads remain relatively tight by historical standards, yields have moved higher, providing a more supportive starting point for returns. This reflects both higher underlying rates and some repricing of risk.

Valuations are therefore less stretched than they were at the start of the year but not compelling enough to rely on carry alone.

More importantly, the market environment is shifting. After an extended period of unusually low volatility, markets are beginning to exhibit more frequent and pronounced swings.

Macro uncertainty, evolving central bank expectations and geopolitical developments are contributing to a more dynamic backdrop, marking a move away from stable, one-directional conditions.

Equity markets, while still resilient, may also become more sensitive to changing expectations, with greater divergence emerging beneath the surface.

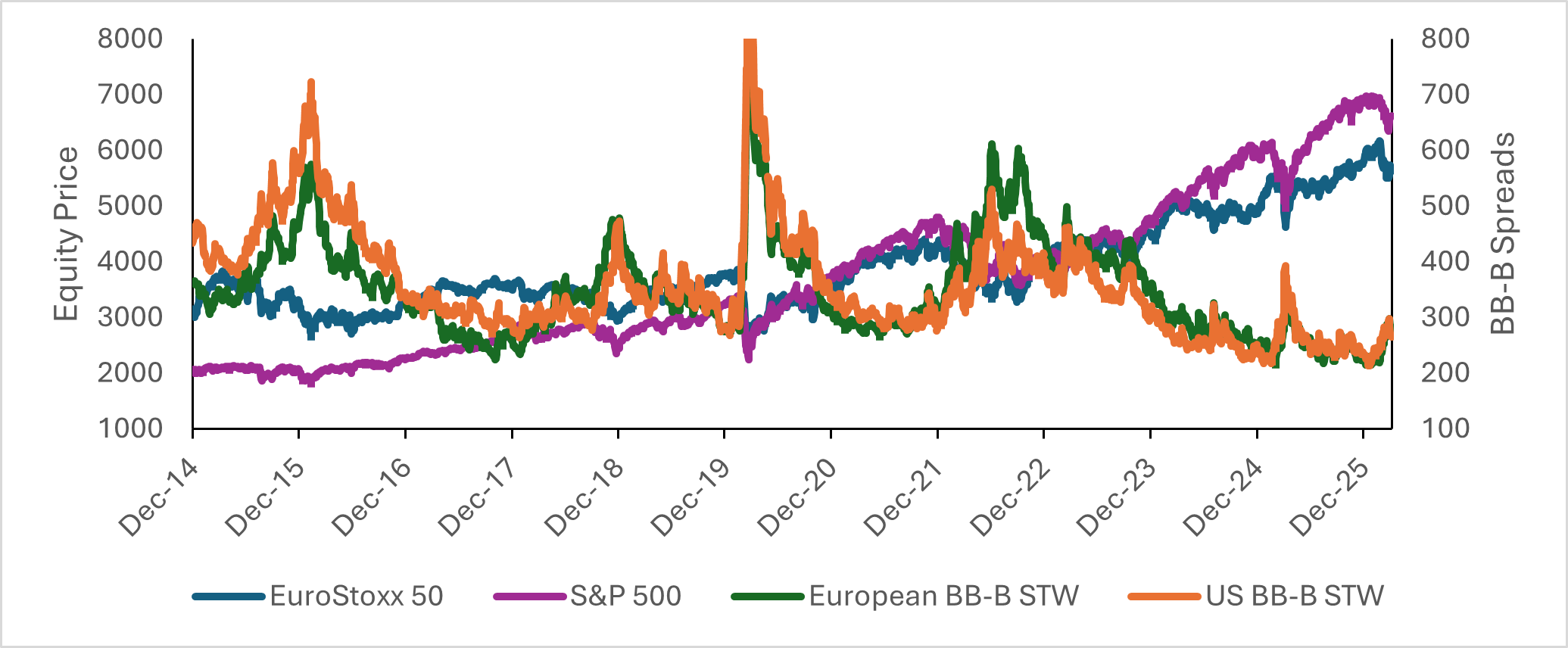

Equity prices & credit spreads

Source: Bloomberg data as of 7th April 2026. ICE BofA BB-B US High Yield Constrained Index (HUC4), ICE BofA BB-B Euro High Yield Constrained Index (HEC4). S&P 500 Index and EuroStoxx 50 Index. Indices selected by Muzinich as best available proxies for the respective asset classes.

For investors, this shift changes where returns can be generated. In low-volatility environments, credit returns are largely driven by carry, with limited differentiation across issuers and sectors.

As volatility rises, pricing becomes more dispersed, creating both risks and opportunities. A similar pattern is emerging in equities, where index stability can mask increasing divergence at the stock and sector level.

A traditional long-only approach remains inherently dependent on market direction. Even with higher yields, investors remain exposed to shifts in sentiment and potential spread widening.

While carry provides some cushion, it may be insufficient in a more volatile environment. The key question is therefore not just whether yields are attractive, but whether returns are resilient to changing conditions.

A credit market-neutral approach offers an alternative by shifting the focus from market direction to relative value. By constructing portfolios of paired long and short positions, returns are driven by changes in relative pricing rather than overall market moves.

As volatility rises, dispersion increases and pricing becomes less uniform, creating dislocations between similar credits, sectors and regions.

These inefficiencies, often driven by technical factors or investor flows, are difficult to exploit in long-only portfolios but sit at the core of market-neutral strategies.

The current rate environment further supports this approach. With cash rates no longer near zero, market-neutral strategies can generate a natural carry component broadly aligned with risk-free rates, before any additional alpha from relative value trades.

These strategies draw on multiple return sources. Basis trades exploit discrepancies between cash bonds and derivatives, relative value trades capture differences across similar credits or regions, and intra-capital structure trades seek inconsistencies within an issuer’s debt stack. All tend to benefit from periods of higher volatility and dispersion.

Market neutral does not mean risk-free, but risk is managed differently. Portfolios are built from many smaller positions, reducing reliance on any single outcome, while leverage is used to balance exposures rather than to take directional bets.

The result is typically lower volatility and shallower drawdowns than long-only credit, while still benefiting from positive carry.

For investors, this has clear implications. Market-neutral credit is not a replacement for long-only exposure, but a complement, providing a return stream driven by pricing inefficiencies rather than market direction and helping to diversify portfolios alongside traditional credit and equity allocations.

Jamie Cane is a portfolio manager at Muzinich & Co. The views expressed above should not be taken as investment advice.