The returns made from investing in emerging markets have largely been a byproduct of whether the US dollar is strengthening or weakening, according to James Syme, manager of the JOHCM Global Emerging Markets Opportunities fund, who said this one factor dictates investors’ experience of the asset class more than anything else.

“If you look at the longer term, you make almost all your money in emerging markets during weak-dollar periods,” he said.

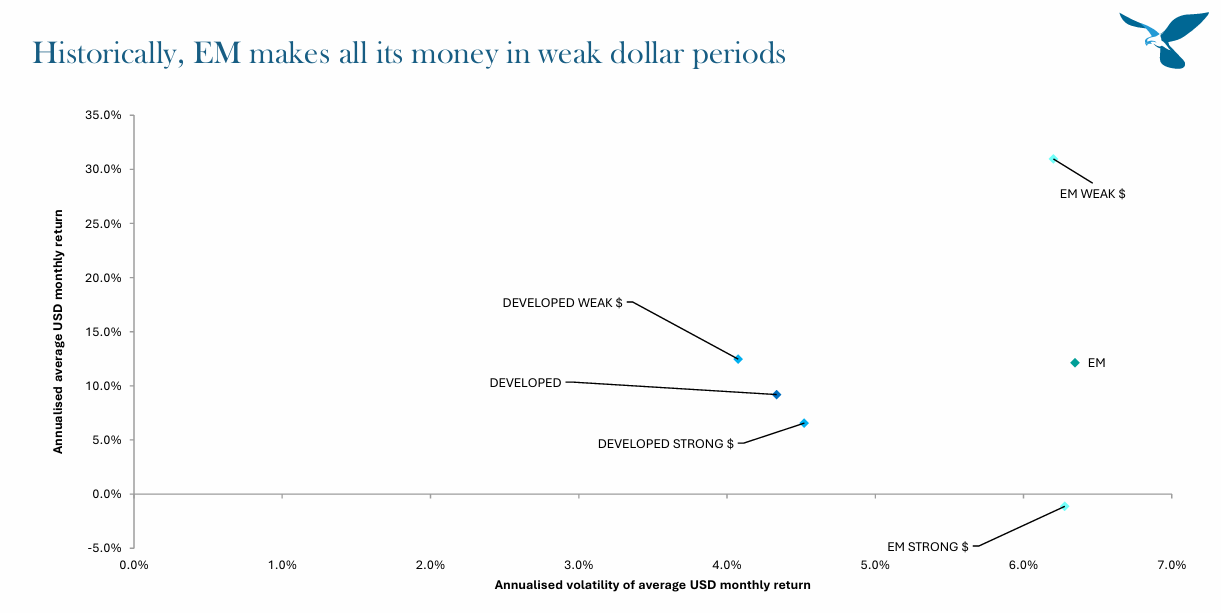

In fact, in strong-dollar environments, historically, investors have actually lost a little money in emerging markets. So the whole asset class is extremely sensitive to the direction of the dollar.

The chart below highlights this. The horizontal axis is the volatility of returns and the vertical axis is average returns going back to 1989.

Source: JO Hambro Capital Management

During times of dollar weakness, “you take on a bit more risk but you get a return premium,” Syme said.

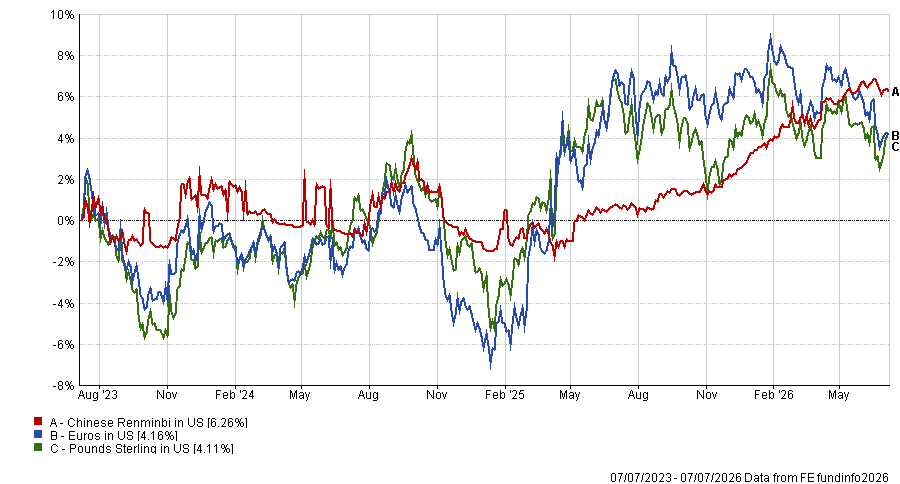

This is pertinent right now because the dollar has weakened significantly over the past 18 months. Indeed, the chart below shows currencies versus the dollar over three years.

US dollar vs other currencies over 3yrs

Source: JO Hambro Capital Management

“The dollar seemed to reach a temporary peak in December 2024 and has broadly been depreciating since. Since then, US growth stocks have clearly been extremely strong, yet EM equities have still outperformed,” he said.

Some investors may query if the data in the first chart is correct, Syme noted, with clients asking him if it is really possible for emerging market equities to annualise at 30% per year during weak-dollar environments.

He pointed to the most recent 18 months, within which emerging market equities have made an annualised return of 39.3% per year as the dollar has fallen.

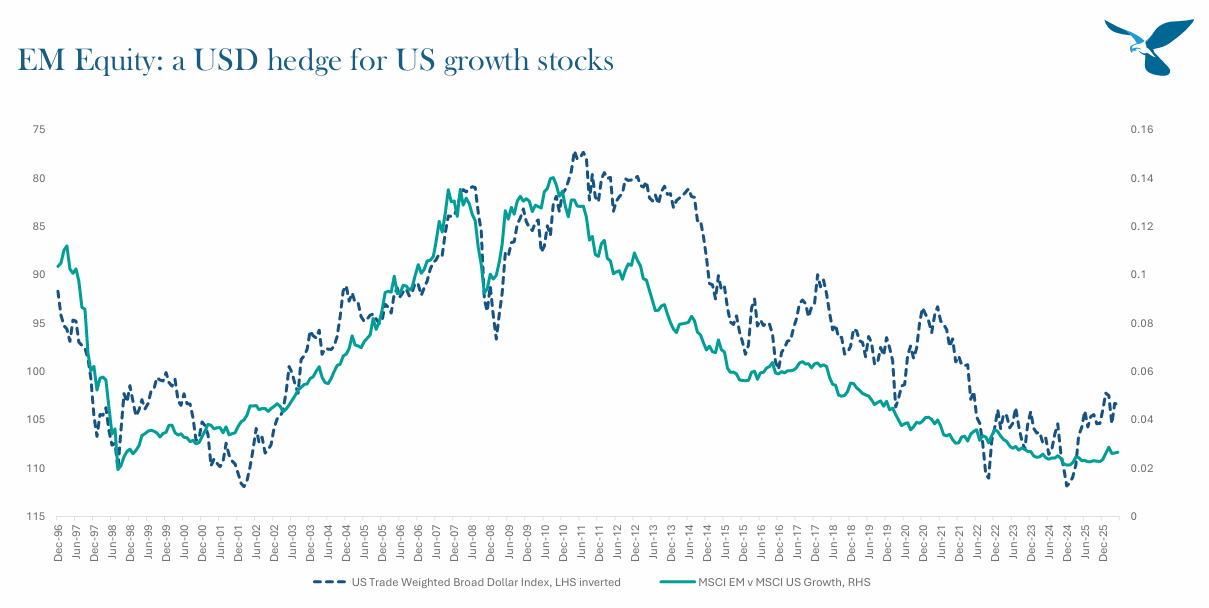

This stark contrast may be useful for investors looking to expand their horizons beyond the US. The chart below looks back at the past 30 years. The dotted line is the direction of the US dollar, inverted, so when the line is going down it represents a stronger dollar; the solid line is the relative performance of emerging-market equities against US growth stocks.

Source: JO Hambro Capital Management

“When the dollar turns down US growth tends to underperform and historically the best hedge [to poor US equity returns] has been emerging-market equity,” Syme said.

This is particularly prevalent right now. After decades of dominance, the US market has struggled to keep pace with the rest of the world as investors have moved their allocations away from American companies on valuation grounds.

“Most of the clients we talk to are trying to work out how much US growth exposure they have, how to manage that risk and what opportunities there are elsewhere,” said Syme.

Those looking at Japan are “extremely concerned about fiscal and monetary policy” as well as the weak yen. Although Europe is an option, he said emerging markets are a “strong fit” for hedging US markets. “It's rare in finance that you get a fit that strong,” he said.

This does not mean the opportunities are across the board. Syme note that the countries that benefit from this phenomenon tend to be more toward the “emerging” part of the asset class, such as Latin America, South Africa, India and Turkey.

Latin America is extremely dependent on commodities, both economically and in market terms. However, since Covid there has been a “huge repricing” in commodities that has not been reflected in Latin American companies.

“That reflects the undervaluation of both the companies and the currencies. Since December 2024 we've seen some strength in Latin American equities and we've been overweight Brazil and Mexico and benefited from that,” said Syme.

“But commodities have moved higher too, so we're still not where we should be. If you take the 10 commodities that matter most for Latin America – iron ore, copper, lithium, silver, gold, wood pulp, sugar, wheat, soy, crude oil – the scale of undervaluation gets enormous.”

The recent repricing is therefore not enough and means Latin American companies are a “great opportunity right now”.

He also likes South Africa, where the economy has struggled for a long time but the new government has implemented positive changes that have led to a sovereign credit-rating upgrade.

“The South African economy is genuinely strong, and again, that hasn't yet been reflected in South African equities,” he said.

Investors should not mistake these as the only places the JOHCM Global Emerging Markets Opportunities fund is interested in at present, however, with China, Korea and Taiwan – all enjoying strong runs from the AI trade – also a key theme.

Co-manager Roshni Bolton noted they own the three biggest emerging-market beneficiaries of the Western AI boom: TSMC, Samsung Electronics and SK Hynix.

“These companies operate at such high capital intensity and technical complexity – thanks to processing excellence and a culture of quality refined over decades – that they hold an almost insurmountable competitive advantage,” she said.

“That allows for margin expansion through the cycle, with better shareholder returns at the peaks and higher margins at the troughs compared with previous cycles.”

However, valuation still matters, she said. The fund continues to own these stocks as the managers believe their share prices are “still reasonable”, but noted that this is something “we would reassess if the valuation becomes untethered from the fundamentals”.

Syme pointed to selling out of commodities in early 2008 (too early) as an example of this. “We were early, and we were wrong, and then we were very right,” he said.

The fund made similar changes with consumer and domestic demand in 2011 and 2012 in the lead up to the taper tantrum, and again with Chinese internet names in 2021.

“For now, we still find value in these three [AI] names, but when the time comes, we will move against them. It's not just about riding the trend all the way to the end; there has to be a point at which you can no longer find upside in these names compared with others, and as that happens, we have to look for other opportunities,” said Syme.