“If I had asked people what they wanted, they would have said faster horses.”

- Often attributed to Henry Ford

Investors have for decades relied on their ability to predict returns, but the evidence is clear; it’s extremely hard to do. What if there was another way to generate better returns? We argue that by abandoning return forecasting and focusing instead on risk, we can create a portfolio that has both high risk-adjusted returns and high absolute returns.

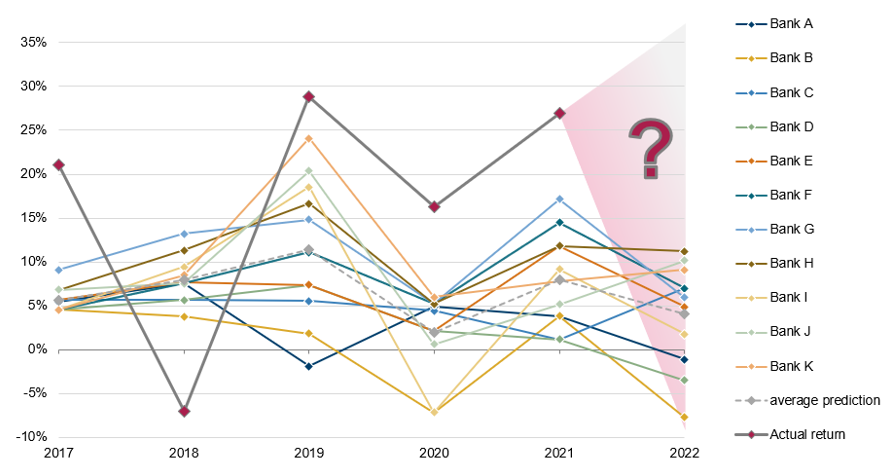

Often conventional thinking becomes so ingrained that it is difficult to imagine anything outside its borders. Consider the S&P 500, one of the most watched financial markets, and perhaps the best-known barometer of investors’ wealth. The S&P 500 returned 27% in 2021, 17% ahead of its 30-year average.

It is clearly a worthwhile exercise to predict such performance and allocate capital accordingly, and indeed analysts from investment banks – arguably some of the best informed market participants around – duly make their predictions on an annual basis.

According to Bloomberg, only one got within 10% of the S&P’s actual return in 2021. On average, the cohort was out by 19%, and the worst by 26%.

What’s more, when you look back historically, as we do in Figure 1, 2021 was not an unusual year. It seems that even the best informed analysts are unable to forecast the returns of arguably the most-watched financial market in the world.

Figure 1. 12-month ahead return forecasts of the S&P 500 by bank analysts

Source: Man Group database and Refinitiv, as of 31 January 2022

Does this matter? Well, yes it does.

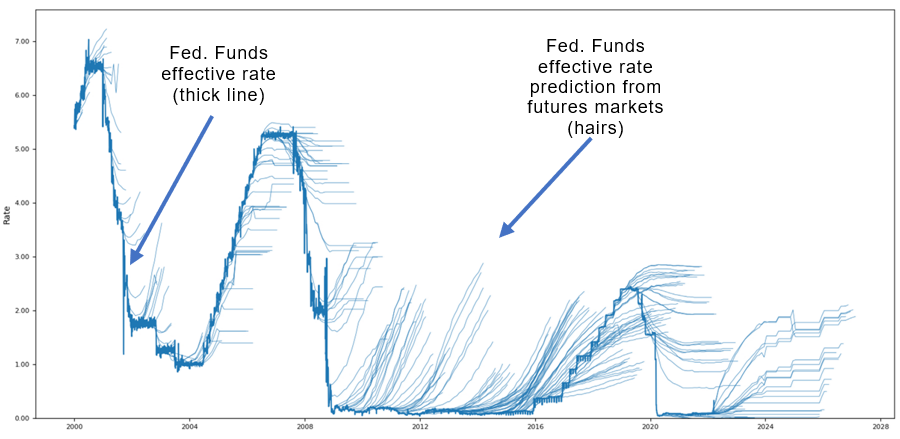

The unreliability of return predictions means we are liable to mis-allocate resources. Further, if Figure 2 is any guide, there is scant evidence that the crystal ball works any better in rates markets.

Figure 2. Federal funds effective rate versus expectations from federal funds futures markets

Source: Man Group database, as of 28 February 2022

One answer to this predicament might be to attempt to generate better predictions. Given evidence from Figures 1 and 2, however, we might argue that this is the equivalent of asking Henry Ford for faster horses. Instead, we believe there is an alternative route to generating better returns; by abandoning horses altogether and abandoning return forecasting.

As investors, ultimately we want to generate a better return on our capital, but our key point would be that we shouldn’t do this without factoring in risk. We might not, for example, invest the same amount in two asset classes whose return estimates were the same, but whose risks are quite different. Common sense suggests investing more capital to the asset with lower risk, all things equal. Risk-adjusted returns, therefore, would seem to be our primary goal when constructing portfolios.

Risk-adjusted returns can be maximized either through improving return predictions, which we would all agree is hard, or by improving risk predictions. It stands to reason that if we predict that risk is likely to decline or stay low, we should allocate more capital to it.

In this context, some academic work by Harvey et al (‘The impact of volatility targeting’, Journal of Portfolio Management, 2018) is particularly useful. They find that the volatility of US equities in a given month is a good predictor of volatility the following month; if volatility this month is low (high), it is likely that volatility next month is also low (high). All things equal, therefore, risk-adjusted returns are likely to be higher when risk is low than when risk is high.

It is comforting to know that we should put more money to work in the good times, and take money off the table in the bad. This should help us sleep better at night.

You can’t eat Sharpe ratio

The astute reader will no-doubt point out that in the real world, it is often the absolute return that matters, not the risk-adjusted return. Who cares if a 2% return is achieved with an information ratio (return/risk) of 3, when a return of 6% is required to meet liabilities?

Faced with this problem, it seems natural that investors seek better returns through taking more risk. This may mean allocating more to equities than bonds, or more high-yield over investment-grade credit, for example. This problem is exacerbated, of course, the lower interest-rates become, and indeed this has been the narrative for most of the last three decades.

Leverage to the rescue

So it would seem that the real world (the desire for an absolute return) gets in the way of what is optimal from a capital allocation point-of-view (maximizing risk-adjusted returns).

However, this problem is fairly easily solved with a little leverage. Either by investing in marginable instruments (futures over cash, for example), or borrowing to fund cash positions, higher returns can potentially be generated from investments with high risk-adjusted returns. From our example in this section, we can turn a 2% return into a 6% return by gearing three times, and still with an information ratio of 1. Leverage is often viewed in a negative light, but when the risks are properly understood it shouldn’t have to be this way, in our view.

Conclusion

In a nutshell, what we are saying is that returns are hard to predict, but we don’t need to predict returns with greater accuracy to generate better returns from our portfolios. Investors can additionally look at the predictability of risk, and make use of leverage to gear up investments with low returns yet high risk-adjusted returns.

Focusing on risk lends itself to a systematic approach, which has the advantage of removing emotion from the investment equation. Risk is measurable, unlike return forecasts, which can easily change depending on number of coffees drunk. Perhaps it’s time to embrace this and accept our failings. Perhaps we should not just back another horse, but choose a different race altogether.

Graham Robertson is head of client portfolio management at Man AHL. The views expressed above should not be taken as investment advice.