Macro-economic uncertainty is punishing many investment trusts, whose prices have fallen to “extraordinary levels, not seen since the global financial crisis”, according to Peel Hunt's head of investment companies research Anthony Leatham.

Discounts are a popular way (for investors that wish to) to time markets, buying good investment companies at low prices in the expectation that this will correct over time.

“Whilst uncomfortable today, the opportunity cost of not getting involved at these levels is akin to the post-great financial crisis period,” he said.

This is especially true for trusts in the alternatives sector, including private equity and property, long-duration growth-focused strategies and inflation-linked portfolios. Below, Peel Hunt’s analysts highlight some of the trusts that have fallen to anomalous discounts.

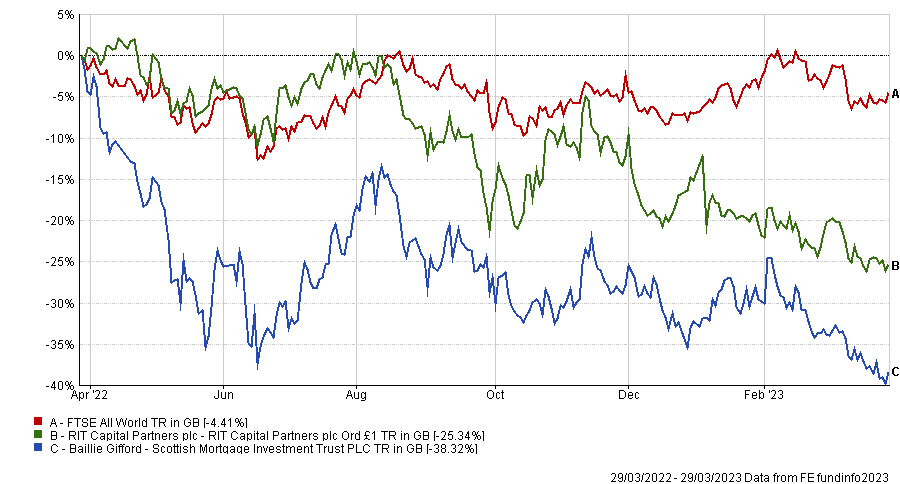

We begin with the highly-regarded and long-term outperformer Scottish Mortgage, which has suffered for its exposure to unlisted assets, as investors have become weary of opaque portfolios, perceived valuation risks and board disruption. This has combined to widen the discount to 21%.

“Given the cloud of negative sentiment hanging over Scottish Mortgage, it is not clear where the discount will settle,” said Leatham.

“However, if we apply the average PE [private equity] trust discount of 40% to the unlisted holdings, and a 15% discount to the listed equity assets (using the IT Technology sector average), then a blended discount of 22% is around fair value.”

Similarly, RIT Capital Partners has moved to a 24% discount due to its above-average 41% exposure to private equity.

Other highly-regarded and long-term outperformers across private and public equity strategies that have reached abnormal discounts include Syncona (23% discount), Augmentum Fintech (37%) and HarbourVest Global Private Equity (51%).

Performance of trusts over 1yr against index

Source: FE Analytics

The list continued in the renewables sector, where Gore Street Energy Storage trades at a 16% discount versus a 12-month average premium of 4%.

“Understandably, there is a lot of excitement about the structural need for battery storage and the important role that it plays in the energy transition,” said Leatham.

“However, this discount may be a reflection of how far-out some of their construction projects are, particularly when compared to other sector peers.”

Energy efficiency trusts have also fallen in price. Here, SDCL Energy Efficiency Income “has the advantage of scale and liquidity, however, the rating has suffered in sympathy with its smaller peers.”

“We note that there are some exciting developments in the portfolio, which are either not particularly well-understood or have been overlooked by investors.”

Performance of trusts over 1yr against sector

Source: FE Analytics

Moving on to the infrastructure sector, Digital 9 Infrastructure delivered company updates that featured a number of “important catalysts for NAV growth and improved dividend cover”, which are “not reflected” in the 38% discount, according to Peel Hunt researchers.

Trading at an 18% discount, the Octopus Renewables Infrastructure trust was also highlighted for recently putting through a 10.5% increase in its dividend and recent full-year results showing “strong dividend cover to support this diversified strategy”.

For investors attracted to the income and the inflation-linkage provided by property, Peel Hunt highlighted the LXI REIT (33% discount), the Supermarket Income REIT (27%) and the Residential Secure Income REIT (36%) – the latter is yielding 8.3% for a “resilient portfolio of shared-ownership properties”.

Another source of income which “continues to trade on wide discounts, despite robust returns” were the two high-yield, short duration and floating rate debt strategies: Sequoia Economic Infrastructure Income, which trades on a 15% discount with a yield of 8.5%, and BioPharma Credit with 6% discount and 7.2% yield.

Finally, Peel Hunt researchers highlighted four opportunities where continuation votes are due: abrdn Japan Investment Trust, European Opportunities Trust, VinaCapital Vietnam Opportunity and JPMorgan Indian Investment Trust.

The JPMorgan trust in particular was “an interesting opportunity” also due to a conditional tender offer which “will provide some downside protection to performance over the next two and a half years”.