Long‑term trends such as electrification, AI‑driven power demand and the global push toward decarbonisation are shaping the multi‑decade opportunity set across global listed infrastructure, according to Tom Levering, lead manager of the $1.7bn Wellington Enduring Infrastructure Assets fund.

Recent geopolitical disruption, including the conflict in the Middle East, has brought those themes into sharper focus rather than changed their direction, the FE fundinfo Alpha Manager said.

In 2022, when Russia invaded Ukraine, Europe’s dependence on Russian gas became painfully clear, he noted.

“If you look at what is now happening in the Middle East – it’s the same story [on a global scale],” said Levering.

He noted that the need for energy autonomy has not gone unnoticed by the market, which “loves energy right now, so energy infrastructure prices have gone up”.

Levering stressed that while geopolitical events can dominate headlines and short‑term price moves, his investment approach remains focused on long‑duration infrastructure assets rather than making near‑term macro calls.

“With the extreme bullishness on energy, the risk is a resolution in the Middle East, so we are thinking about how to avoid direct exposure to that and how to benefit from the other side of it,” he noted.

As such, he said the Wellington strategy has been investing in companies that own and build liquefied natural gas (LNG) regasification facilities in Europe, as well as companies building liquefaction capacity in the US.

This was echoed by Hilde Jenssen, head of fundamental equities at Nordea Asset Management, who said that “companies with long-duration growth visibility, regulated or contracted cashflows and structural alignment with energy security and decarbonisation goals” are a good investment opportunity right now.

In particular, she said she sees the most compelling opportunities in European grid infrastructure and transmission – upgrading ageing networks, expanding interconnectors, and deploying advanced cables, transformers and digital control systems to handle rising electricity demand.

Decarbonising the world

While Levering is cautious about direct exposure to near‑term energy price volatility driven by the Middle East conflict, he argued that it ultimately reinforces a much longer‑term shift toward decarbonisation and electrification.

Global research group Wood Mackenzie modelled a scenario in which prolonged disruption to Middle East energy supplies triggers a long-term structural shift towards energy independence. It noted that global oil demand could fall by 20% and gas demand by 10% by 2050, while there would be an acceleration in investment in electrification, domestic renewables and nuclear power.

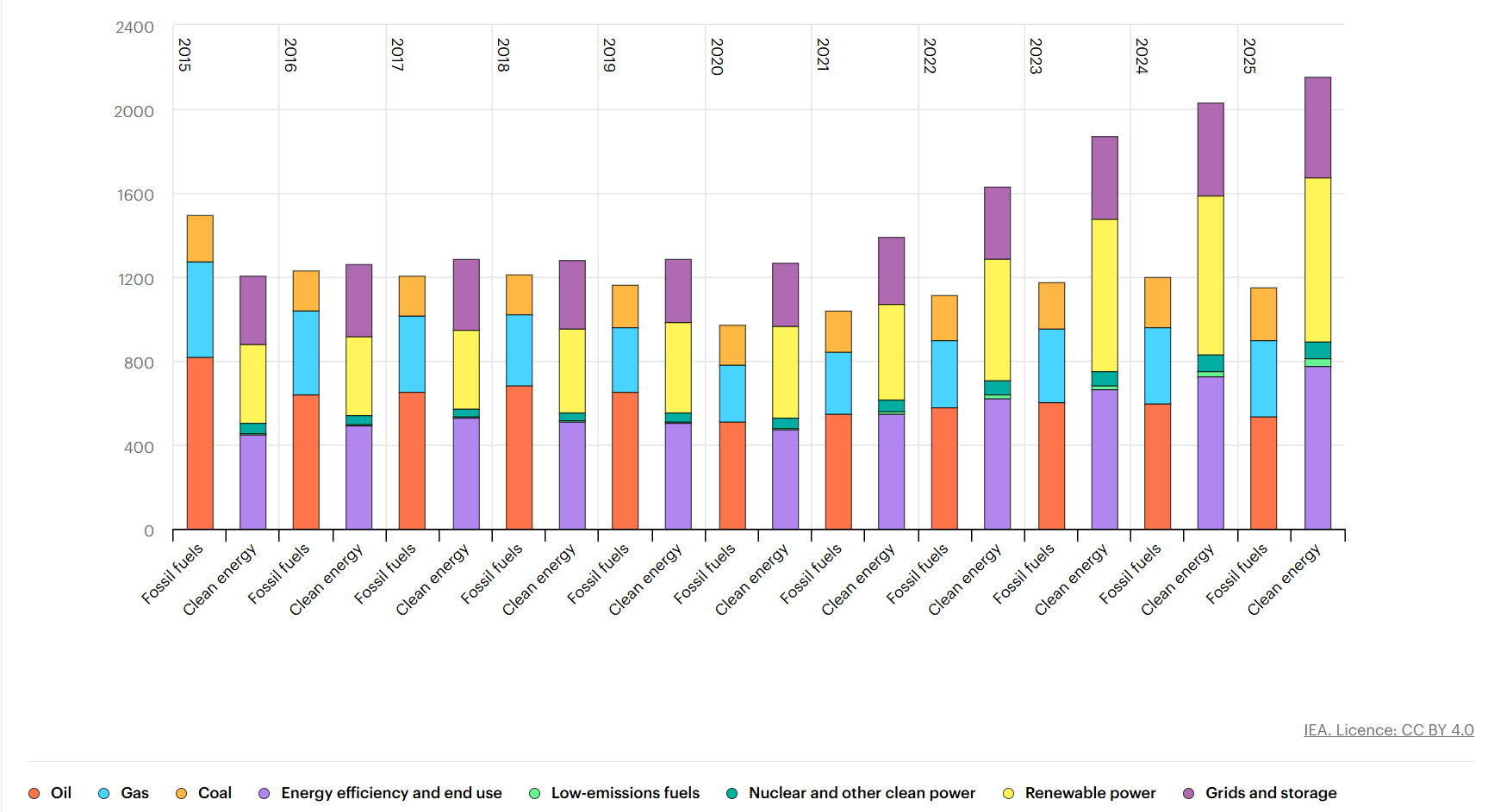

Indeed, the International Energy Agency’s (IEA) 2025 ‘World Energy Investment’ report projected that capital flows to the energy sector were likely to reach $3.3trn in 2025, with $2.2trn earmarked for clean energy and electrification – twice as much as the $1.1trn expected to go into oil, natural gas and coal. The 2026 report is due in June 2026.

Global investment in clean energy and fossil fuels, 2015-2025

Source: IEA

Levering said that one of the biggest changes in his career as an infrastructure investor has been the advent of the decarbonisation trend and the resulting shift to electrification.

“The growth rate in oil and natural gas assets has come down – so we [the fund] own very little of that today, while the sheer level of growth in electrification is reflected in our portfolio.”

The Wellington strategy’s top 10 holdings include E.ON, one of Europe’s largest electrification distributors and grid operators. Meanwhile, fellow portfolio holding global power utility ENGIE bolstered its focus on low-carbon electricity production by acquiring distributor UK Power Networks in February 2026.

“So you end up with a fund that looks far more electric infrastructure-heavy than oil infrastructure,” said Levering.

However, with low-carbon energy typically dependent on inconsistent power sources such as wind (which isn’t always blowing) and solar (which is dependent on sunlight), Levering said it is also important to invest in natural gas power infrastructure “to back up the grid”.

“More natural gas power plants are actually good for renewables because they allow higher penetration levels that the grid otherwise could not handle,” he said. US midstream natural gas company Targa Resources is the fund’s top holding at 4.7%.

AI infrastructure

Levering identified AI as another multi-decade theme he expects to remain dominant in the infrastructure sector over the long term.

“It has been a huge accelerant to overall power demand growth,” he said.

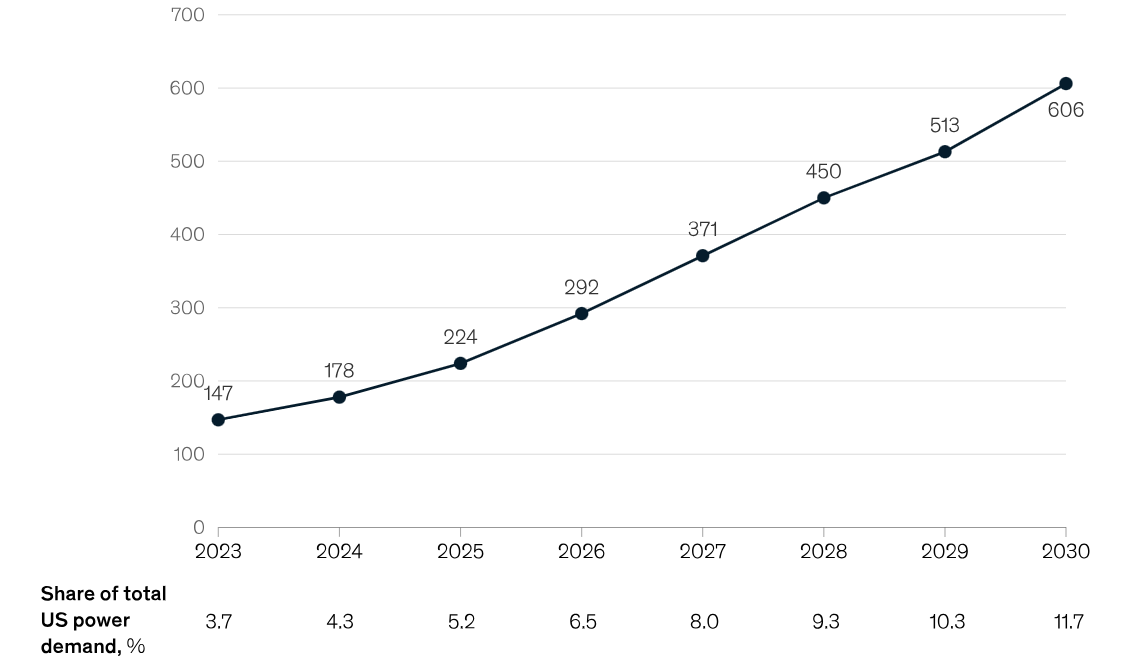

McKinsey research suggests that the power needs of data centres could reach 11-12% of US power demand by 2030, with electricity demand for data centres in the US specifically expected to increase by about 400 terawatt-hours (TWh).

Demand for power from US data centres (TWh)

Source: McKinsey & Co

“But technology is a very competitive business, with assets that depreciate quickly, so considering how we can participate in the AI build-out while keeping our risk profile the same led us into regulated utilities that are building the power infrastructure to supply data centres,” said Levering.

He noted that a one-gigawatt data centre can cost as much as $50bn to build and “the power assets related to that are another 5-10%”.

One of the big concerns surrounding the AI build-out is the risk to return on investment – are the big bets going to pay off?

Levering said the contracts and regulations surrounding the power infrastructure involved are structured so the data centre is “obligated to pay the full cost on a take-or-pay basis – so very little risk on a regulated basis”.

“Regulated electric infrastructure is one of the most overlooked parts of the puzzle because returns are steady, so investors tend to ignore it in favour of assets where returns have spiked due to AI demand,” he added.

“We think chasing those higher growth rates can be a problem, so we are focusing on regulated infrastructure growing at high single digits.”