Every geopolitical shock of the past decade in Asia has looked alarming in the moment and irrelevant five years later. The pandemic, US-China tensions and the recent oil spike that followed the conflict with Iran all spooked investors and moved markets but ultimately faded.

In fact, “every dip in emerging markets has been a red herring", according to Jason Pidcock, manager of the £2.6bn Jupiter Asian Income.

“It has spooked investors of a nervous disposition but has been an opportunity for traders and something that we have looked through, including the most recent one, the conflict with Iran,” he said.

"Some people would have been caught out. They would have sold because they got scared and then bought back in at a higher price.”

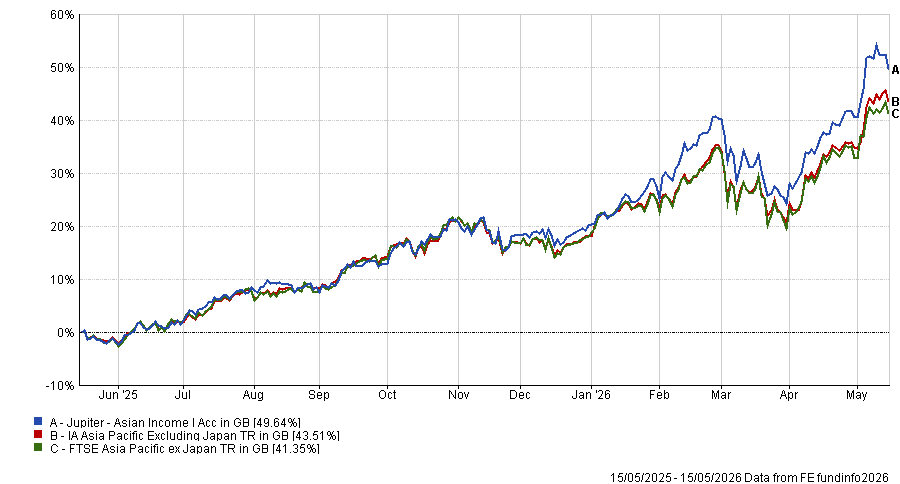

His cool head has paid off so far. The fund has a maximum FE fundinfo Crown rating of five and is up 24.4% year to date against a benchmark gain of around 20% over the same period. Since launch in March 2016, it has returned 85.6%, with first-quartile performance over one, three and five years.

Performance of fund against index and sector over 1yr

Source: FE Analytics

The Iran conflict pushed oil prices higher and hit emerging markets unevenly – India, the Philippines and Pakistan felt the impact more than wealthier markets like Taiwan, Korea and Singapore. Pidcock expects the effect to reverse as prices normalise, with the market having already priced in much of that recovery.

"The market knows this is a man-made issue which will come to an end," he said.

Getting exposure to Asia now also brings another advantage, according to the manager, in the form of early access to a product that consumers, factories, armed forces and government departments will all be buyers of in the next decade: humanoid robots.

"In 10 years' time there will be humanoid robots all over the place," he said. "You may have one in your home. You will certainly have friends or family members who own a humanoid robot."

The hardware and software those robots require, he said, will largely come from Asia – and the fund already has exposure to companies he expected to benefit.

This is the next leg of the same technology earnings story already driving returns in Taiwan and Korea – an extension of the productivity gains that AI is beginning to deliver, he said.

However until then, some stocks will suffer in the meantime.

"There are times where we own stocks that we even think are likely to underperform," he said. "They are balancing and hedging to a degree the bigger chunk of the portfolio where in the short term we are expecting outperformance."

Over five years, he expects every holding to beat the market.

The fund holds 25 stocks across five markets, with technology and financials as the two largest sector exposures – 41.2% and 21.6% respectively.

Top names in the portfolio include Taiwan Semiconductors (9.4%), Samsung Electronics (7.9%) and Taiwanese semiconductor company MediaTek (6.6%).

Taiwan and Korea, Pidcock argued, are indispensable to the global semiconductor supply chain – US companies that dominate AI development could not function without them. That makes Asian tech a play on global growth rather than domestic or regional economies alone.

Finally, the macro backdrop is also more convincing than in some developed markets. The four areas where Jupiter Asian Income has most of its money had an average GDP per capita of $62,000 against $58,000 for the US, euro area, Japan and the UK combined, with higher GDP growth, smaller budget deficits and lower government debt to GDP.

The fund's price-to-earnings ratio is lower than that of developed markets and its dividend yield – currently 2.91% – is higher.

A weaker dollar, if it continued, would add further to the case. Pidcock noted that capital flows into Asia tend to follow dollar weakness and that the fund's gold mining positions – around 5% of the portfolio – would be direct beneficiaries.

"We don't forecast currency," he said, "but if there is a weaker dollar, we have enough companies in a structural growth story not to really worry about what the currency markets are doing."