The Lowland trust has a long list of stocks: 118. That is a lot for an active fund, as many choose to take a high-conviction approach to investing, picking relatively few stocks and hoping their choices will perform better than the average.

“This isn’t conviction management,” said James Henderson, manager of the trust. “I don’t know how one can be truly convinced by things. There are too many variables and too much difficulty out there.

“But you can think, on the balance of probabilities, that something’s cheap and worthwhile – and then try to make it count within the portfolio.”

That is how he runs Lowland, taking bigger positions in companies where he sees more upside but including a long list of stocks that should mitigate the fact that the managers will be wrong “some of the time”.

The portfolio is benchmark-aware but is not driven by the index, he explained, with Henderson and co-manager Laura Foll willing to avoid large index stocks such as British American Tobacco and AstraZeneca where they feel there are better options elsewhere.

“Not owning the concentrated list of big-cap stocks allows us to have a much greater variety of things,” he said, which includes investing in a large range of mid- and small-caps.

While his top 10 largest holdings are all large-cap names, a good chunk of the portfolio is invested lower down the market capitalisation, as these stocks have more room to grow.

Henderson said: “A small company of £250m is more likely to become a £2.5bn company than a £2.5bn company is likely to become a £25bn company.”

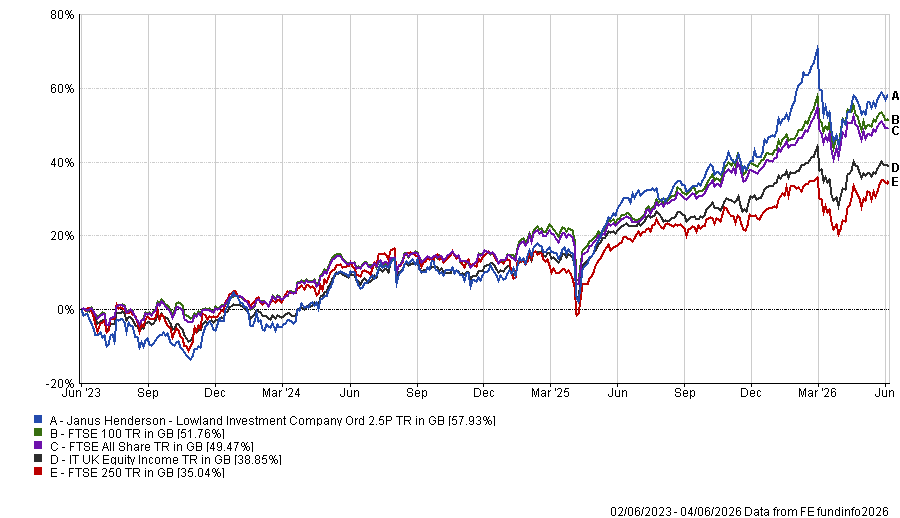

The area has been challenging for Lowland in recent years, with mid- and small-caps underperforming their large-cap peers. However, the trust has been a top-quartile performer in the IT UK Equity Income sector during this time, despite the poor performance at an index level.

Performance of trust vs sector and indices over 3yrs

Source: FE Analytics

While mid- and small-caps have underperformed at an index level, there have been several companies bid for in the past year. In the Lowland portfolio, he highlighted chain maker Renold and credit products and insurance services provider IPF as lucrative examples.

Smaller companies remain out of favour, with investor meetings “still quite lonely” for Henderson, who said there are “not many people turning up for them”.

“At the moment, the brokers have to work quite hard to get much interest going,” he said, but noted that this is why he remains positive – arguing it is usually a bad sign for the market when there is too much interest, as this often signals the top.

“We’re 12 or 13% geared at the moment. And we’re getting cash in from these takeovers. It’s not taking us long to find good value homes for that cash, so it’s an interesting time,” he said.

Below, Henderson explains the parallels between investing and gardening, why the UK has an investing problem and how politics rarely has an impact on markets, despite a lot of discussion about it.

What is your process?

We have an emphasis on income and growth. I’ve always believed that the way to grow the income is to grow the capital first, so we never chip away at the capital and pay it out as income. And then we aim to get sustainable income growth coming through too.

We’re more value and contrarian-driven than some funds. One way we look at it is turnover to the market cap, adjusted for debt. That gives a feel for the size of the business. Then we ask: ‘Will it get a better margin on that turnover by the actions management is taking, by us helping them, or some other means?’

There are different risk metrics in different sectors. For the general capital goods companies, turnover is a good one. For property companies, for instance, the obvious one is discounts. But it’s not just one number.

Does the UK have an investing problem?

There is definitely a problem getting money into productive investment. For me, the biggest issue was UK pension funds leaving the market. [New] initiatives to try and get people back are interesting but they won’t get very far. They’re not going to be a big help.

I think what brings investors back to the UK is performance – another period like we’ve had over the past couple of months or so. We are seeing real interest. It’s at the margin, but we are seeing interest.

Do you worry about politics?

If I could have all the time of my life back that I’ve spent discussing politics, I’d be able to do something [useful] with it. We debate politics a lot but it rarely has much effect on the market at the end of the day.

I don’t think there’s any correlation between a change of party and stock market returns. Actually, there’s very little correlation between GDP growth and market returns as well. After all, you’re not buying the UK economy, you’re buying individual companies with individual management teams that do their own thing and find their own way with the problems they face.

Good management teams and reasonable valuations are much more important than worrying too much about politics. That’s why we don’t spend a lot of time debating politics.

What have been your best and worst stock picks in recent years?

Over the past two years the greatest contributors have probably been the banks, with Standard Chartered up around 175%, Barclays 116% and HSBC 100%.

Another big driver of performance has been from companies being bought at substantial premiums. In two years, we’ve lost seven companies to acquisition. IPF was taken over at a considerable uplift to the undisturbed price last year, for example.

Conversely, Marshalls is one of our biggest losers – down 55% in two years. It’s a well-run company that’s been dragged down by economic woes, but we think it will come good eventually.

What do you do outside fund management?

I have an interest in gardening. I joke about it being like this job – needing variety in the garden and not wanting everything out at once. You need things coming into flower at different times.