Electricity demand is growing for the first time in 15 to 20 years across the developed world thanks to the introduction of AI, which is putting greater pressure on how countries will produce their energy, according to Manuel Losa, co-manager of the £4.9bn Pictet Clean Energy Transition fund.

The outbreak of the Iran war earlier this year pushed oil and gas prices to multi-year highs and made renewable energy sources far cheaper, although they were also cheaper before the war, he said.

“Renewables are at a point – and they have been there for the past six years – where it is cheaper to build a wind farm or a solar panel than to simply run your existing gas or coal power plant,” he said.

“If you install an onshore wind farm in the UK, it will be deflationary for UK electricity consumers. If you install solar PV, it's less deflationary in the UK, but in Spain it will be massively deflationary.”

This comes at a time when electricity demand in developed countries, in Europe and North America, which had been flat or declining for the past 15 years, is now going up.

“It is no longer only about substituting. You're not only thinking about running your gas power plant versus building a new wind farm. Now you're thinking about building additional capacity,” he said.

This changes the mix. While gas is convenient – as it can be turned off and on when required – it is expensive. And renewables are catching up.

For example, in countries such as Spain and those with latitudes closer to the equator, solar can sustain energy 90% of the time.

In the UK this is not possible as there is less sunlight, but the renewable mix can reach 90% of the energy requirements, he said.

“Right now it is not only about substituting. You're not only thinking about running your gas power plant versus building a new wind farm. Now you're thinking about building additional capacity and to invest in the energy transition, because electricity demand for the first time in 15 to 20 years is growing. Renewables will account for a significant part of that new energy supply.”

Below, Losa explains how Pictet Clean Energy Transition invests similarly to Charlie Munger’s philosophies and shares an anecdote from a recent SpaceX trip in which Elon Musk explained what was needed for the world’s energy picture to resemble a “respectable civilisation”.

What is your process?

We try to outperform the MSCI AC World by investing in companies that will benefit from the clean energy transition. Many people focus a lot on valuation or focus a bit more on quality but I like to say we like Charlie Munger’s qualities: we like to buy great companies at a fair price. And sometimes we prefer this much more than buying fair companies at a great price.

In terms of company metrics, we focus a lot on profitability. I think returns on equity are one of the best metrics. In terms of valuation, one thing that is very important is sustainable free cashflow yield, which is similar to the P/E [price-to-earnings] but it's your free cashflow assuming that your capex is equal to your maintenance capex.

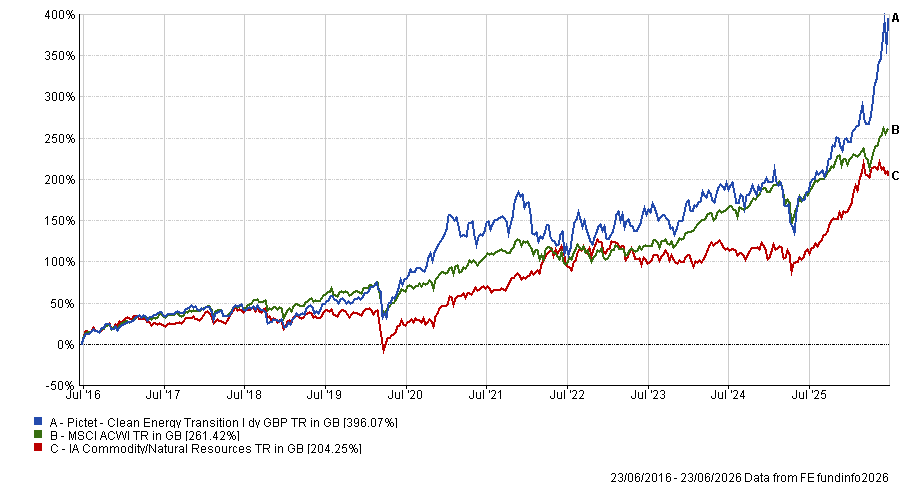

Performance of fund vs sector over 10yrs

Source: FE Analytics

How are renewable energy and oil different from an investing perspective?

Some people say: if the energy transition is such a revolution as oil was, why have we not seen the same kind of evolution we saw in oil, which took maybe 10 to 15 years?

And the reality – which many people don't pay attention to – is that oil is a liberalised market. Renewables and electricity in most countries are regulated markets, you cannot charge whatever you want.

With renewables, you have contracts, so you cannot make whatever you want. Even when there is a moment when you could make a ton of money, like the Ukraine war, prices are capped. That never happened to oil.

Basically, because they are regulated, there is a cap. Companies need to invest a lot of money to do this [build out renewable energy], and if you have a return on equity of 10%, and there is no dividend growth, you cannot grow more than 10%.

So why should people invest in the energy transition now?

Because I think it is one of the largest challenges we have ever faced and it's going to be economical for everyone. When we talk about the energy transition, we are not only talking about changing the electricity mix, we are talking about changing the whole energy mix.

The world consumes somewhere around 160 to 170 petawatt hours per year in gross consumption. Final consumption is a third of that; we lose two-thirds of that energy to heat, etc.

I met Elon [Musk] at SpaceX, four weeks ago. He was saying that we use one divided by one trillion of the total solar energy. To be a ‘respectable civilisation’, we should improve that by one million.

Now, I'm not sure that's the exact order of magnitude, but to progress as a civilisation, we should take more advantage of the renewables and solar sources that we have.

That is a challenge and it will probably imply that we see investments moving more towards electricity, more towards renewables, and more investment in efficiency over the next 20 to 30 years. There is nothing that is going to stop it.

Is Pictet Clean Energy Transition all about renewables?

When we think about the energy transition, most people focus only on the renewables part, which is about supplying energy. When we invest in the energy transition, that is only one part of where we invest. We invest across the whole value chain of the energy transition.

It means electrification, which is renewables, but it also means energy efficiency. Within efficiency, we can invest in things that improve efficiency across the board: more efficient chips, more efficient HVAC systems or buildings that are much more insulated.

The opportunity is not only on the renewables side, there is opportunity everywhere. Whether we move towards more renewables or less renewables, or other parts, depends on the matter of valuation: finding great companies, finding companies with great returns.

Why are you so keen on semiconductors?

There is no energy transition without semiconductors. Semiconductors allow you to pass electricity and to stop it. When we think about solar panels, they produce electricity as DC. You need to move it to AC, so you need semiconductors and inverters to do that.

But then you also have AI, which requires a ton of electricity. We know that. A one-gigawatt data centre is the equivalent of powering a city of one million people. And if we are able to manufacture chips which are much more efficient, we will reduce the amount of electricity we need to consume, but also process more information with the same amount of electricity.

We invest in chips which are the most efficient, which can be sometimes 40% or 50% more efficient than the ones most people talk about.

What have been your best and worst performers over the past year?

The best name I would say is Marvell, which is similar to Broadcom. Last year, because of competition concerns, the stock did very badly, but we've been adding over the past 12 months and added for the last time in March. Since then the stock has done significantly more than 100%. Over 12 months it is up circa 242%.

One would be some of the industrial software names we hold, because the sector has seen significant de-rating. Nemetschek was down 47% over the past year.

What do you do outside fund management?

Apart from spending time with the family, I like a lot of sports. That would include anything from skiing to cycling, running and playing basketball.