Some investments take years before reaching their full potential, but when they do, returns can be spectacular.

Overlooked by most investors and less famous than giants like Samsung, TSMC or Nvidia, Taiwan Union Technology is a Taiwanese company that makes copper-clad laminates; a printed-circuit-boards component critical to AI hardware that only a handful of companies globally can supply in its high-end version.

Gabriel Sacks, manager of the Aberdeen Asia Focus trust has held it for years, but over the past 12 months it returned 833%.

“While the market has been focusing on the mega returns from investing in mega-cap names, our best calls in the last year have been from names we have held for several years and show that thinking small can also lead to exceptional returns,” he said.

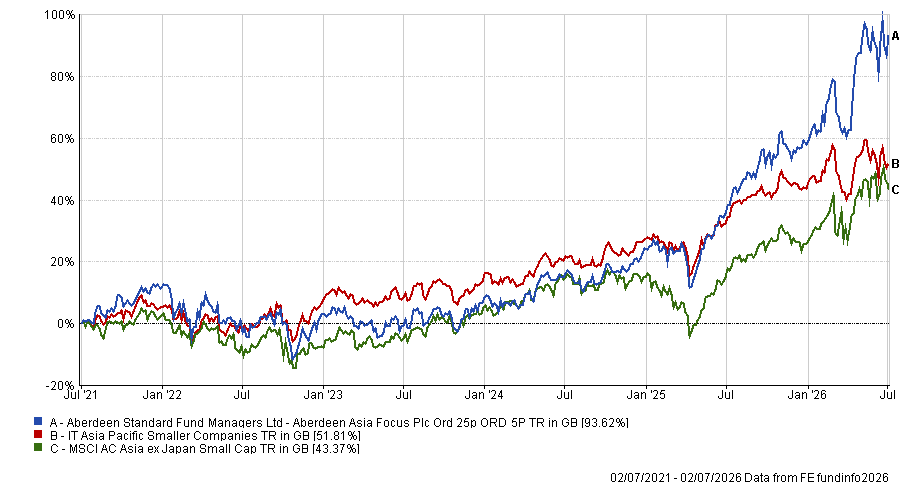

Aberdeen Asia Focus invests in smaller companies across Asia excluding Japan and Australia. It has returned 47.5% over the past year and 99.2% over five years, with an active share above 95%. Sacks’ argument is that the richest opportunities in the region are not in the names that dominate the index. Below, he explains why.

Performance of fund against sector and benchmark over 5yrs

Source: FE Analytics

What is your investment philosophy and process?

Quality investing for us is about identifying businesses that can sustainably create shareholder value: clear competitive advantages, strong profitability, resilient cashflows and a disciplined balance sheet.

No single metric captures that, so we score companies across five dimensions – industry economics, business model strength, financials, management quality and ESG. Only a small subset meets our highest standards, which naturally concentrates the portfolio into higher-quality names.

We keep an open mind on sectors. Avoiding being prescriptive can lead us into tougher, cyclical areas that are under-appreciated by the market, and that's where the mispriced opportunities are. We exit when the thesis breaks down, or when the story has played out and there are better opportunities elsewhere.

Why should investors pick your fund?

Small-cap in Asia doesn't mean what people think. We're looking at the bottom 20% of market cap in the region, but that now translates into companies under $10bn or so – many of these would qualify for the FTSE 250 or even the FTSE 100 in the UK.

It's a well-established part of the market, just badly covered since MIFID [the EU Markets in Financial Instruments Directive].

On top of that, large-caps tend to be held across global and tech portfolios, so they move together. Smaller companies move less in line with each other, so a portfolio built from them can reduce volatility at the aggregate level, even if individual names are more volatile.

How are you positioned in the AI supply chain beyond the obvious names?

We've been spending more time going deeper into the supply chain. Lithography from ASML is reaching a point where it's hard to keep shrinking chips, so the industry is starting to stack chips instead, which needs better packaging to manage the electronics and the heat.

That's brought new technologies into demand. Liquid cooling is one: servers and chips increasingly need to be cooled with liquid rather than fans, and we hold a Taiwanese company called Asia Vital that benefits from that shift.

We also introduced a company called ASM PT this year. It's linked to ASML, an older and more legacy business, but the bonding and glue technology it makes for stacking chips has come back into demand.

We've shifted some exposure from Taiwan into Korea and into advanced packaging further down the supply chain, and we've hired a dedicated tech analyst because these areas have become too specialist for generalists to cover.

What's the biggest risk to the Korea trade right now?

China. A few years ago all the electric-vehicle battery manufacturing was Korean – LG Chem, Samsung SDI. Now you have the emergence of CATL, and every car maker will use the Chinese batteries.

In the inspection and metrology space we cover, a lot of the Chinese market has already moved to Chinese suppliers. There are two big Chinese memory makers coming to list soon. We need to watch China as a disruptor.

Samsung and Hynix are still relatively cheap though, and earnings are coming through strongly. If you want broad exposure to Korea's semiconductor cycle, pair Asia Focus with large-cap or passive exposure to the region.

What were the best calls over the past 12 months?

Taiwan Union Technology is up 833% over one year. Capacity constraints mean it has increasing pricing power. Chroma ATE is up 634% over one year. It tests semiconductors, power electronics and EV batteries for foundries and system companies including TSMC and Nvidia, and it's been investing heavily in R&D for years.

Both names have contributed more than 500 basis points of relative performance each. We've held them for years: they were under-researched and under-loved when we bought them, and both are more than 10-baggers for us now.

And the worst?

Newgen Software Technologies is down 64%. It makes low-code platforms that reduce the technical barrier to building software, but AI is now doing that job better than we expected.

We underestimated the extent to which AI would offer a more powerful and flexible solution to the same problem Newgen was addressing. We thought organisations would stick with more controlled, guard-railed software given data security concerns. In practice, AI's ease of deployment won out, and conversion of its order book to revenue had already started to slow. We exited the position fully.

What do you do outside of fund management?

I like tennis and football, and I love to travel.