The near-term macroeconomic outlook is still positive for the dollar but the medium-term picture is less positive if foreign appetite for US assets fades or a deflationary growth shock brings Fed easing back onto the agenda.

US economic activity has held up better than other major economies but inflation is proving sticky and the market has had to price a more hawkish Fed path.

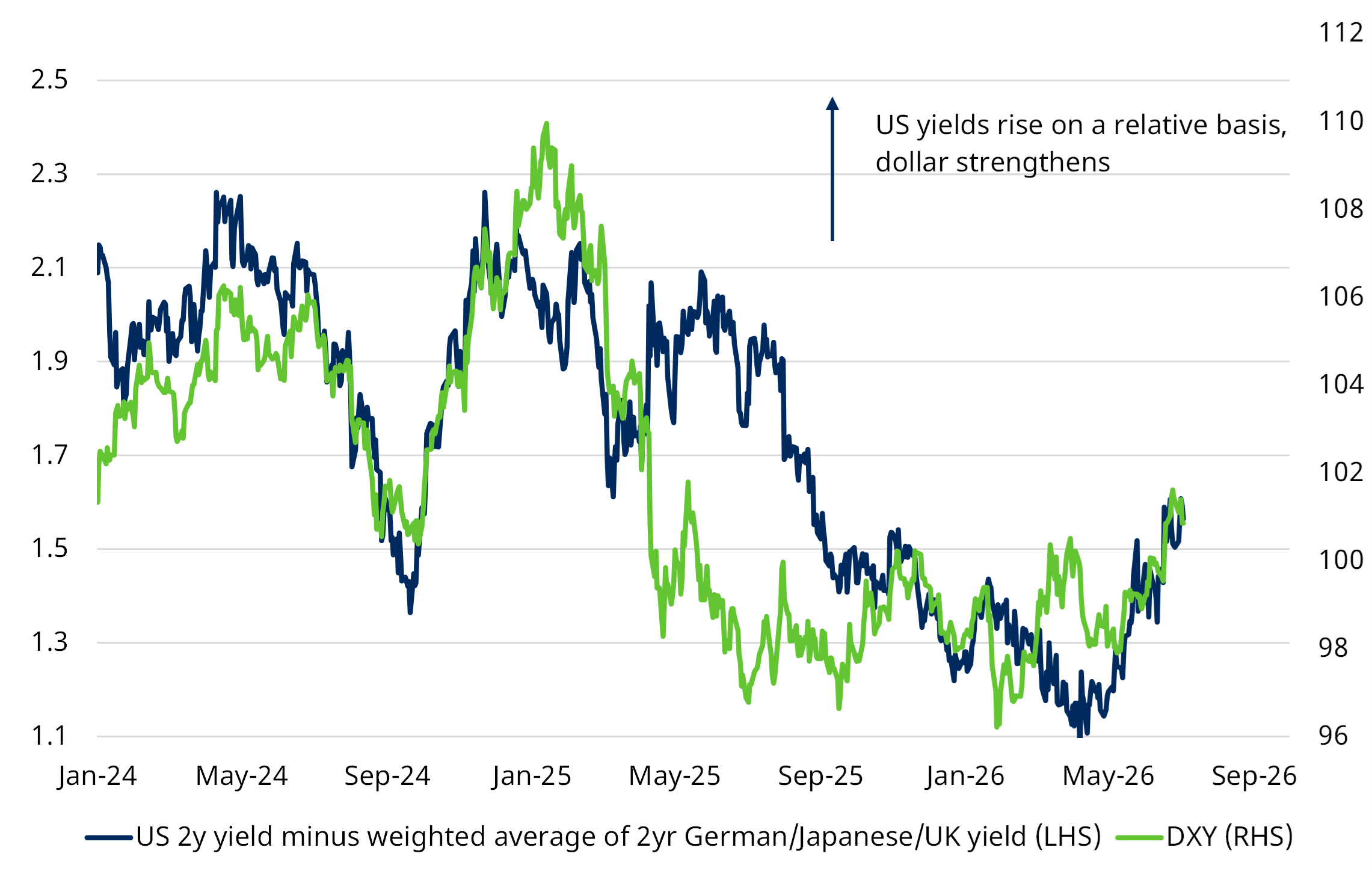

That relative-yield shift has already helped the dollar break higher from its earlier trading range and is broadly consistent with our baseline assumption of dollar strength into the end of 2026.

Relative US yields have been doing the heavy lifting for the dollar

Source: LSEG Datastream, Schroders Economics Group, 6 July 2026.

The other side of the trade for other global currencies remains fragile, however.

While the eurozone economy has been more resilient to the Iran shock and the ECB has been quick to raise interest rates, the euro still looks too firm relative to fundamentals.

With eurozone inflation coming in below expectations, if markets started to price that ECB tightening was not likely, there would be room for euro/dollar to move towards 1.10 in the months ahead.

Sterling is also vulnerable as weak growth, political uncertainty and the pricing-out of UK hikes are consistent with the pound heading towards the mid-1.20s against the dollar.

The yen continues to test Japanese authorities’ appetite for intervention, while the renminbi's recent appreciation may fade later in the year since widening rate differentials against the US will become harder to ignore if export growth continues to roll over.

Base case

All of this chimes with our May Q2 baseline forecast, where the dollar was assumed to rise through 2026 before giving back some ground in 2027.

Our end of 2026 assumptions published back was GBP/USD at 1.21, EUR/USD at 1.07, USD/RMB at 7.09 and USD/JPY at 167.8.

Our end of 2027 working assumption is for the dollar to give back some of those gains – to 1.27, 1.12, 7.03 and 162.5 respectively – as fading inflation pressures give a tough-talking Fed breathing space and a pivot to a more forward-looking policy agenda would bring rate cuts back onto the agenda in 2027.

For now, chair Kevin Warsh’s hawkish rhetoric implies a clear risk that US rates end up being raised, keeping the dollar firmer for longer.

Medium-term risks

But looking further ahead, the medium-term dollar story is more balanced.

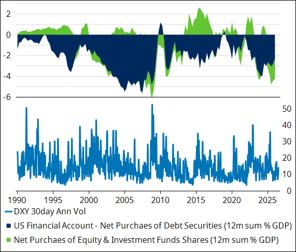

The key support for the dollar is still the relative US yield advantage, but the funding of the US current account deficit has become more dependent on short-term equity and investment-fund inflows. That leaves the dollar more sensitive to shifts in risk appetite.

If US markets keep performing, those flows can continue to support the currency. But if equity sentiment turns, the same channel can amplify FX volatility.

A larger role for short-term equity and fund inflows leaves the dollar more sensitive to risk appetite.

Source: Macrobond, Schroders Economics Group, 24 June 2026.

More generally, if the party in US markets draws to a close there are good reasons to think the dollar will be left nursing a hangover.

A weaker dollar

A weaker dollar has far-reaching implications for all global investors. These range from immediate portfolio effects to longer-term impacts on asset performance as economies, industries and individual businesses adjust to a lower-value dollar.

After all, the consequence of the boom in the US is that is has accumulated large, twin current account and budget deficits and an overvalued real exchange rate.

The implications of a weaker US dollar are neither straightforward or uniform.

If the next trend depreciation of the dollar eventually kicks in, it may pose stagflationary risks for the US, but it could also deliver a deflationary impulse to the rest of the world through cheaper commodity imports and manufactured goods. It could also support common-currency returns to investors from other markets – notably in the emerging world.

However, the outlook is complex, with second-order effects and policy responses potentially creating both winners and losers.

But as we recently argued, one beneficiary could be the yen. It is one of the clearest cases where the medium-term view is starting to differ from the near-term trend.

Near term, fiscal concerns, capital outflows and dollar strength have kept USD/JPY under upward pressure.

But as Japanese real rates turn less negative and the Bank of Japan normalises policy, the incentive to fund carry trades in yen should fade. The medium-term case for a stronger yen is therefore building, though the adjustment is likely to be slow.

David Rees is head of global economics at Schroders. The views expressed above should not be taken as investment advice.