Now that all the “valuation excess” has been shaken out of Chinese equities, it could provide an interesting opportunity, according to Guinness Asian Equity Income fund manager Edmund Harriss.

Despite the regulatory crackdown in China, which has obliterated many of its technology giants and added to fears of an economic slowdown, the manager does not think Chinese equities are at risk of being a ‘value trap’.

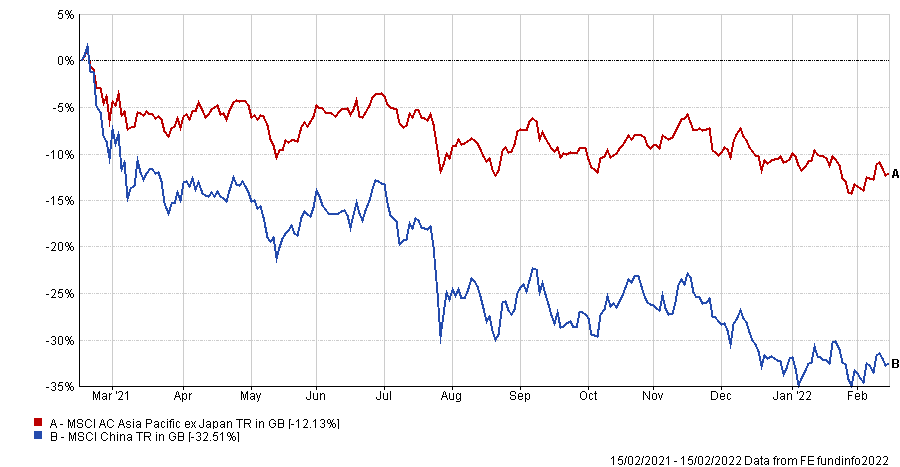

Over the past year, the broader Chinese index has been dragged down by its high weightings to stocks such as Alibaba and Tencent, who were the main target of the country’s regulatory crackdown of technology firms.

Investors have also been wary of an economic slowdown in China on the back of a shortfall in property investment after the country’s real estate market was rattled by the potential collapse of major property developer Evergrande late last year.

Performance of MSIC China v MSCI AC Asia Pacific ex Japan over 1yr

Source: FE Analytics

“I think right now, China is a really, really interesting opportunity because all the valuation excess has been shaken out,” Harriss said.

“China is a bit of a dirty word in the investment world, but that market is expected to grow about 9% per annum over the next couple of years.”

Although 9% growth for the overall Chinese equity index may not seem particularly strong on the surface in comparison to the double-digit growth investors have come to expect in recent years, Harriss explained that this number is being weighed down by some of the large-cap stocks in the market.

“What is interesting is that there are aspects of the Chinese market where growth is a lot quicker,” he said. “I think, as an investor, you're not well served by looking at it on an index basis.

“You've got a lot of growth coming through in the alternative energy space, you've got a lot in the EV [electric vehicle] space, you've got a lot in renewables and in industrial automation.”

Despite this, many global investors have now shunned the region entirely, with some labelling the country as ‘uninvestable’ due to the lack of protection for foreign investors and overwhelming power of the country’s political party over corporations.

There were a growing number of global funds that held China’s big technology giants like Tencent and Alibaba in their portfolios before the regulatory crackdown. Now only a handful of global equity mandates hold these former technology darlings.

However, the wild swings in sentiment surrounding investment in China is not something new, according to Harriss.

“China’s macro-economic management story, over the 27 years I have followed it, has been one of ‘squeeze and release’ with concomitant investor reactions of deep gloom to euphoria,” he said.

“At present, the view is one of gloom, which places China stocks firmly in value territory. The reality is that, while certain sectors and industries are financially weak, the economy is a whole is well capitalised and resourced.”

This bullish stance on China is reflected by Harriss’ Guinness Global Equity, a three FE fundinfo Crown-rated strategy, holding an overweight allocation to Chinese equities of 35.7% compared to 31.4% of the MSCI AC Asia Pacific ex Japan index.

But even so, Harriss noted that his Chinese equity exposure is vastly different to that of the index, which is still dominated by the large banks and technology companies.

He said: “We have a Chinese real estate developer with 30% net debt to equity, no credit squeeze and that can be a beneficiary of others’ misfortune.

“We have exposure to a textile maker that supplies Nike, Adidas and so forth, which has been investing in capital equipment over the past few years. So the labour is very productive, dividend is growing nicely, and profits are growing nicely.

“These are the areas where you can select and get some quite interesting ideas, and you can still find pretty decent growth – but you're going to get them at pretty attractive valuations.”

The next hurdle Chinese equities now face is the rising levels of inflation and potential squeeze from rising interest rates.

Harriss said: “The market is still wrestling with how on earth to value some of these growthier areas, which is I think much more of an art than science.”

The Guinness Asian Equity Income strategy follows a mix of quality and value investment approaches, with a focus on companies growing dividends.

“At least here I've got something I think that I can hang my hat on, so that when the market heads south – as it did in the first quarter of 2020 – I can still point to my companies making money and paying out dividends,” Harriss said.

“As investors move away from growth via earnings delivered out in the future – which are obviously going to be worth less in present value terms as interest rates start to rise – people are going to focus more on like the types of companies that I've got, where there is nothing priced in for growth.”