After years of US dominance, Europe emerged as a hotspot for capital in 2025, as investors began to broaden their horizons.

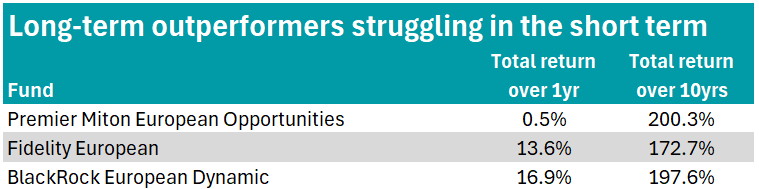

But not every European fund shared Europe’s resurgence, with three long-term leaders slipping into the fourth quartile as the market’s style rotation to value and cyclically exposed markets worked against them.

Source: FE Analytics

What links all three funds is a clear tilt towards quality – an investment style which has had a tougher spell over the past years as markets favoured more value-oriented areas.

A stalwart of the IA Europe ex UK sector, BlackRock European Dynamic is the largest fund in the table, with $4.9bn in assets. It has achieved top quartile returns in five separate calendar years between 2016 to 2026.

Its high-conviction portfolio of 35 to 65 stocks – currently led by names such as ASML, UniCredit and Siemens Energy – can cause short-term performance to diverge from peers.

Giles Rothbarth, manager of BlackRock European Dynamic, told Trustnet that 2025 was a quality bear market, meaning his preference for stocks with strong balance sheets, margins and cashflow profiles was punished, creating a dislocation between earnings and share prices.

“There have been three major periods over the past 30 years marked by a similar disconnect between prices and earnings,” he said.

“In each case, the subsequent return to active management was significant and outsized as fundamentals returned to the fore. We believe we are moving towards an environment that will provide strong potential for alpha.”

As such, Rothbarth said he is looking at the rest of the year with pragmatism and a continued focus on long-term drivers of return, “while also being mindful of the impact of near-term earnings – favouring those demonstrating resilience, cyclical recovery and idiosyncratic catalysts”.

Meanwhile, the £4bn Fidelity European fund has also delivered an impressive long-term record, compounding a 172.7% return over 10 years. However, its 13.6% gain in 2025 meant the fund slid to the fourth quartile.

Managed by Samuel Morse and Marcel Stotzel, the fund takes a disciplined bottom-up approach, typically holding 50 to 60 high-quality European stocks.

The managers target capital preservation, low turnover and rigorous downside analysis to deliver a 1% to 2% per annum outperformance with a smoother return profile than a market – an approach which may lag during sharp and speculative rallies.

Fidelity European also typically favours large-cap stocks, particularly those offering attractively-valued dividend growth, targeting sectors such as healthcare, consumer staples and financials.

Its defensive tilt helped it limit losses to 1.6% in 2022, delivering a top-quartile result during a difficult year for the sector.

A spokesperson at Fidelity International, said: “Over the year, fund performance was impacted by the market environment and style headwind, which has favoured cyclical value stocks following the fiscal stimulus announced by Germany.”

From a sector perspective, the healthcare sector has also been a detractor, the spokesperson said – largely because of exposure to Novo Nordisk. Materials and software holdings also weighed on results.

“We have been here before: it is important to emphasise that style-driven headwinds are temporary and historically these phases have averaged out positively over a three-to-five-year horizon,” the spokesperson said.

It was Premier Miton European Opportunities that delivered the weakest return of the three funds in 2025, gaining just 0.5% – although its return over 10 years is strongest at over 200%.

Similarly to the BlackRock fund, it has delivered five top-quartile calendar year returns between 2016 and 2026. However, the Premier Miton European Opportunities fund made a notable 22.1% loss in 2022, dropping to the fourth quartile.

The £646.7m fund has been co-managed by Carlos Moreno and Thomas Brown since 2015 and has a clear quality-growth bias and a strong mid- and small-cap tilt, with the latter currently making up around 45% of the portfolio.

Brown said: “We are very proud of our strong long-term track record but 2025 was tough – as with every year, even the very good ones, there were some individual stock-picking mistakes but the style bias was the dominant factor.

“High quality stocks underperformed the market by around 7% in 2025 and growth stocks underperformed value stocks by around 15%, which presented a very strong headwind.”

He added that last year’s headwind has “actually been blowing for around five years now and, while we are disappointed with the returns from our strategy over that horizon, we think this sets up a fantastic buying opportunity for some of the very high-quality businesses that we like to hold within the portfolio”.

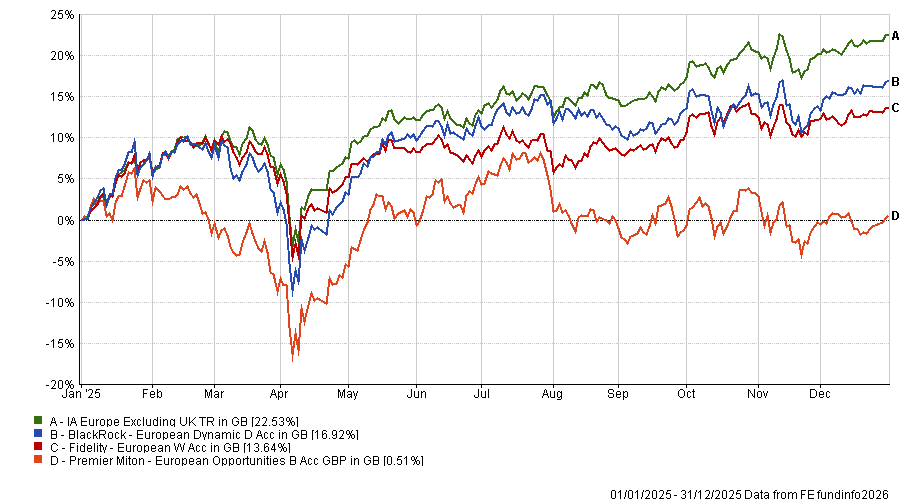

Performance of the funds vs sector in 2025

Source: FE Analytics

Which of the three funds is worth buying now?

All three funds still have a reason to be part of investors’ portfolios today precisely for their focus on quality, according to Darius McDermott, managing director at FundCalibre, who noted that one difficult year does not erase the strength of their long-term records.

“Delivering first quartile returns over a decade is no accident, reflecting experienced managers, disciplined stock selection and repeatable processes that have added value through multiple market cycles,” he said.

“In many cases, underlying earnings have continued to improve, yet share prices have lagged behind,” he noted. “From a risk-rewarded perspective, that disconnect creates compelling upside potential for patient investors willing to look beyond short-term noise.”

McDermott’s choice was Premier Miton European Opportunities, which would suit investors with a higher risk tolerance who are comfortable with sharper swings in performance in pursuit of greater upside over the long-term.

“It tends to be punchier and more volatile, so it will suit,” he said, adding that smaller and mid-cap companies still trade at meaningful discounts, leaving scope for further catch-up as sentiment and fundamentals normalise.

The other names are more suitable for other type of investors.

James Rowlinson, associate investment governance director at Forvis Mazars, picked BlackRock European Dynamic because it offers “a compelling way to access growth in what is structurally a low-growth region”.

Rowlinson highlighted Rothbarth’s “excellent” long-term track record and disciplined investment style built around identifying high-quality companies with durable, compounding earnings.

He added that the manager has responded proactively to recent market conditions, tilting towards companies with stronger near-term earnings visibility and businesses with more defensive, cash-generative profiles.

“This reflects a pragmatic rebalancing while remaining true to the fund’s long-term quality growth philosophy,” Rowlinson said.

“Overall, we believe this strategy remains well aligned with our view of Europe: a region with modest trend‑growth where investors must be selective.”

Finally, Gill Hutchison, research director at the Fund Research Centre, said she leans toward Fidelity European, given its demonstrated ability to protect capital in weaker markets.

“We suspect [Fidelity European] would be the initial beneficiary of a more cautious tone in markets, given its exposure to defensive growth sectors,” she added.