Gold has been on a hot streak in recent years as geopolitical instability, equity valuation concerns and lower interest rates have created a near-perfect storm for the precious metal.

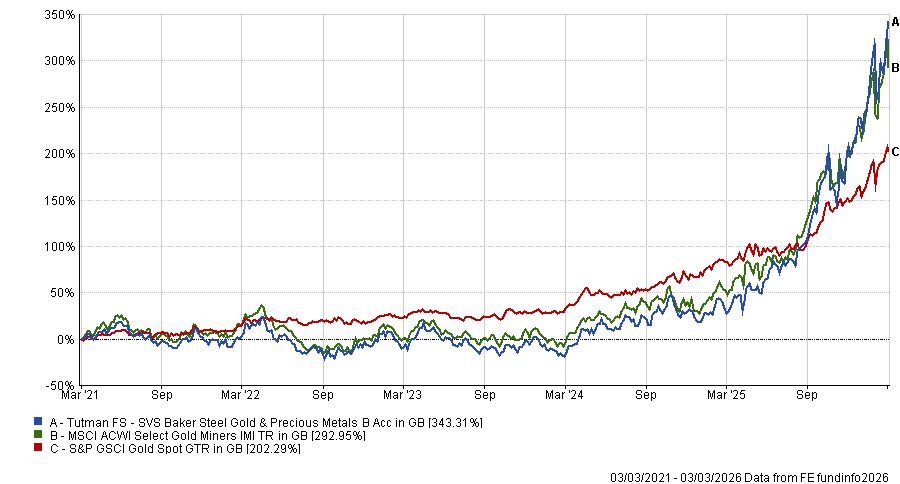

The metal has tripled investors' money over five years, up 211.7%, but there has been an even quicker way to make meteoric gains: investing in miners.

SVS Baker Steel Gold & Precious Metals invests in global precious metal miners and has achieved a 243.9% return in just 12 months. Over five years, the fund is up 343.3%, more than 100 percentage points above the gold spot price.

Performance of fund vs benchmark and gold spot price over 5yrs

Source: FE Analytics

But despite this phenomenal run, director of market strategy Cosmo Sturge believes there is still plenty of room to run for gold and precious metal producers.

Miners tend to lag the gold spot price on the way up by around six months as investors wait for higher prices to feed through into company profitability.

Despite strong share price gains, he said that valuations remain relatively undemanding, noting that most major gold miners trade on a price to net asset value (NAV) of around 0.7x.

This is below both the long-term average of 0.8x and almost half of the previous cyclical peak in the late 2000s of 1.4x.

“We’re confident they're still not stretched in valuation terms,” he said, noting that miners are currently using a price in the $3,000-$4,000 range rather than the current spot price of $5,000, suggesting there could be further upside if they start to view the spot price as entrenched.

As such, gold does not need to move from its current level for miners to keep outperforming the wider market, he said. In fact, if the price stays the same, this would still be “fantastic” for metal producers, as the all‑in sustaining cost of mining an ounce of gold is somewhere around $1,600 to $1,800.

“Even if gold traded sideways in its current range, [miners] would be printing money, delivering very strong quarterly results and continuing buybacks,” said Sturge.

The gold price is hard to predict but there are factors that give Baker Steel confidence that it is well supported currently.

First is the “wide variety of investors” in gold, including central banks, financial institutions, family offices, retail investors and consumers, who are buying jewellery despite higher prices.

“Physical gold ETF flows only really started picking up midway through last year, which was a really strong lift,” he said. “Prior to that, there’d already been a year’s worth of gold rally as it was central banks and globally diversified mixes of family offices and retail investors and high‑net‑worth individuals accumulating physical gold.”

“The key for us is the return of Western investors, who tend to move both physical gold and gold‑mining equities. We think that’s only just starting,” he said, noting that Western investors had been selling gold and ignoring miners in the past few years, choosing to take profits.

Despite its strong run, gold has been more muted recently and suffered a leg down at the start of the year when US president Donald Trump nominated Kevin Warsh as the next Federal Reserve chair.

Markets viewed the nominee as more hawkish, something Sturge described as “nonsensical” given the president’s desire for lower interest rates.

Gold should therefore remain supported from a monetary policy perspective too. Historically, he noted, the precious metal hits its peak after the rate-cutting cycle has concluded.

“If you look at the Fed’s dot plot and consensus – a downward slope in rates – gold has not yet hit its cyclical peak,” he said.

Gold thrives in periods with persistent inflation, doubts about policy effectiveness and high geopolitical tension. That was true in the 1970s, the 2000s, and early 2010s, all multi-year bull cycles when gold rose 100–400%.

“Since mid‑2024, gold has risen about 170% so, in our view, we’re probably midway through a normal bull cycle. We’re not putting targets on it, but historically this would imply significant room left.”