Emerging markets have been on a rollercoaster ride this year, as initial momentum has been hampered by the closure of the Strait of Hormuz – a key trade route especially for oil destined to Asia.

Amundi has held back from re-entering emerging markets despite seeing a compelling opportunity, as uncertainty forces a rethink of how risk is deployed across multi-asset portfolios.

Francesco Sandrini, head of multi asset at Amundi, said the team was “very tempted” to increase exposure to emerging market debt during the recent correction but ultimately decided to wait, as “uncertainty is at its peak”.

Spreads across credit markets, including emerging markets in both hard and local currency, have compressed significantly, leaving valuations broadly expensive. While Sandrini said emerging markets still look “a little healthier” on a relative basis compared with US and European high yield, that alone was not enough to justify deploying additional risk.

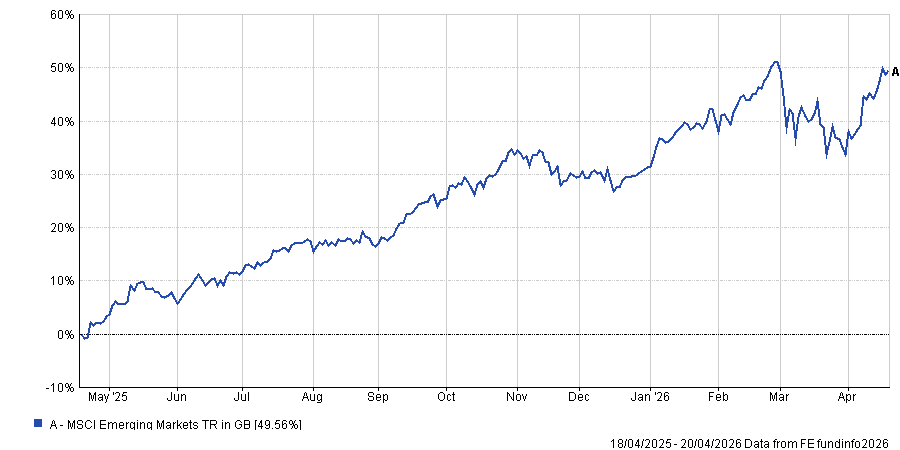

Performance of index over 1yr

Source: FE Analytics

Instead, the team chose to “spend the risk budget in spreads differently”, reallocating towards European investment grade and selected government bond markets where dislocations appeared more attractive. Italian government bonds, for example, have widened more than emerging market debt, offering what Sandrini described as a clearer opportunity for a “cooling down”.

Before the recent escalation in geopolitical tensions, Amundi favoured emerging market local currency debt, underpinned by the view that the US dollar would weaken over time.

“We are tempted to go back,” Sandrini said, because the structural case for the area remains intact. However, the current environment makes it challenging.

“In these days the US dollar is one of the few asset classes that has been working,” he continued, noting that periods of heightened volatility tend to drive simultaneous declines across equities and fixed income, undermining diversification within multi-asset portfolios.

This dynamic, where “you are falling twice”, has made it harder to express pro-risk views, particularly those tied to dollar weakness. The risk of another spike in the US currency, combined with only modest widening in emerging market spreads, has reinforced the decision to wait for clearer conditions before rebuilding positions.

Beyond emerging markets, Amundi has leaned into carry opportunities within developed markets, particularly in Europe. Sandrini said the recent repricing in interest rate expectations has created opportunities within short-term maturities.

Markets are currently pricing up to three rate hikes from the European Central Bank this year. “We think this expectation is excessive because central banks will tend to wait, look through and expect resolution,” he said, believing that policymakers are unlikely to respond aggressively to a supply-driven inflation shock.

This has led Amundi to increase duration exposure in the two-year segment of the German curve, where higher yields offer both carry and the potential for capital gains if rate expectations are scaled back.

“The longer it takes to stabilise, the higher the probability the ECB considers one or possibly two hikes as a preventive move,” Sandrini said, but added that central banks have learned from previous episodes and are likely to avoid measures that could further weaken already fragile growth.

In equities, the firm has also become more cautious as the market recovery matures. Sandrini estimates that markets are “70–80% through the recovery process”, prompting a reduction in strategic allocation while maintaining a tactical long position.

Even after the renewed closure of the Strait of Hormuz, markets still believe in a reconciliation.

Amundi’s positioning has been adjusted to reflect this shift. Exposure to Japan and Europe has been trimmed, while the US remains the primary allocation, alongside selective positions in markets such as Brazil. At the same time, hedging activity has increased, with the team adding protection when volatility falls to more attractive levels.

“We are increasing hedges opportunistically and selectively taking profits,” he said.

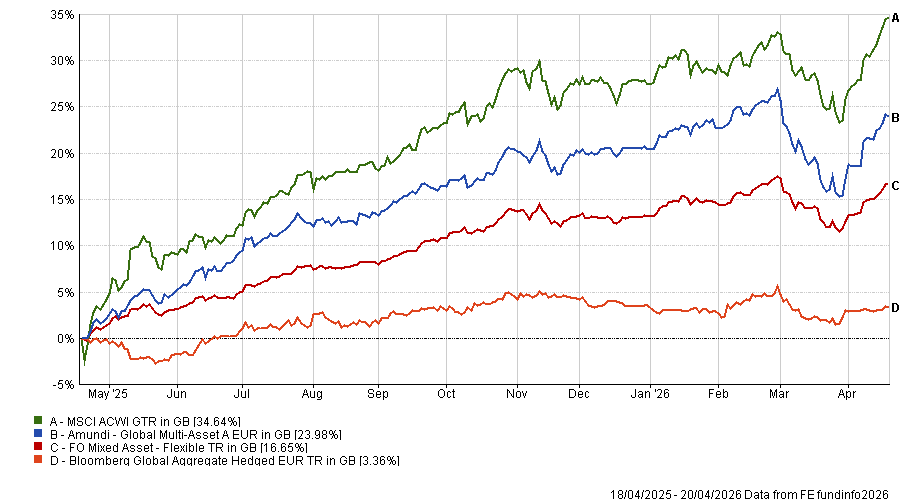

Performance of fund against index and sector over 1yr

Source: FE Analytics

Sandrini highlighted the UK as a useful component in multi-asset portfolios, as it has behaved differently from other developed markets in recent months.

“The UK has been quite interesting,” he said, describing it as “a good diversifier” that has benefited from distinct flow dynamics relative to Europe, particularly gilts.