Over the past decade, Japan’s equity market has been shaped by a mix of slow-moving structural reforms and bouts of yen volatility.

To identify which funds have outperformed in this landscape most consistently, Trustnet has compared the discrete annual returns of IA Japan funds against one of the sector’s most used benchmark – Topix – between 2016 to 2025.

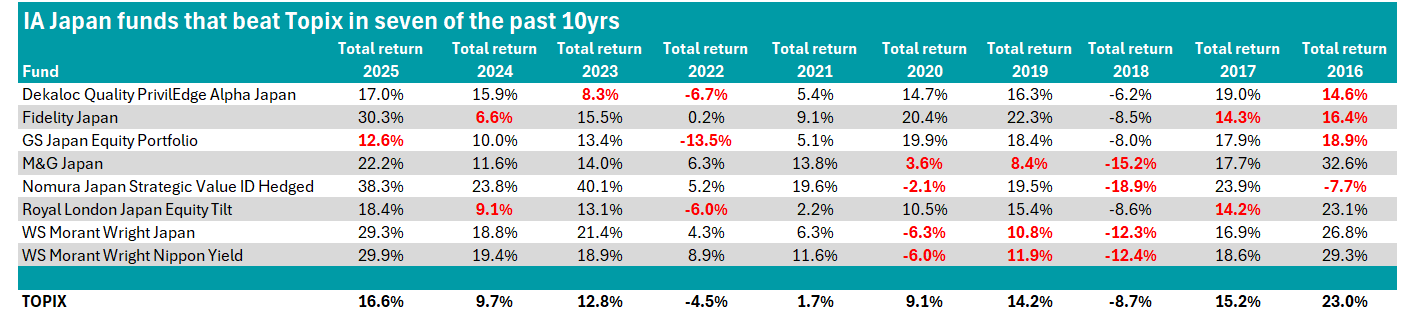

As shown in the table below, eight actively managed funds beat the index in at least seven calendar years.

Source: FE Analytics. Figures highlighted in red represent years in which a fund underperformed Topix.

While all eight of these funds are just as consistent as each other, their paths to achieving this track record look very different.

For example, Nomura Japan Strategic Value ID Hedged, Fidelity Japan and WS Morant Wright Nippon Yield posted the strongest returns in the IA Japan sector in 2025, gaining 38.3%, 30.3% and 29.9% respectively, while GS Japan Equity Portfolio languished in the fourth quartile. It had a much better year in 2020, posting a first quartile return of 19.9%.

Yet a contrasting picture emerged in 2018, with Japanese equities ending the year broadly flat after a volatile year driven by global trade tensions and erratic foreign investor positioning. Every fund in the table (and the sector) made a loss – bar Lindsell Train Japanese Equity, which gained 2.1%.

However, Dekaloc Quality PrivilEdge Alpha Japan offered the best downside protection among the funds in the table that year, followed by GS Japan Equity Portfolio, while winners in 2025 struggled.

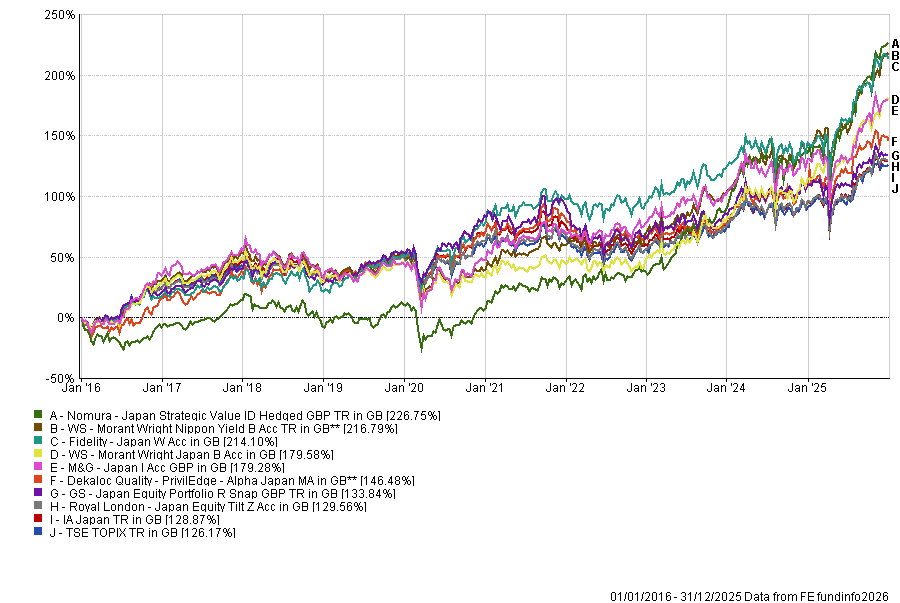

Nonetheless, over the full decade, the Nomura strategy posted the strongest 10-year return of the funds in the table, gaining 226.8%.

The £2.3bn fund has been one of the standout performers in the sector, delivering a top three return in 2021, 2024 and 2025 and topping the entire sector in 2023.

Although involved in the strategy since 2005, Yoshihiro Miyazaki became lead manager in 2021, taking over from former manager and architect of Nomura Asset Management’s Japan Strategic Value strategy Kentaro Takayanagi.

The quantitative approach involves employs a quality-value tilt, with prospective investments assessed on their price-to-book ratio, earnings yield based on three-year estimates and a merger & acquisitions (M&A) ratio showing the cost to acquire the company relative to operating profit. A prospective stock needs to be undervalued on at least one of these metrics relative to the market average to pass the filter.

Fund Research Centre recommends the fund, noting that is an “all-weather strategy”.

Analysts added: “The fund is suited to those who are seeking a relative value approach in Japanese equities. It could be used as a mainstay exposure to the asset class in a portfolio, provided there is some tolerance for performance variability.”

Earlier this year, Nomura Japan Strategic Value was highlighted for its consistent performance over three consecutive calendar years and it has also beaten MSCI Japan over the five years from 2020.

Of the funds in the table, Fidelity Japan has delivered a first-quartile return in the most years – in six of 10 – including in 2019, when it was the only fund in the table to do so.

It also delivered a first-quartile return in the sector in 2020, alongside GS Japan Equity Portfolio, while other funds in the table – including the Nomura strategy – languished in the fourth quartile.

The Fidelity fund invests across market capitalisations and sectors without being constrained by a benchmark, although its current top holdings include well-known large-caps like Mitsubishi and Toyota.

It has been managed by Min Zeng since 2022, following the retirement of longstanding manager Ronald Slattery.

WS Morant Wright Nippon Yield was another of the sector’s regular outperformers, with other stand-out years including 2022 – a year in which it posted the second-best return in the sector with an 8.9% gain.

The £1.1bn fund, launched in 2010, also holds an FE fundinfo Crown Rating of five.

Square Mile analysts said the strategy typically exhibits a high tracking error to any benchmark, “however, this is not targeted or monitored”.

It tends to be underweight areas such as information technology, healthcare and consumer staples due to valuation sensitivity, and has generally outperformed its sister strategy, WS Morant Wright Japan.

The strategy is one of the more expensive options in the table, with an OCF of 1.18%, but it has also been recognised for producing a top-quartile Sharpe ratio in seven out of 10 years.

Another fund worth mentioning is the £5bn M&G Japan, which delivered the best return in the table in 2016 and second-best in both 2021 and 2022.

Managed by Carl Vine since 2019 and supported by FE fundinfo Alpha Manager Dave Perrett, the strategy is built around deep fundamental research and detailed modelling to identify mispriced opportunities. Former manager Johan du Preez departed the firm in 2019 after 21 years.

The management team focuses on understanding downside risk and often buys on weakness and trims on strength, with the portfolio typically holding around 45 names with position sizes of between 1-5% active weight.

RSMR analysts noted that “relative performance could struggle in the short term when the market is totally focused on growth stocks to the exclusion of everything else”.

It is also one of the cheaper options in the table, with an OCF of 0.47%.

Performance of the funds vs sector and benchmark, 2016-2025

Source: FE Analytics

Although these active funds stood out over the decade, they were not the only strategies to show consistent strength.

Two exchange-traded funds (ETFs) also beat Topix in seven years: iShares Nikkei 225 UCITS ETF and Xtrackers Nikkei 225 UCITS ETF.

However, this outperformance should be taken with a pinch of salt. Passive funds are designed to replicate the performance of their chosen index as closely as possible – in this case, both ETFs are tracking the Nikkei 225, rather than the Topix used in this research.