James Bullock has been adding to business software company Intuit despite it being the Lindsell Train Global Equity fund's worst performer in June, arguing the market's punishment of 'AI loser' stocks has run well ahead of the actual risk to their businesses.

Bullock's fund lost 1.5% in June, against a 0.8% gain for the MSCI World index, leaving it 10.8% behind the benchmark over the second quarter. He attributed the shortfall to the fund's exposure to companies that markets have labelled 'AI losers', a group that includes software and information services businesses like Intuit.

Outside of Alphabet, Lindsell Train Global Equity holds almost nothing in the semiconductor, memory and energy names widely seen as AI's beneficiaries.

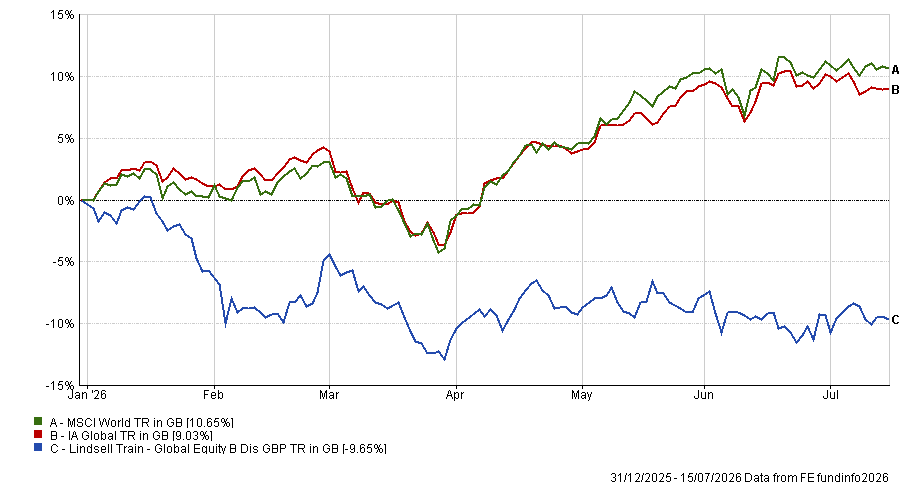

Performance of Lindsell Train Global Equity vs sector and index over 2026 so far

Source: FE Analytics. Total return in sterling between 1 Jan and 15 Jul 2026

The AI rollout and its potential impact have dominated stock markets in recent years, with investors weighing up if companies are likely to be winners of the AI buildout and adoption or losers that find their business models disrupted.

Companies like Intuit, RELX and London Stock Exchange Group have been put in the AI loser camp by some on the view that their customers will replace their proprietary data and tools with AI. However, Bullock argued that these companies' unique datasets and intellectual property means they are "likely to avoid the sort of black swan tail risks that AI arguably heralds", even if the market currently disagrees.

"But whilst the risk is not, and never has been, zero, Mr Market's newfound ability to conceptualise it (however unlikely) is becoming a self-fulfilling prophecy. If you take the view (I suspect commonly held and arguably supported by the continued success of the 'momentum trade') that share prices contain insight, then falling prices can quickly spiral into a vicious cycle; whereby a weak share chart implies a broken business model, more downward pressure and so on," he said.

"The difficulty of disproving a negative thesis (how do you refute an assertion made without evidence?) and the much-discussed rise of passive (massive, price-insensitive flows that polarise and build momentum) perpetuates both the narrative and trend."

Intuit is the clearest example in his portfolio. Its shares fell 21% in US dollar terms in June alone, leaving them down nearly two-thirds from last year's highs.

That repricing has pushed Intuit's free cashflow yield from around 2.5% in 2025 to more than 10% now. Management still guides to earnings-per-share growth of 16-18% next year, yet the shares trade on a forward multiple of just 11 times non-GAAP earnings.

Despite this, investors continue to avoid the stock, which Bullock suggested is a behavioural problem: "The fear of being wrong (always possible I'm afraid) has a much sharper sting if consensus already told you so. It's said that it's better to fail conventionally than succeed unconventionally. Perhaps, but to fail unconventionally is surely the most painful of all and many investors will avoid this at all costs.

"Even if, at the current price and risk, the balance of probabilities skews heavily in your favour, the reputational damage of 'getting it wrong' is simply too distasteful – no matter how unlikely, or how attractive, the rewards for being right."

Lindsell Train Global Equity has held Intuit since its launch in 2011, alongside RELX and London Stock Exchange Group. All three have delivered strong long-run returns (total annualised sterling returns of 14%, 14.1%, and 18.6% respectively) despite recent falls in perceived value.

"In our view, these are exceptional companies in strong industries and, given our heritage and experience investing here over the decades, we feel in a good position to walk where others fear to tread, to take advantage of historically attractive valuations," the manager said.

Intuit's own management appears to share that confidence, with the company spending around $1bn a quarter on share buybacks, a rate that now equates to a buyback yield of close to 7%, at a valuation Bullock considers detached from its growth guidance.

Bullock's position is not shared by every quality-growth manager. Fundsmith Equity sold out of Intuit entirely in the first half of 2026, replacing it with accounting software rival Sage. Rathbone Global Opportunities also exited Intuit this year, as part of a wider move away from consumer-facing software and information services names on concerns about AI-driven competition.

For Bullock, buying into weakness means accepting a trade-off between price and probability, while tolerating the discomfort of looking wrong until the market agrees otherwise. He has extended this approach beyond Intuit, adding to RELX, LSEG and FICO in 2026 and starting two new positions he has not yet named, both roughly halved in share price from last year's highs.

"It's important to emphasise that we won't change our portfolios without strong cause, and even here we are talking about low-single-digit turnover. However, as with the additions of Alphabet and Games Workshop in April 2025, the extreme volatility evident so far across 2026 has created opportunities we'd be remiss to ignore," he finished.