Semiconductors have been the latest beneficiaries of the AI trade as TSMC in Taiwan and SK Hynix in Korea have rocketed higher in 2026.

For Stonehage Fleming Global Best Ideas Equity fund manager Carolyn Bell and her deputy Prandhana Naidu, this has been one of the biggest detractors to performance.

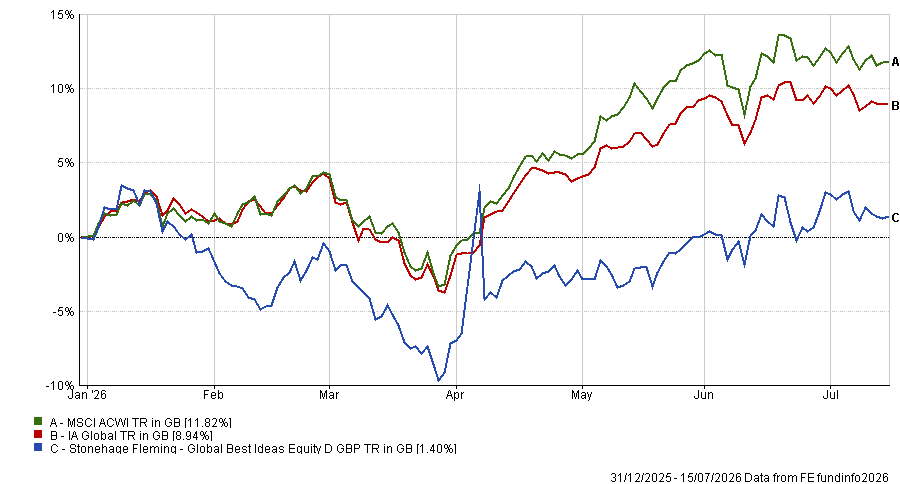

Indeed, the £1.3bn portfolio has been a bottom-quartile performer in the IA Global peer group over the past six months. Bell took charge in April 2026, although she has worked on the fund since 2024.

Performance of fund vs sector and benchmark YTD

Source: FE Analytics

“Could everybody start looking at something that doesn't make semiconductors, because that's all anyone's been looking at. Reassess what you're getting the opportunity to buy now,” she said.

“We're in a cycle. The semiconductor industry will certainly be bigger than it was, but we don't think the rate of growth in the semiconductor industry can continue into perpetuity. At some point, the infrastructure build-out will be past its peak.”

There has been a shortage of memory chips, which has allowed certain companies that Stonehage Fleming Global Best Ideas Equity does not invest in to outperform. But this won’t last forever, warned Bell.

Currently, these stocks have pricing power as there is not enough supply to meet the rapidly increasing demand, but investors need to be careful when investing in a near-to-medium-term shortage.

“We may be better off investing in businesses that will benefit over the long term from a much bigger semiconductor industry and that aren't moving so much on pricing, which is a bit unpredictable,” she said.

“That's why the equipment names are better long-term holdings for us. I think they're higher-quality names and actually more durable.”

That is not to say the fund does not own companies involved in the AI trade. Below, Bell and Naidu explain how ASML has been the fund’s top holding over the past year, why it doesn’t invest in energy or property and why the managers can’t believe Mastercard is so cheap.

What is your process?

CB: It's very much a quality-growth fund. We have four pillars that keep us on track. One of which is organic growth: we're looking for sustainable competitive advantage in every stock.

Then strong management, evidenced through historic capital allocation, efficiency (strong margins) and a strong balance sheet with lots of free cashflow generation.

Is there anything you don’t invest in?

CB: We don't target any sector allocation but we don't usually find opportunities in real estate because it's so driven by interest rates, and we don't usually find opportunities in energy, because it's so driven by the oil price, which isn't something any individual company can control.

We're trying to harness businesses that can, as much as possible, control their earnings growth. They are quite rare.

Why has Stonehage Fleming Global Best Ideas Equity struggled in recent years?

CB: The issue has been the style rotation. We're not anomalous in our underperformance in the past couple of years versus our peers in quality-growth.

We don't stray into growth or value just because those areas are working; we're not momentum led. It's really important that investors have a diversified portfolio and that their quality-growth managers are genuinely quality-growth.

What have been your best and worst performers over the past year?

PN: Our best performer in absolute terms was ASML, the semiconductor equipment company, which was up 149% in the 12 months to the end of June. ASML’s performance really accelerated in the past six months as AI capex commitments from hyperscalers and memory companies underpinned the growing demand for AI chip production. Alphabet has been another very strong performer for us, up 99%.

Our worst performer has been Netflix (down 46% to end June). It has been weak on the failed Warner Bros Discovery bid, co-founder Reed Hastings stepping down from the board and questions on engagement levels impacting sentiment. Content slate, content costs and engagement levels are important metrics we are tracking closely.

Is there a company you believe is mispriced?

CB: I shout about Mastercard because it looks so cheap to me for the strength of the business and the earnings power it has. It actually sold off on the Iran war, because cross-border revenues matter to it, so travel matters.

It's just super cheap to me. It is genuinely cash-generative, has a right to win and is basically in a duopoly. It's been a superlative performer over the period since it came to market and right now it is in the portfolio on 23x forward earnings. You hardly ever get the opportunity to buy it at that level.

What do you do outside of fund management?

CB: My passion is the Renaissance. I've got my degree in English, and then a master's in early modern studies. I started a PhD in Shakespeare, which I abandoned to go into fund management – I still feel a bit guilty about that. Also, I've got two kids – I love them too, I probably should have started with them.

PN: I'm quite a foodie. I've got one child, a daughter, and she's into it too. She’s got a very exquisite palate. So we at least attempt, on the weekends, to do something culturally different. We combine that with travel.