Past performance does not predict future returns. You may get back less than you originally invested. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

This article is featured in the Q1 2026 Future Strategist newsletter, you can read the rest of the newsletter here.

The outlook for emerging markets (EM) coming into 2026 was constructive. The International Monetary Fund’s (IMF) January update saw it upgrade its projection for global growth this year, supported by moderating inflation, technology investment and easing fiscal and monetary policies. Along with a weakening US dollar, the macro backdrop was one that typically favoured EM outperformance over Developed Market (DM) counterparts. Historically, Latin America and Eastern Europe have been the biggest beneficiaries of a weaker dollar, and these markets were outperforming through 2025, along with North Asia where South Korea and Taiwan were benefitting from the memory upcycle and global AI capex buildout.

The war in Iran has altered this benign global environment. The Strait of Hormuz has been effectively closed with the IEA (International Energy Agency) calling it the largest supply disruption in the history of the oil market. Disruption extends beyond energy markets, with a third of global seaborne fertiliser trade also impacted, having consequences for agricultural production globally. While US efforts are now focused on reopening the Strait, the risk of ongoing interference by Iran and the challenges in securing insurance for ships suggests that disruption is likely to remain for some time. Oil prices have eased back but remain around $100 even as hopes have risen that Trump can secure an off-ramp and make a deal. Even if the Strait of Hormuz were to reopen tomorrow, shipping traffic would not return to pre-war levels for an extended period of time, and with ongoing damage to energy infrastructure across the region supply will not be able to return to prior levels as it will take months to ramp up oilfields after production shut-ins.

This matters for EMs as inflation expectations influence monetary policy. Higher oil, gas, fertiliser and freight costs slow the disinflation process and reduce central banks’ capacity to keep cutting rates, particularly in countries significantly dependent on imports. However, EMs are more resilient now than heading into previous crises. The IMF argues they are now able to weather shocks better than in the past, with smaller capital outflows, more contained borrowing costs and stronger policy frameworks; it also stressed the role of larger reserve buffers in limiting FX volatility. Importantly, the dollar’s response as a safe haven asset has been less pronounced than might have been expected. As and when the war concludes, the dollar’s bounce could prove short-lived as the Fed resumes easing, and concerns remain over the US fiscal backdrop and policy uncertainty, compounding doubts over the safe haven appeal of US assets.

The medium-term case for EM remains intact, although the shorter-term impacts will vary widely, with energy importers in Eastern Europe and much of Asia facing a more difficult inflation/interest rate trade-off, while exporters and those with stronger external balances and more credible policy frameworks should prove more resilient and, in some cases, stand to benefit. This would otherwise have been the Gulf exporters but, given their proximity to the conflict, it is Latin American countries like Brazil, Colombia and Mexico that are seeing energy exports cushion the impact of higher prices.

Beyond the immediate macro shock, the war also reinforces a broader market shift already underway. In recent months, the market had already been embracing the HALO trade (heavy assets, low obsolescence) as investors reassessed the vulnerability of software and other asset-light business models in the world of AI. The war in Iran strengthens that shift – it reinforces the premium on physical capacity, supply chain security and national resilience, particularly in industries tied to energy, infrastructure, logistics, defence and critical materials. It may also accelerate parts of the energy transition, as governments place greater weight on renewables, grids, storage and efficiency as tools of energy security as much as decarbonisation.

At the same time, governments and companies are increasingly less willing to rely on just-in-time global supply chains for strategically important inputs, suggesting a world of structurally higher capital intensity and, in selected sectors, higher precautionary inventory holdings. This is supportive not only for heavy asset businesses, but also for parts of the commodity complex and the industrial supply chain that underpin energy security, rearmament and domestic manufacturing resilience. This favours EM because many of the beneficiaries of a world that increasingly values physical capacity, resource security and capital intensity, from commodity producers to manufacturers embedded in strategic supply chains, sit in EMs rather than DMs.

The long-term case for EM remains compelling; after more than a decade of underperformance vs DMs, EM equities still trade at a significant valuation discount (the end of 2025 discount was near its highest level since 2004 on both P/E (Price-to-Earnings) (35%) and P/B (Price-to-Book) (45%)). The asset class has spent years out of favour and is now moving into a period in which several important tailwinds are beginning to align: a weaker dollar, stronger resilience to external shocks, the North Asia technology cycle, supply-chain reconfiguration, and a greater premium on physical assets, strategic commodities and industrial capacity. This does not remove the near-term pressures created by the war, but it does suggest that the current disruption is more likely to reinforce differentiation within EM than to derail the medium-term story for the asset class as a whole.

MSCI EM discount to MSCI DM (forward P/E)

Source: Bloomberg, April 2026.

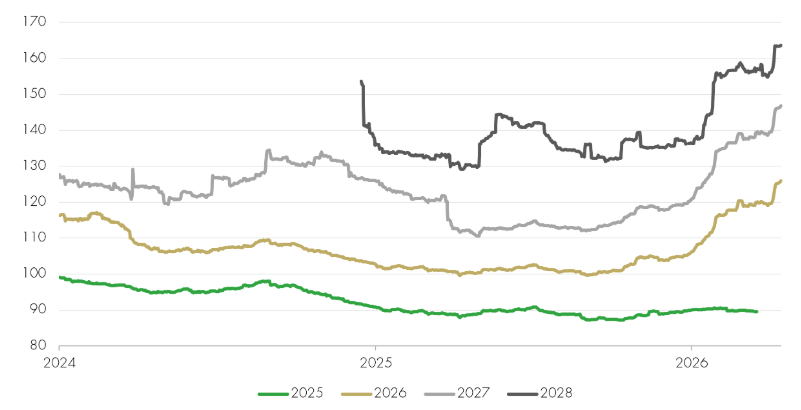

EM Earnings estimates being revised sharply higher

Source: Bloomberg, April 2026.

Read, watch and listen to more insights from Liontrust fund managers here >

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

The Funds managed by the Global Equities Team:

-

May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund.

-

May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings.

-

May invest in smaller companies and may invest a small proportion (less than 10%) of the Fund in unlisted securities. There may be liquidity constraints in these securities from time to time, i.e. in certain circumstances, the fund may not be able to sell a position for full value or at all in the short term. This may affect performance and could cause the fund to defer or suspend redemptions of its shares.

-

May have a concentrated portfolio, i.e. hold a limited number of investments or have significant sector or factor exposures. If one of these investments or sectors / factors fall in value this can have a greater impact on the Fund's value than if it held a larger number of investments across a more diversified portfolio.

-

May invest in emerging markets which carries a higher risk than investment in more developed countries. This may result in higher volatility and larger drops in the value of a fund over the short term.

-

Certain countries have a higher risk of the imposition of financial and economic sanctions on them which may have a significant economic impact on any company operating, or based, in these countries and their ability to trade as normal. Any such sanctions may cause the value of the investments in the fund to fall significantly and may result in liquidity issues which could prevent the fund from meeting redemptions.

-

May invest in companies predominantly in a single country which maybe subject to greater political, social and economic risks which could result in greater volatility than investments in more broadly diversified funds.

-

May hold Bonds. Bonds are affected by changes in interest rates and their value and the income they generate can rise or fall as a result; The creditworthiness of a bond issuer may also affect that bond's value. Bonds that produce a higher level of income usually also carry greater risk as such bond issuers may have difficulty in paying their debts. The value of a bond would be significantly affected if the issuer either refused to pay or was unable to pay.

-

May, in certain circumstances, invest in derivatives but it is not intended that their use will materially affect volatility. Derivatives are used to protect against currencies, credit and interest rate moves or for investment purposes. The use of derivatives may create leverage or gearing resulting in potentially greater volatility or fluctuations in the net asset value of the Fund. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead.

The risks detailed above are reflective of the full range of Funds managed by the Global Equities Team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.com or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

Understand common financial words and terms See our glossary