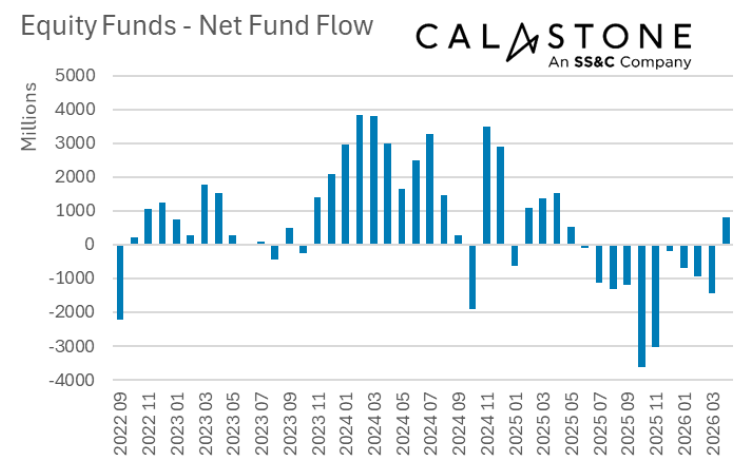

UK investors returned to equity funds in April 2026 for the first time in almost a year, Calastone’s latest Fund Flow Index shows, but the rebound was narrow.

Investors added a net £1.1bn to equity funds in April 2026, ending a record 10-month selling streak, but the recovery masked a sharply divided picture in which the Middle East conflict and its asymmetric effect on global markets determined where money flowed.

The return to equities was the first since May 2025 and made last April the best month for inflows since April 2025. Between June 2025 and March 2026, UK investors had pulled money from equity funds every single month, a run without precedent in Calastone’s data.

Source: Calastone Fund Flow Index – Apr 2026

However, investors were selective last month: US equity funds took in £1.1bn and global equity funds, which are predominantly US-exposed, attracted £1.3bn. Every other regional category recorded net outflows.

Asia Pacific was the hardest hit, with investors withdrawing £383m. Emerging markets saw outflows of £355m and European equity funds lost £104m.

UK-focused equity funds also saw net selling of £342m, although Calastone noted this was the best result for UK-focused funds since December 2024, when flows were distorted by the aftermath of UK budget speculation.

Edward Glyn, head of global markets at Calastone, said the regional pattern reflected the uneven economic consequences of the ongoing Middle East conflict.

“The war in the Middle East has strangled energy and feedstock flows to large parts of the world – leaving US supplies largely intact, even if prices are higher,” he said.

“The expected economic fallout means that Asia and Europe - the worst affected regions - saw stock markets either flat or down during April. The gloomy outlook drove outflows from funds invested in most parts of the world.”

The US stock market surged by almost 10% in April after softer economic data brought forward investor expectations for Federal Reserve interest rate cuts. That shift lifted rate-sensitive large-cap technology companies disproportionately, though Glyn cautioned that the broader earnings picture remained uneven across sectors.

Glyn added that the rally’s foundations were narrower than the headline gain suggested: “The rally still looks narrow, with a small group of large-cap names doing most of the work, but it was strong enough to pull flows back into US and global equity funds, where US exposure typically dominates.”

The concentration in US equities was matched by a concentration in index funds. Investors added £2.6bn to passive funds during April while selling £1.5bn of active funds.

The resulting £4.2bn gap in favour of passive was the third largest in Calastone’s records.

Glyn said: “For momentum investors, simply buying index funds makes sense, which helps explain the particular skew to index funds in April.”

The return to equities appeared partly funded by withdrawals from safe-haven money-market funds.

Investors had added £3.8bn to money market funds across the 10 months of equity outflows between June 2025 and March 2026. But in April, they pulled £671m from this fund category, a withdrawal that coincided with flows to equities turning positive for the first time in almost a year.

Fixed income flows also stabilised. Outflows from bond funds were negligible at £27m in April, a significant improvement on March’s larger shake-out, as higher yields began attracting new buyers.