A period of stagflation would be “the worst of all economic outcomes” for markets, according to experts, as they warned rising unemployment could lead to an inflation plateau.

Since the initial vaccine announcement in early November, markets have been forecasting a period of inflation following a the economic recovery from Covid-19.

This appears to be the case, with central banks communicating they are willing to let economies run ahead of its average inflation targets. The Bank of England’s current rate of inflation is 2.5% for example, an increase on the previous month. This is the highest it has been since pre-pandemic and ahead of the 2% target.

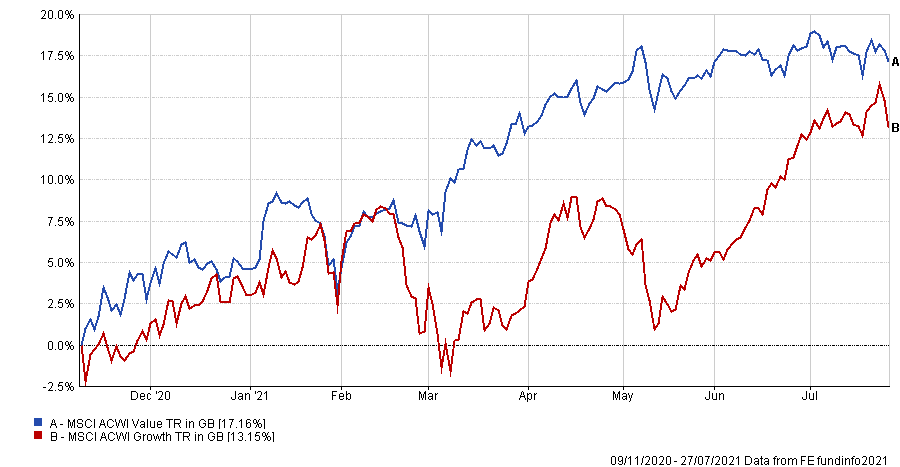

Combined with a period of economic recovery and growth as countries reopen post-lockdown, this has been an ideal environment for value stocks and sectors, which have led markets since ‘Pfizer Monday’ last October.

Performance of MSCI ACWI Value vs MSCI ACWI Growth since Pfizer Monday

Source: FE Analytics

But what if instead of inflation, markets entered a period of stagflation – when economic growth slows in conjunction with higher unemployment and rising prices.

Some believe this is possible, as UK unemployment is on the rise. Currently one in 20 people who want a job cannot fine one, according to latest Office for National Statistics (ONS) data.

This is higher than at the start of the pandemic and despite the government’s furlough scheme aiming to preserve jobs during the lockdowns, some people still face unemployment once the scheme ends in September.

Laith Khalaf, analyst at AJ Bell, said stagflation was probably the “worst of all economic outcomes for financial assets,” as rising prices without the overhead of economic growth to support company earnings would be problematic.

In a stagflation environment Khalaf said: “I would expect all stocks to come under pressure.”

Rob Morgan, pension and investment analyst at Charles Stanley Direct, added that stagflation would be both a tricky and unhappy scenario for both growth or value.

In this environment investors would need some short-duration assets where the reward or payoff in terms of cash flow was front-end loaded rather than much further away. These cash flows can increase in line with inflation, owing to pricing power, he explained.

Alternatively investors could hold inflation-linked assets such as inflation-linked bonds, some infrastructure assets or ‘real’ assets such as gold as well as certain selected property, which all are less affected by inflation.

Not all agreed, however. Ben Yearsley, Fairview Consulting director, said if stagflation was to occur it would have a greater impact on value stocks than their growth counterparts.

Without that economic growth cyclical assets would have “nowhere to go”, according to Yearsley, and would therefore stagnate.

These companies would have no pricing power and a “double whammy” of lower demand and higher costs, Yearsley said.

He added that things could be different for banks - a value stock staple - because they could increase interest rates. But this was unlikely due to the significant debt in the global economy.

Value fund manager, Liam Nunn member of the Schroders Value team, disagreed with this forecast, arguing that the outperformance of value stocks was not just tied to economic recovery, rising inflation or interest rates.

This is a misconception, Nunn said, adding that the “myth” around value’s relationship with macroeconomic factors was not supported by the long-term data.

Going through 50 years of values’ performance relationship to real bond yields in the US market, there has not been a strong, persistent correlation. It has only been a phenomenon over the past five years.

“Over the past 50 years there has been positive correlation and negative correlation at different times, it's swung around all over the place,” Nunn said.

This correlation may feel stronger than it is because value and bond yields moving together has been a “powerful narrative” recently and has seen some near-term positive correlation.

“So I think that it's understandable that people focus in on it today,” Nunn said.

Another misconception is that value just constitutes cyclical stocks and that value funds are therefore “stuffed full” of sectors and companies entirely dependent on strong economic growth.

This isn’t the case, according to Nunn, because what is cheap changes over time, this just happens to be the case at the moment.

Khalaf, added that value stocks such as tobacco are not “purely cyclical bets” just as Nunn described. These, Khalaf said, could fare better than the wider, value category during stagflation, in the absence of environmental, social and governance (ESG) headwinds.

Long-term Nunn said the performance of value was not intrinsically linked to economic growth or inflation, adding that he was not worried about the impact of stagflation.