More than £1bn has been withdrawn from the Trojan Income fund in the past year but remaining investors should treat it as a buying opportunity in the fund, market commentators have said.

There are two main reasons behind investors leaving the fund. First, performance has slipped in the past year as it has not been a favourable market environment for the Trojan Income process.

FE fundinfo Alpha Manager Francis Brooke, Hugo Ure and Blake Hutchins, run the fund in a more cautious mindset, focused on protecting capital rather than shooting the lights out with returns or sacrificing capital to chase a higher yield.

Brooke, who launched the fund in 2004, therefore buys companies with reliable and growing income from the ‘growth’ part of the market.

Square Mile Research called this a “sound investment process” and should protect investors in downturns, but added that the fund’s “low risk” characteristics meant it could lag during more “aggressive upswings”.

This was the case during the past 12 months where the combination of a more conservative approach and underexposure to cyclicals – which have led markets since November – meant the fund has underperformed significantly. Over one year it is the worst performing fund in the IA UK Equity Income sector.

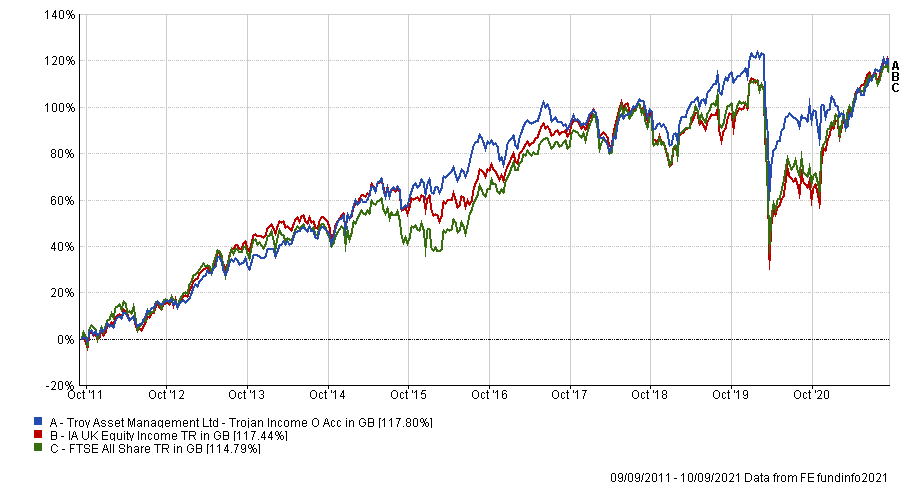

Performance of fund vs sector and index over 1yr

Source: FE Analytics

Despite heavy outflows during the past year and the weaker performance, Trojan Income remains one of the biggest funds in the IA UK Equity Income sector, at £2.7bn.

Ryan Hughes, head of active portfolios at AJ Bell, said that this underperformance was expected.

“It was no surprise to see the fund lagging significantly, in fact, I would have been worried if it had done anything else given its style bias,” Hughes said.

“As a result, short-term performance seems to have shaken some investors out of the fund resulting in reasonably large outflows.”

The second reason was the announcement that founding manager, Brooke, would be steeping down at the end of this year, transferring lead management of the fund to Hutchins.

Hughes said that while this transition has been well-communicated ahead of time “it may have caused some investors to look elsewhere.”

Sometimes a change in management can create some concern for investors who may associate the manager with the style and therefore performance of the fund, even if there is continuity in the process.

Adrian Lowcock, independent fund commentator, said that Hutchins’ management takeover has been “well planned” and noted that Brooke’s skills won’t be completely absent post 2021, as he’ll take on a more background role. This should be reassuring for investors.

Lowcock added that Trojan group generally have a “strong culture and clear process” which isn’t likely to change in any significant way with a change in manager. Neither of the two factors raised were a concern, he noted.

Overall, Lowcock recommended that remaining investors in the fund should stay put, while Hughes labeld the fund a 'Buy'.

The fund in currently soft closed new institutional and pension investors but it is still available to new retail investors with no minimum investment amounts or charges. A 5% charge does apply to new institutional and pension investors, “with the intention of preventing burdensome marketing requirements on the managers time,” Square Mile said.

Hughes said that the fund was an “excellent option” for investors wanting exposure to high quality UK companies. He added that it remains a “core part” of AJ Bell’s own portfolios because it is still performing as expected, but said “it’s important to recognise that it will have periods of underperformance given it focuses on quality.”

Looking at the fund’s long-term performance, it has beaten its sector and benchmark over the past decade.

Performance of fund vs sector and index over 10yrs

Source: FE Analytics

Tom Sparke, GDIM investment manager, was also bullish on Trojan Income, particularly because the fund has below average volatility versus its peers, “which is important in uncertain times.”

Indeed the fund’s 10-year cumulative volatility is the best in the sector, a product of the team’s more cautious, approach.

This was “impressive” according to Sparke, given that the fund has a concentrated portfolio of 45 names, meaning a dip in just a handful of companies would be more closely felt.

Another ‘Buy’ argument for Sparke was that Trojan Income was that the UK market is also an attractive place to invest at the moment.

He said that the domestic market offered good value relative to other regions and from an income perspective was already returning decent yields after last year’s dividend crisis.

Trojan Income holds an FE fundinfo Crown Rating of four and has an ongoing charges figure (OCF) of 1.01%.