Recent price rallies in numerous commodities are unsustainable, according to Amati’s Georges Lequime, but this doesn’t mean investors can’t make money from the sector.

Post-Covid bottlenecks in the supply of natural resources have been exacerbated by the war in Ukraine, due to Russia’s status as one of the world’s biggest producers of commodities. This has caused panic among traders, contributing to large price swings.

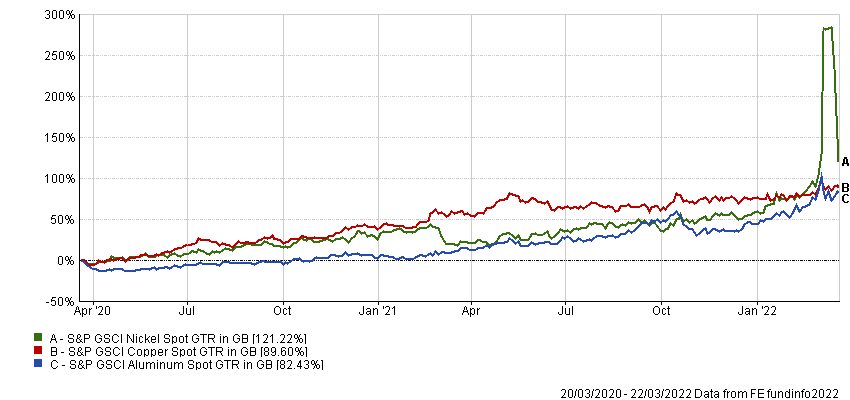

The nickel price has now begun to correct after doubling in a single day on 8 March, following a well-publicised short squeeze. However, Lequime, manager of the TB Amati Strategic Metals fund, said the rally in lithium was also unsustainable – its price is up more than 500% over the past year.

He also warned that copper and aluminium looked “very hot”, with prices likely to fall towards the long-term average in the next six months.

Performance of indices over 2yrs

Source: FE Analytics

Yet he said this didn’t make the sector a no-go area, as the fortunes of mining stocks often lag behind the commodities they extract, pointing to gold as an example.

“Through the 1980s and 1990s, we often used to see gold mining companies trade at 1.5 to 2x net asset value [NAV], and EBITDA [earnings before interest, tax, depreciation and amortisation] multiples between 15 and 25x,” he explained.

“But the M&A deals that the gold industry went through in 2011 to 2012 caused those ratings to disappear.

“The market said, ‘you’ve destroyed a lot of capital’ and now this sector is trading at an average of 5.5x EBITDA.”

Performance of ETF vs index since 2011

Source: FE Analytics

Lequime said the fall in the gold price between 2011 and 2015 acted as a reality check for miners, forcing them to become more disciplined and focused on the bottom line, rather than expanding at all costs. Yet these more efficient business models were not being reflected in valuations.

“I can only ascribe it to the fact that the sector is so under-owned, and when the rest of your portfolio is doing very well, there’s no need to invest in it,” the manager continued.

“Some of these gold mining companies are on 20% free cashflow yields. Investors will come back at some point, yet we still have that big disconnect.”

Gold has risen by about 40% over the past three years, but it is lagging well behind many of the metals mentioned above. Yet while Lequime and his co-manager Mark Smith are wary of many miners of these “hot metals”, they do not avoid them altogether.

For example, they hold two lithium miners – Sigma Lithium, which operates in Brazil, and Atlantic Lithium, which operates in Ghana and the Ivory Coast.

Smith said he was attracted to these companies by the high lithium grades in their mines, with low grade variability and contaminant levels in the ore body.

“When you tick all these boxes and you've got large projects with more than 20 years of life, they can modularise their mining business,” he said. “Quality attracts quality in these companies.”

The rise in the price of lithium over the past few years can largely be attributed to its vital role in electric vehicle batteries, and Smith said understanding this supply chain was key to making money from this commodity.

Because Sigma and Atlantic Lithium have high-quality ore deposits and scalable mining operations, they can enter joint ventures with chemical tollers, allowing them to cut out the middlemen and go straight to electric vehicle battery manufacturers with “take or pay contracts”. Their customers include the likes of Mitsui and Tesla.

“It's these middlemen that take all the money and profit in this industry,” Smith continued.

“But [Sigma and Atlantic] can use the credit rating of these battery manufacturers to finance a project. The more inferior companies – and there's a lot of them out there given the lithium price rally that we've seen – can only sell their industrial-grade concentrate to the next man in the battery supply chain. They can't participate in the value uplift from selling battery-grade lithium carbonate direct to the battery makers and the car manufacturers.”

The benefits of these joint ventures are clear – Smith said a miner selling lithium concentrate can expect to receive $2,700 a tonne, whereas the lithium carbonate produced by a chemical toller commands $76,000 a tonne.

“So there's the value uplift,” Smith added. “We do our homework based on the sector as well as the companies we invest in and we don't just blindly invest in a trend, like we've seen from others.”

Data from FE Analytics shows TB Amati Strategic Metals has made 27.6% since launch just over a year ago, compared with gains of 31.5% from its IA Commodity/Natural Resources sector.

Performance of fund vs sector since launch

Source: FE Analytics

The £50m fund has ongoing charges of 1%.