Bank of America is going into 2023 with a less bearish stance than it went into 2022, given the pain that has already been felt in markets, but has its eye on a series of surprises that could change things for better or worse.

“[A] bear market in bonds and stocks means much greater investor pessimism versus a year ago and [it is] very unlikely central banks around the world hike rates another 280 times in '23,” its strategists explained in a 2023 outlook note.

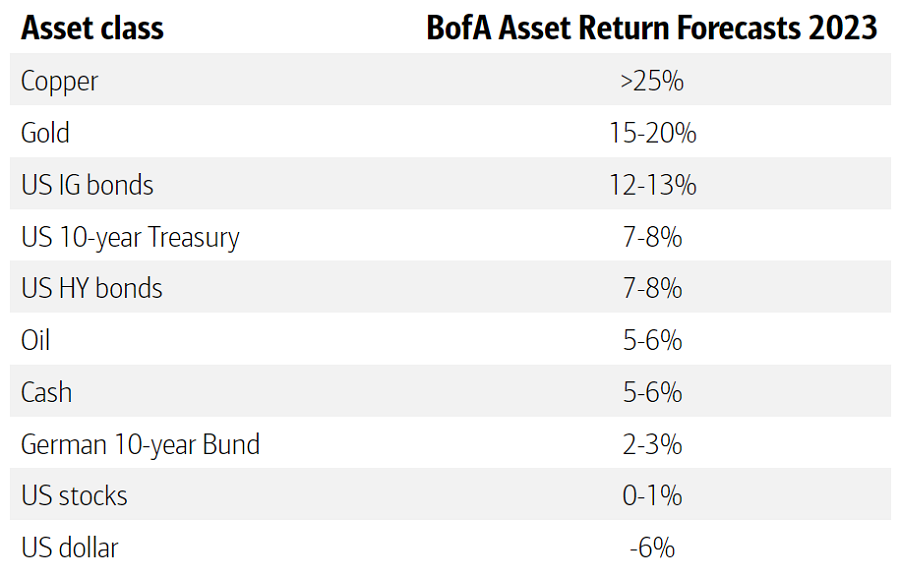

BofA economists and strategists forecast there will be a mild US recession, lower inflation, a stronger China, peaks in interest rates, yields, spreads, US dollar and oil prices and flat US stock prices in 2023, as well as it being a very positive year for gold and base metals.

This means the bank’s expected market returns for the upcoming year are “cautiously positive”, although, as the table below shows, it still expects cash to make a higher return than US stocks.

BofA Research expected returns in 2023

Source: BofA global investment Strategy

But when it comes to how to position during 2023, Bank of America strategists said they are likely to stay bearish on risk assets for the immediate future. The bank will be long bonds in the first half and with equities it will “nibble” when the S&P 500 is at 3,600 (it is currently above 3,900), “bite” at 3,300 and “gorge” at 3,000.

In the second half of the year, Bank of America expects to be long stocks and corporate credit. Part of this is based on the expectation that the Federal Reserve will start to cut rates in 2023 – the bank’s forecast has the Fed funds rate peaking at 5-5.25% in March before the central bank pivots in the summer then cuts by 25 basis points in December.

However, it added that 2023 could throw up some surprises for investors and highlighted six in particular that they should be watching out for.

The first of the three positive surprises is called the ‘botox bull’ by Bank of America and would be kickstarted if the market started to think policymakers are not willing to tackle inflation by enduring a recession.

In this scenario, “investors [would] discount monetary/fiscal policy capitulation at the first sign of recession pain on Main St to coddle new electoral expectations of stimulus checks, rebates, debt forgiveness, [etc] to ease slightest economic pain”.

The second positive surprise would be a ‘1975 redux’. This is based on the Great Pivot in December 1974, when the Fed started to cut rates and ultimately took them from 9.25% to 4.75% – despite inflation being at 12%.

The pivot was driven by deeply negative GDP, a 40% fall in the stock market and a jump in inflation from 5.6% to 6.6%; over the next 12 months, the S&P 500 staged a 31% rally.

Geopolitics could provide the third positive surprise, if the backdrop flips from being negative to positive. This would take the form of a “static” situation between China and Taiwan, a Russia-Ukraine stalemate and improving Saudi-US relationship.

BofA said “all aid a big fall in oil prices down to less than $70 per barrel, allowing European and Asian cyclical assets to significantly outperform”.

However, the bank also highlight three negative surprises to keep on the radar.

The first is a continuation of the ‘detox bear’, or the turmoil that has been seen as central banks attempt to ween markets off of ultra-loose monetary policy.

Bank of America strategists said: “12 years of hubristic monetary excess and abnormal credit/equity returns require more than six months to detoxify; hardcore investor beliefs ("Fed always blinks", "stocks always go up", "tech always leads stocks up") need to end via Fed policy so asset prices can lead inflation lower.”

The second negative surprise is a ‘US dollar super spike’ if markets continue to punish perceived policy mistakes by flocking to the greenback.

This would stop bond yields from falling and cause the long investment-grade credit trade – which is the consensus trade for 2023 as these assets tend to hold up in recessions – to fail. “[Here, the] bear market ends with a classic liquidity panic and rush to US dollar safe haven,” the bank said.

Geopolitics could also be negative. BofA strategists warned that inflation could cause social unrest and negative geopolitical repercussions in countries with strategic importance and/or nuclear power.

They gave the examples of Iran (where consumer prices inflation is north of 50%), Pakistan (>25%), Turkey (>80%) and Egypt (>15%) as countries where this is a potential concern.