Terry Smith, manager of Fundsmith Equity, revealed he has found a bank in which he is considering investing at the fund’s latest annual general meeting.

This is a volte face, as the manager of the £25.4bn global equity open-ended fund has long shunned the banking sector.

Smith used to be a banking analyst but said as recently as last year that he categorially “never invest[s] in banks” because they have “massive leverage” and “inadequate returns”.

“Even if the bank you are invested in is well run it can still be damaged or destroyed by a general panic in the sector,” he wrote in the Financial Times shortly after the collapse of Silicon Valley Bank (SVB) in March 2023.

Smith also highlighted that banks are increasingly facing the threat of being disrupted by fintech companies.

Fundsmith declined to comment on Smith’s change of heart or to reveal which bank he is considering investing in.

Other managers are also taking a renewed interest in the sector.

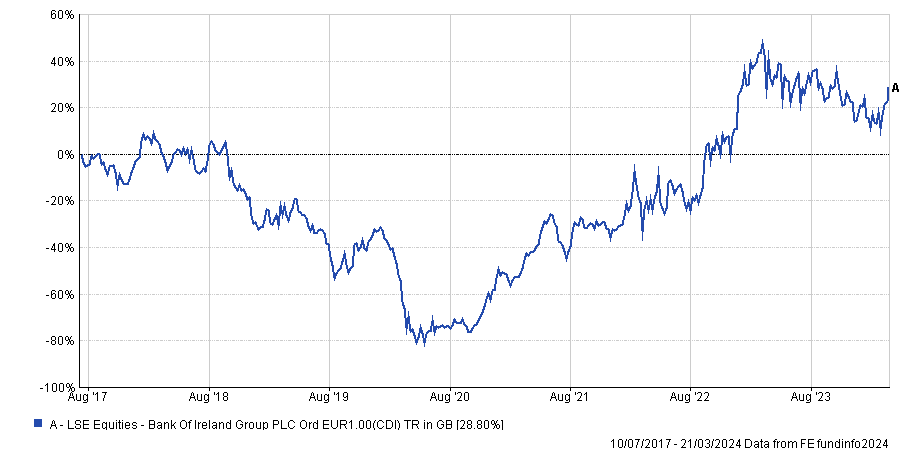

Julian Bishop, co-lead portfolio manager of the Brunner Investment Trust, said many banks are in a much better shape than they were 10 years ago. He took the Irish market as an example as he recently added Bank of Ireland to his portfolio.

“Ireland has been dealing with a very tough crisis in its property sector. Whenever that happens, the banking sector gets into problems because they're financing it and the value of their collaterals collapses,” he said.

“When you get a crisis, the regulator is accused of being asleep at the wheel and has to up its game. It has to force banks to hold more capital, to de-lever, take less risk and improve their credit standards, etc.”

However, Bishop explained that the Irish banking sector has improved markedly since the European sovereign debt crisis.

“There were four main banks in the Irish market, but two of those have basically pulled out. So, the market structure has improved,” he said.

“At the macro level, household debt to GDP in Ireland was 93% 10 years ago versus 2.6% today. In 2013, non-performing loans were at 21%, while they are at 3.6% today. The capital ratio has improved from 9% in 2013 to 15% today.”

Performance of stock since listing

Source: FE Analytics

While Bank of Ireland was a loss-making company 10 years ago, it has been rebuilding its balance sheet and now boasts a return on tangible equity of 15%, according to Bishop.

He added: “Bank of Ireland has only been able to return about 6% of the current market cap over the past 10 years, but we think it can return over 40% of its market cap through dividends or share buybacks over the next three years. It’s an incredible return and a lot lower risk than it was in the past; that's absolutely worth considering.”

The Cashflow Solution team at Liontrust is also positive on banks in Europe, many of which have reported growth in their annual dividends and announced share buyback programmes.

Samantha Gleave, co-manager of Liontrust European Dynamic, holds Italian bank UniCredit. “It's enjoying a recovery in its earnings and there’s been quite a lot of self-help at that bank. It’s been prompted by the arrival of a new CEO a couple of years ago, who has taken out excess costs, rationalised the business and returned cash to shareholders,” she said.

Performance of stock over 5yrs

Source: Google Finance

Other bank holdings include Mediobanca, also from Italy, Banco Santander in Spain and Germany’s Deutsche Bank, which Gleave described as a “deep value play”.

She said: “Deutsche Bank is one of the few contrarian value stocks in the portfolio. It's trading on a very attractive valuation and the new CEO is engaged in a very significant cost restructuring programme.”

Performance of stock over 5yrs

Source: Google Finance

European banks proved their resilience last year during the banking crisis in the US, Gleave continued.

“One of the big differences between Europe and the US is that European regional banks have been heavily regulated since the global financial crisis, whereas regional banks in the US haven’t been. I think that is why the banking crisis that we've seen in the US didn't unfold in Europe,” she explained.