After months of strong performance from European equities and the euro, Neuberger’s multi-asset team has closed its overweight positions in both and rotated into regional fixed income, arguing that the balance of risks and valuations has shifted decisively in favour of bonds.

Maya Bhandari, chief investment officer for multi-asset EMEA at Neuberger Berman, said the firm is “cashing in on the European-focused 'Liberation Day' risk trades” that have delivered “handsome returns” since the second quarter.

The team now holds a neutral stance on both European stocks and the euro and is re-establishing long positions in bunds, UK gilts and European investment-grade credit.

Bhandari framed the shift as a response to changing fundamentals. “When the facts change, we change our minds,” she said, quoting John Maynard Keynes. “Every risk has a price, and while for riskier European assets – such as equities and the euro – both risks and prices have increased, they have moved oppositely and more favourably in fixed income.”

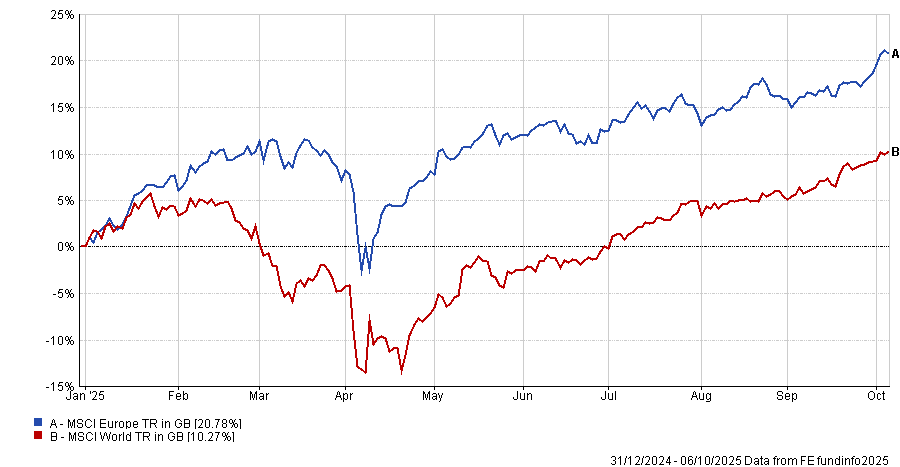

Performance of indices over the YTD

Source: FE Analytics

Neuberger’s initial moves followed the Liberation Day market shock earlier this year, when newly announced tariffs triggered a global sell-off. The firm responded by increasing exposure to non-US markets, adding European and Chinese equities and later Japanese stocks. It also upgraded non-US developed bonds – particularly German bunds – while cutting its US dollar exposure in favour of the euro.

“In the dark days of early April, European stocks suffered significantly and ahead of global equities. Depending on the specific index, they shed 13-14% of their value over the course of the following week in an 11-12 standard deviation move,” Bhandari recalled.

“Turning long European equities was on our radar at the time – an asset we liked just got materially cheaper – and we moved European stocks to overweight, endorsing unhedged exposure by moving the euro to overweight versus the US dollar in tandem.”

Two quarters later, those trades have largely played out. European equities have rallied strongly, supported by a rebound in sentiment and a weaker dollar, while banks – a large share of the regional index – have delivered outsized gains. The euro has climbed from near parity to around 1.18 against the dollar, bolstering unhedged returns.

As such, the picture for Europe has deteriorated markedly since spring.

Back in April, European fundamentals looked supportive with improving earnings prospects, expectations of German fiscal stimulus and a weaker dollar enhancing the outlook for unhedged returns, said Bhandari. By October, earnings growth have collapsed to zero, revisions are sharply negative and fiscal support has failed to materialise, while banks’ strong share price gains mask “disappointing” profit delivery.

“Tariff outcomes have been worse than expected, German fiscal easing has been sluggish and the prospect of further support from other countries has faded after France’s debacle.”

Valuations that once appeared attractive have become stretched after sharp price rises and flat earnings, leaving relative value only modestly appealing.

Investor sentiment has also swung from underexposed to neutral, with flows into European equities reaching their highest level since 2017.

In the firm’s assessment, the valuation and sentiment backdrop that justified an overweight in spring has largely reversed. Absolute valuations have become “punchy” after the rally, while relative valuations – still modestly attractive versus the US – now reflect weaker profitability. “This seems justified,” Bhandari said.

Given these shifts, Neuberger now holds European equities “at target” rather than overweight. The firm remains more positive on Japan, where fundamentals, shareholder reforms and valuations continue to support an overweight stance.

The other side of Neuberger’s asset allocation shift is a renewed focus on European fixed income. The firm sees a widening gap between equity and bond valuations – a “20,000-foot premium gap” that offers more compelling relative value opportunities.

Long-dated eurozone bond yields have recreated a premium last seen in the early days of the Covid pandemic. Neuberger expects this divergence to narrow as economic growth and inflation soften.

The firm expects the European Central Bank to deliver further rate cuts rather than stay on hold, with a similar dynamic supporting UK gilts. “Less fiscal easing should also dampen upward pressure on term premia,” Bhandari said, suggesting scope for bond prices to recover as monetary policy eases.