Close to 90% of funds in the Investment Association universe made a loss on Monday and Tuesday this week when investors went into risk-off mode following the start of a fresh conflict in Iran.

Markets were rattled over the two trading sessions by the news that the US and Israel had launched a massive strike on Iran in the so-called Operation Epic Fury. Iran retaliated by hitting US military bases and neighbours in the Gulf with missile and drone attacks.

Wednesday’s session was better, with markets cautiously rising as investors caught their breath. Russ Mould, investment director at AJ Bell, said: “Tuesday was dominated by investors selling assets that had already served them well, such as defence stocks and gold, as they locked in profits.

“More stability on the markets is welcome not only for sentiment but also as it might give certain investors the confidence to go hunting for bargains and drive a new wave of buying.”

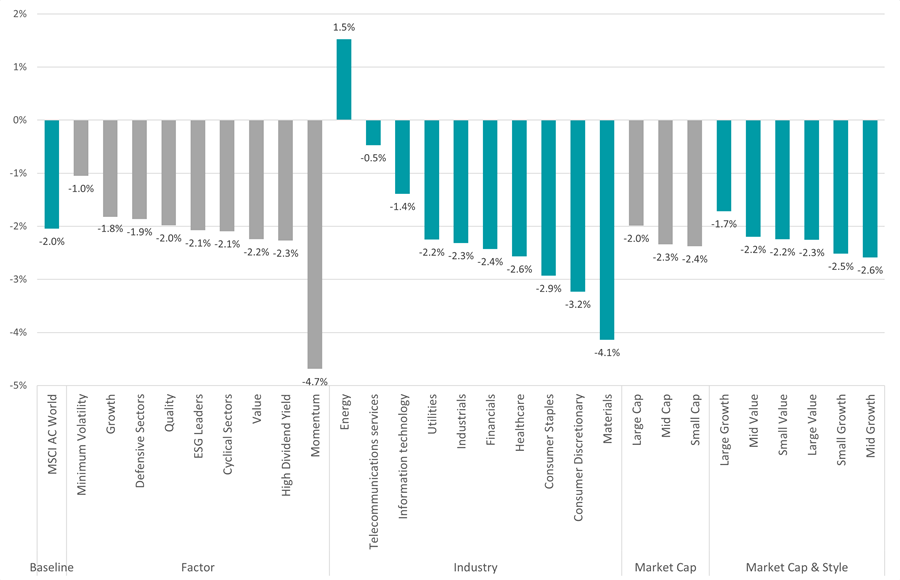

When markets were selling off on Monday and Tuesday, stocks were the hardest-hit asset class, as would be expected in a risk-off environment, with the MSCI AC World index falling 2% in local currency terms.

As the chart below shows, all investment factors have made losses this week with momentum stocks – or those that have been performing strongly over the recent past – hardest hit.

Performance of MSCI AC World and sub-indices on 2 and 3 Mar 2026

Source: Finxl. Total return in local currency on Mon 2 Mar and Tue 3 Mar 2026.

All equity sectors aside from energy fell also, as investors fled to safe havens. Energy stocks, meanwhile, have benefited from the surging oil price.

On a geographic basis, European equities sold off the most with the Euro STOXX shedding 5.5% as investors fretted about the prospect of a prolonged war in the Middle East and higher oil prices fuelling another surge in inflation.

Emerging markets – which have been outperforming recently – also suffered. The MSCI Emerging Markets index fell 4% over the two trading days, while MSCI Frontier Markets was down 4.6%.

The US, on the other hand, held up the best with the Nasdaq 100 flat and the S&P 500 and the Dow Jones both slipping 0.9%.

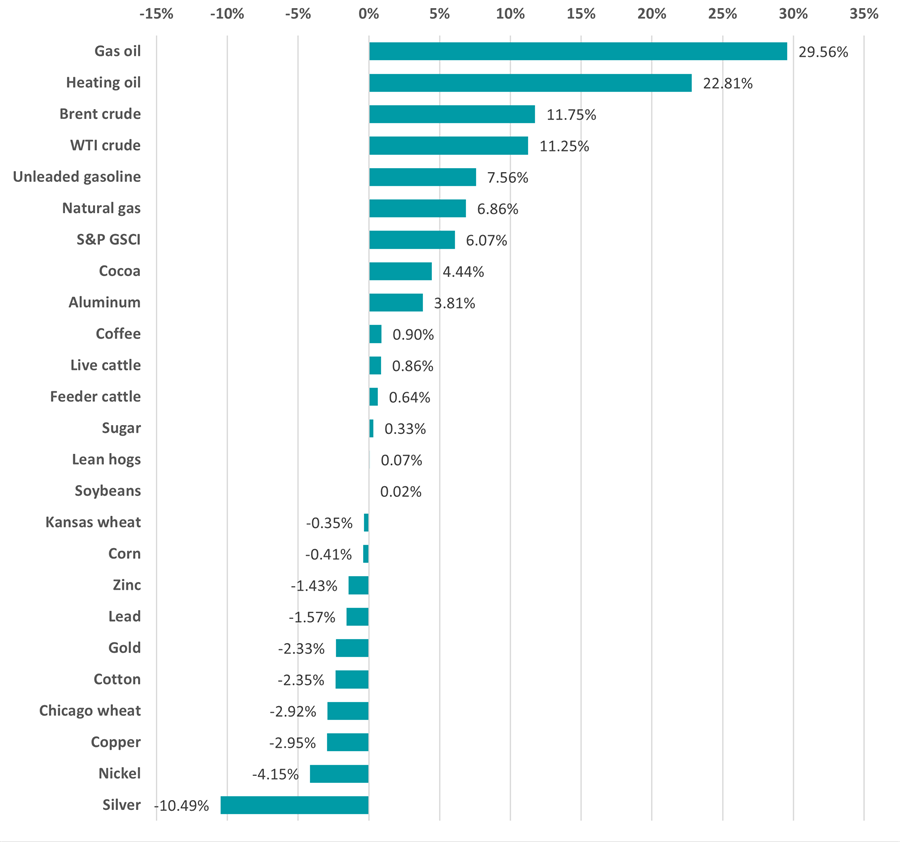

Performance of commodities on 2 and 3 Mar 2026

Source: Finxl. Total return in local currency on Mon 2 Mar and Tue 3 Mar 2026.

Global government bonds fell 1.5% and corporate bonds were down 1.1% but commodities (represented by the S&P GSCI) jumped 6.1% in local currency terms, driven largely by the spike in energy prices caused by Iran’s threats to close the Strait of Hormuz.

Maurizio Carulli, global energy analyst at Quilter Cheviot, noted that recent oil supply and demand fundamentals had pointed at a surplus in 2026, which could be undone by the conflict. The oil price started 2026 at $60 a barrel, had risen to $72 by last Friday and jumped to $80 after the conflict started.

“Depending on how, and for how long, the current military action will continue, the oil price will adjust quite quickly,” he added. “So, if the situation will calm down over the next few weeks, as is well possible, the price is likely to revert to $60-$65/bbl, given oil production is in excess of demand and Opec+ has some spare capacity to increase production further.

“And, vice versa, if the situation precipitates into a widespread and prolonged Middle East war, with shipping across the Strait of Hormuz halted, then the oil price could feasibly rise to $100/bbl and above.”

Gold initially rallied as investors flocked to safe havens when the conflict broke out but has dipped more recently on concerns that higher oil prices will reignite inflation.

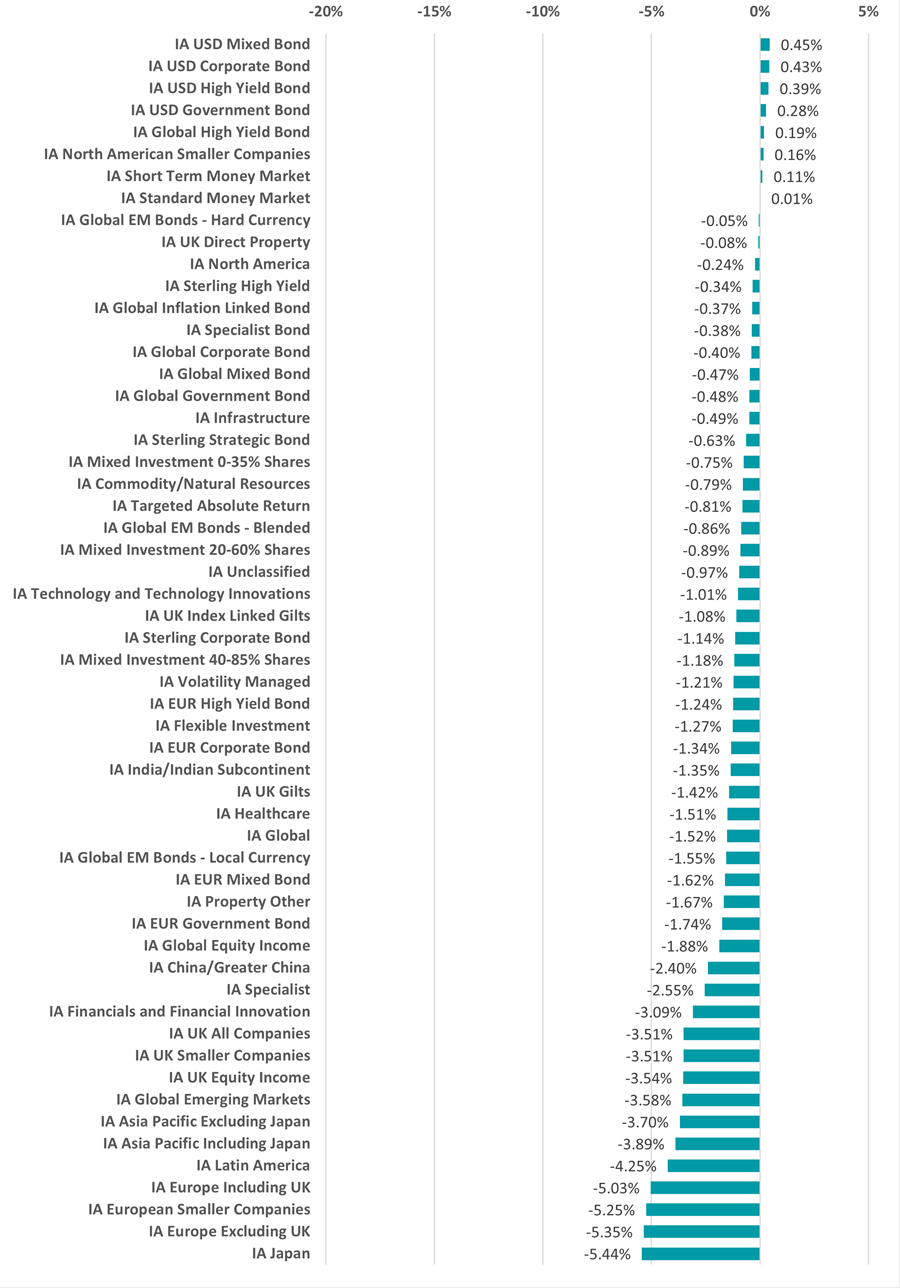

Among the Investment Association’s fund sectors, peer groups focused US bonds fared the best as the US dollar regained some of the safe-haven status it seemed to have lost in 2025. Money market funds also witnessed small gains.

Performance of IA fund sectors on 2 and 3 Mar 2026

Source: Finxl. Average return in sterling on Mon 2 Mar and Tue 3 Mar 2026.

IA North American Smaller Companies was the only non-fixed income or money market peer group to make a positive return over the two days of the sell-off.

The worst returns came from the IA Japan sector, where the average fund lost 5.4%. In keeping with Mould’s point about investors selling assets that had “already served them well”, Japanese equities had previously rallied on the back of prime minister Sanae Takaichi's landslide election victory.

All three European equity peer groups were also hit with some of the Investment Association’s biggest loses this week.

Source: Finxl. Total return in sterling on Mon 2 Mar and Tue 3 Mar 2026.

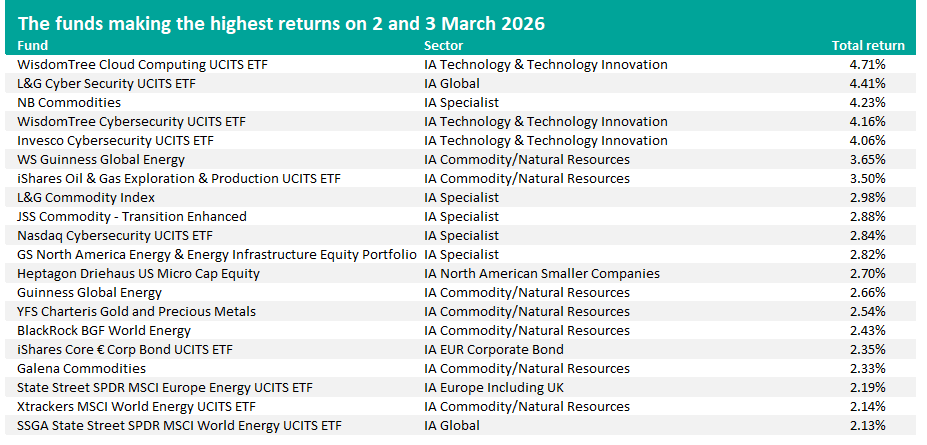

Just 11.6% of the close to 5,500 funds in the Investment Association universe made a positive return during the two trading sessions in question.

The best performers, as can be seen in the table above, revolve around a narrow group of themes.

Technology is one, with WisdomTree Cloud Computing UCITS ETF posting a 4.7% total return. Cybersecurity is the main area of interest, however, owing to its role in hybrid warfare; L&G Cyber Security UCITS ETF, WisdomTree Cybersecurity UCITS ETF and Invesco Cybersecurity UCITS ETF are up more than 4%.

Energy is the other major theme, somewhat predictably thanks to the rising oil price. WS Guinness Global Energy, iShares Oil & Gas Exploration & Production UCITS ETF and BlackRock BGF World Energy are some of the dedicated energy funds making the highest returns.

Source: Finxl. Total return in sterling on Mon 2 Mar and Tue 3 Mar 2026.

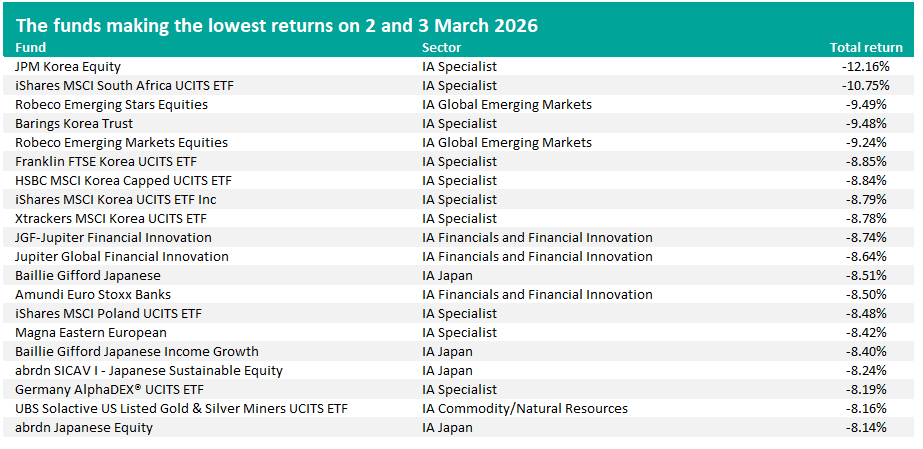

Among the worst performers are Korean equity funds such as JPM Korea Equity, Barings Korea Trust and Franklin FTSE Korea UCITS ETF.

Korea was one of 2025’s best markets, owing to improving corporate governance and the AI trade, but was hit this week when investors tried to lock in profits.