One of the main cognitive biases investors have to grapple with is extrapolation, or believing that the current conditions also the norm (when, in reality, there is no ‘norm’, only an ever-evolving landscape).

Trevor Greetham, head of multi-asset at Royal London, has seen investors extrapolate throughout his career – in the pensions mortgage boom of the late 1980s, in the dot-com bubble of the late 1990s and in the more than decade-long bull run post financial crisis that has shaped the expectations of an entire generation of new investors.

The pattern is always the same: a long period of strong returns produces “a real sense of ‘just give me the big numbers’," he said. This affects more seasoned investors too.

As Trustnet explored recently, fund managers and DIY investors alike have been leaning a lot into risk in early 2026, despite multiple alarm bells ringing. This is particularly true for younger cohorts, with six in 10 Gen Z self-directed investors saying they are taking more risk than usual, according to research from Charles Stanley Direct.

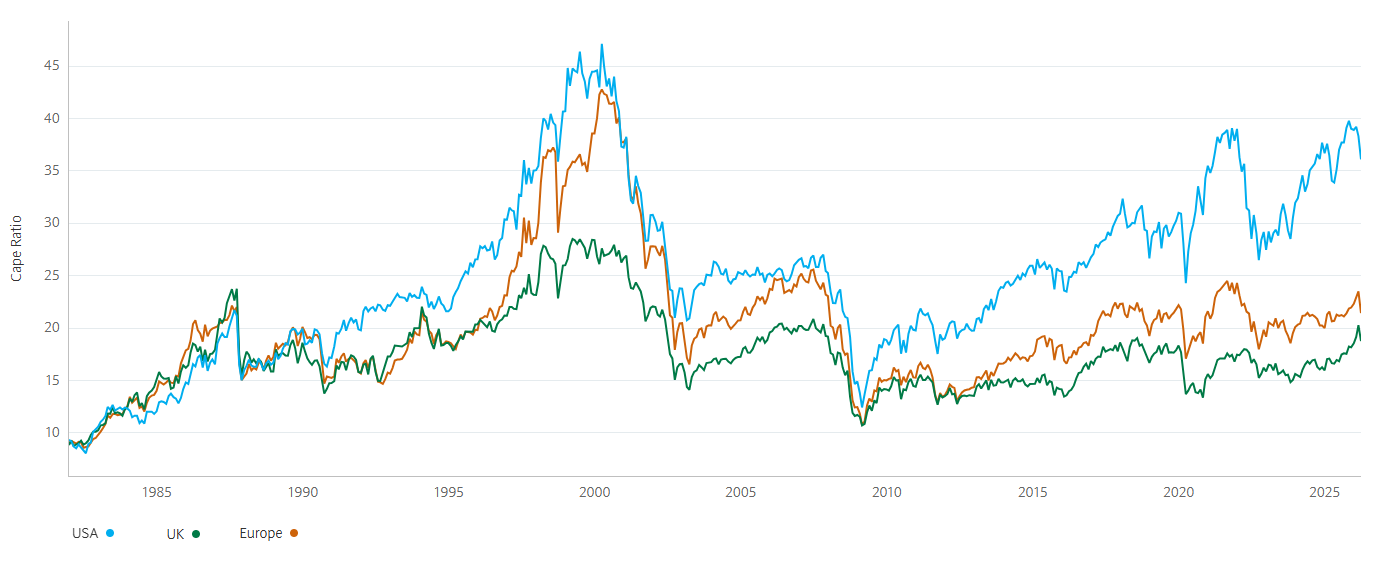

The maths, up to a point, supports them. US equities are currently trading at a cyclically adjusted price-to-earnings ratio of around 36x, according to Barclays data – elevated by any historical standard, but a level that has been sustained and exceeded in recent years.

The same data shows the US CAPE briefly touched 47x at the peak of the dot-com bubble in early 2000, before collapsing to below 25x within three years. The UK, by contrast, sits at around 19x – less than half the US reading.

Historic CAPE ratio by country

Source: Barclays Research

Against that backdrop, a young investor with a 40-year horizon has something that older investors do not: time to absorb whatever comes next. Most of a young investor's future wealth is in money they have not yet put to work.

"It doesn't matter that much if you lose the first year's premium, even if you lose all of it, because there are another 39 years you're going to be putting money in," he said.

"On the other hand, the older you are, the more you have a big pension pot and suddenly you're much more risk averse because you don't want to lose it," Greetham said.

Most pension propositions are structured on exactly this basis, with the youngest investors holding almost entirely equities and gradually diversifying as retirement approaches.

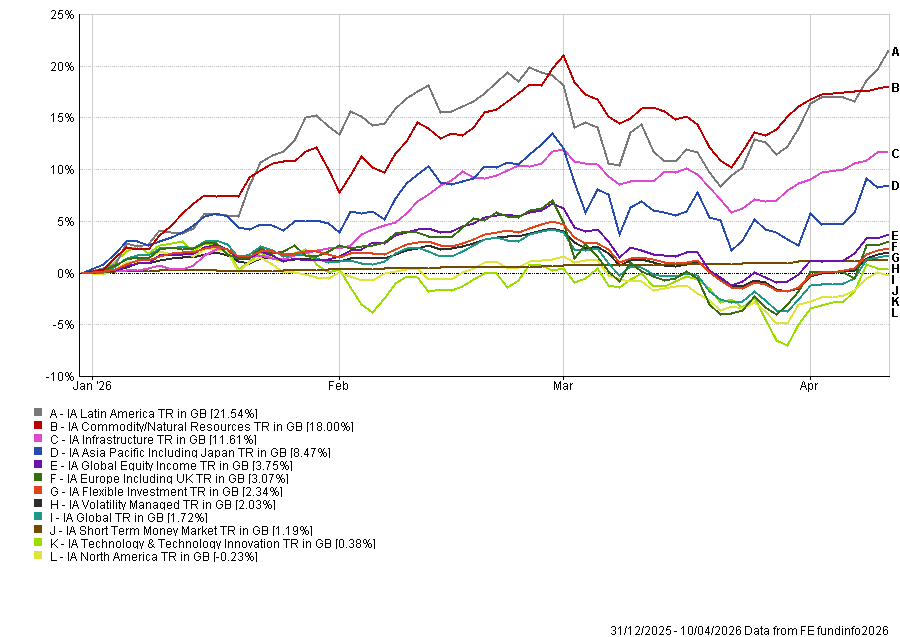

The complication is what the past decade has done to expectations. An investor who started a global tracker at the beginning of 2026 would have made around 1.7% year to date by early April – but only after a volatile ride.

North American funds are down around 0.2% over the same period, yet US stocks have delivered 14% a year for a decade, making them extremely popular.

The sectors that have actually delivered returns in 2026 – Latin America up more than 21%, commodities up 18%, infrastructure up nearly 12% – are not typically where most young investors are looking.

Performance of sectors YTD

Source: FE Analytics

“People have been in this bull market and they're thinking: great, give me more of the 14," Greetham said. "But it's more likely that you'll halve your money than double it over a five- to 10-year horizon, given the valuation point we're starting from."

The study of historic valuation measure and subsequent returns underpins this view.

Greetham has seen this greed before. Early in his career, before the 1987 crash, the product of the moment was the pensions mortgage – the idea that stock market returns would be so strong that the tax-free cash sum from a pension would pay off a home loan. Actuarial departments were routinely asked to run illustrations assuming equities returned 15%, 20%, even 25% a year for 50 years, he said.

"You can imagine: you put £3 in and you paid your mortgage off." The bull market of the time made the numbers feel inevitable. They were not.

Younger investors today have fewer of the battle scars that temper this kind of extrapolation, Greetham continued. As this column noted last autumn, the appetite among young people to get rich quickly is not new. What has changed is how easy it is to act on it – and the tools now available to do so.

"There is a reason why it's logical for the young investor to take more risk," the manager said. "But there's also a bit of human nature that degenerates when you start talking about the kind of risk they're taking. It's often outside investing and more like trading, crypto and gambling."

The answer, in Greetham’s view, is not to abandon risk but to attach a plan to it. "Higher risk for younger investors is sensible," he said, "as long as there's a plan as they get older to diversify into more store-of-value asset classes."