Recent market volatility, stubborn inflation and signs of cooling labour market conditions have raised concerns that economic momentum is slowing.

In this environment, high-quality companies with resilient cashflows and strong balance sheets should be better placed to withstand tougher conditions.

Trustnet asked fund managers which companies they believe are best placed to hold up if growth weakens.

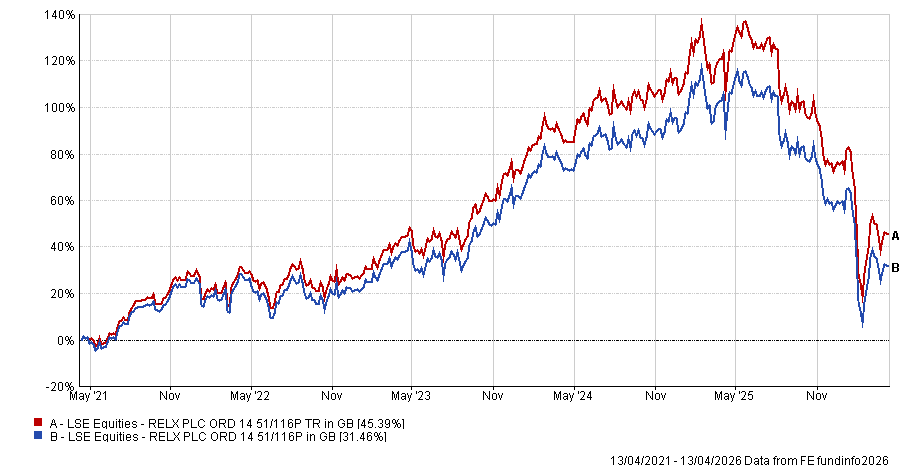

RELX

Alan Dobbie, co-manager of Rathbone Income, highlighted British analytics business RELX, a company which spans scientific and medical publishing, legal content, and risk and analytics.

“For more than a decade, RELX has built a reputation as one of the UK market’s most reliable defensive growth stocks,” he said.

He noted that customers are usually tied in through multi‑year contracts and recurring subscription revenues and, once RELX’s datasets are embedded into the workflows of legal or financial institutions, switching costs are high.

“That resilience has translated into steady high‑single‑digit revenue growth, supported by high and gradually improving operating margins,” he said.

“Strong cash generation, disciplined reinvestment and regular share buybacks have helped deliver dependable, repeatable earnings and dividend per share growth, reinforcing RELX’s appeal as a defensive compounder.”

Sentiment toward RELX weakened earlier this year on fears that AI could commoditise information or pressure pricing power, prompting a sell-off in early February. Dobbie said these concerns are “overdone”.

“[RELX’s value] lies in carefully curated, verified and legally defensible information, combined with workflow integration and regulatory credibility,” he said, adding that AI is more likely to enhance its products than undermine them.

Stock total return and share price performance over 5yrs

Source: FE Analytics

Linde

Industrial gases company Linde manufacturers atmospheric and process gases that are required in a wide variety of industries, including energy, healthcare and steel. It also provides engineering solutions and decarbonisation technologies.

Mark Peden, co-manager of Aegon Global Equity Income, said: “Given the oligopolistic nature of the gases industry – with effectively only three players now controlling the market – and a reliance on long-term, inflation-linked take or pay contracts that numb the sensitivity to downturns in industrial production and provide unrivalled cashflow visibility, the stock is a fantastic defensive compounder.”

He noted that the company has beaten earnings-per-share (EPS) estimates in every quarter since 2018 and has grown the dividend every year for 33 years.

“Although the company is strongly shielded from economic downturns, it also provides nice upside capture in the good times, too, as gas volumes grow when industrial activity picks up,” Peden added.

He pointed to consistent revenue growth, gradual margin expansion, an active share buyback programme and a growing dividend, adding that the stock offers an attractive lower-beta total return across cycles.

Arthur J. Gallagher

Matthew Page, co-manager of Guinness Global Equity Income, pointed to portfolio holding Arthur J. Gallagher as a high-quality, defensive compounder with a durable competitive position in the mid-market.

The insurance broker earns commissions and fees for placing coverage and has maintained “a highly recurring, non-discretionary revenue base with client retention rates above 90%”.

Page said the firm has impressive operating performance, with strong free cashflow generation, expanding margins and a steadily compounding dividend.

“The firm also targets double-digit revenue growth through mid-single-digit organic expansion and disciplined tuck-in merger and acquisition (M&A) of small regional agents and brokers,” he said.

While this introduces some integration and competition risks, Page said Arthur J Gallagher’s long track record of disciplined execution gives confidence in the long-term strategy.

LVMH

Nikki Martin, senior portfolio manager in global equities at Sarasin & Partners, suggested luxury conglomerate LVMH as a high-quality, cash-generative company that can preserve capital through weaker cycles.

She noted that LVMH is “supported by exceptional brand power and pricing ability, enabling it to sustainable margins even as volumes soften”.

“Its diversified portfolio and strong cashflow provide flexibility to invest through downturns,” Martin added.

She noted that the cyclicality of luxury demand is a risk to performance.

Indeed, LVMH’s latest quarterly sales numbers missed expectations, falling by 6% in the first months of the year. The company noted that the Middle East conflict has a 1% negative impact on organic growth in the first quarter of 2026.

Martin said this is ultimately manageable due to the company’s strong balance sheet, cash generation, global scale and entrenched market position.

Tesco

UK supermarket chain Tesco has significant scale, with market share of around 29% , which makes it all the more attractive in a softer economy, according to Callum Abbot, co-manager of JPMorgan Claverhouse Investment Trust.

“Food retail is one of the most resilient sectors in the market, as it sells everyday essentials that people simply can’t go without,” he said.

“If inflation remains elevated, retailers such as Tesco are also typically able to pass on at least some of those higher costs, supporting revenue growth.”

Abbot said the company is in a strong financial position, with an investment-grade balance sheet and reliable cash generation, which has allowed it to return cash to shareholders through a growing dividend as well as share buybacks.

In addition, the chain’s ‘Clubcard’ loyalty scheme allows it to offer target discounts and promotions that smaller competitors struggle to match – although Abbot noted a renewed price war within the sector is a potential risk.

“Tesco has gained market share for 32 consecutive four-week periods in a row,” he said.

“That momentum, alongside its strong competitive position, suggests it is well placed to continue outperforming many of its peers in a tougher environment.”

Stock price performance over 5yrs

Source: Google Finance

Royal Bank of Canada

Turning to financials, Greg Eckel, portfolio manager at Canadian General Investments, said Royal Bank of Canada is an “all-weather franchise”.

“It has paid a dividend every year since 1870 and has not cut it in the modern era, demonstrating the strength of its earnings through multiple cycles,” he said, adding that this consistency is “underpinned by a diversified business model”, with franchises beyond Canada in the US and UK.

This includes a personal banking division which delivered a 26.3% return on equity in the first quarter of this year, while its wealth management division oversees C$1.5trn in assets and C$5.3trn in assets under administration.

“This diversification helps smooth returns across different environments,” Eckel said.

“Market volatility, for example, can weigh on lending activity but often supports trading and capital markets revenues, reinforcing overall resilience.”

He said the bank has continued to deliver “robust profitability” through multiple cycles.

Brixmor Property Group

Vince Fioramonti, manager of Allspring Global Equity Enhanced Income, pointed to Brixmor Property Group, which owns and operates a large portfolio of over 350 open-air shopping centres.

Fioramonti highlighted the company’s stable and predictable cashflows, high occupancy above 95%, strong portfolio quality and low earnings volatility.

He added that the tenant base further reinforces this defensiveness, as Brixmor works with over 5,000 retailers, including Kroger and Publix.

The company generates attractive income, with a dividend yield of around 4% and 6% average dividend growth.

Fioramonti said Brixmor’s portfolio has shown greater stability than more economically sensitive sectors, supported by essential tenant demand and disciplined asset management.

“Robust leasing activity and low bad‑debt expectations – projected at just 75 to 100 basis points of total revenue – reinforce confidence in cashflow durability,” he said.

In February, company management projected that funds from operations (FFO) will increase by more than 4% versus 2025, “suggesting continued growth even as the macroeconomic backdrop becomes more challenging”.

Stock price performance over 5yrs

Source: Google Finance