GQG Partners Global Equity fell 9.5% in 2025, the worst result in the 555-strong IA Global and an exceptionally poor return against a sector average gain of 11.2% and a benchmark return of 13.9%.

The culprit, by deputy manager Sid Jain’s own admission, was maintaining too defensive a positioning, which kept the fund from benefiting when markets recovered.

“We exited the AI trade too soon in early 2025,” he said. “We were also too defensively positioned due to concerns around tariffs early in the year. That positioning worked initially but we did not pivot back to risk-on when conditions changed.”

However, GQG had called it right once before. In spring 2021, the firm sold out of technology entirely and rotated into energy – a move that looked painful for a few months before the 2022 tech bear market vindicated it. The fund returned 4.4% that year, when the IA Global sector fell 11.06%.

GQG's technology exposure remains near zero and his case rests on three things: the scale of capex being deployed, the return of leverage and retail mania.

“Allbirds was very popular shoe company a few years ago. It almost went bankrupt, but instead of selling shoes, it announced it is going to build data centres. A shoe company has become a data centre company. And the stock went up 600%. The meme stock phenomenon is fully back, similar to what you saw in 2021. This never ends well," he said.

Below, Jain explains why GQG is sitting out the AI boom again, where it is finding opportunity instead, and what’s it like working alongside his father, FE fundinfo Alpha Manager Rajiv Jain.

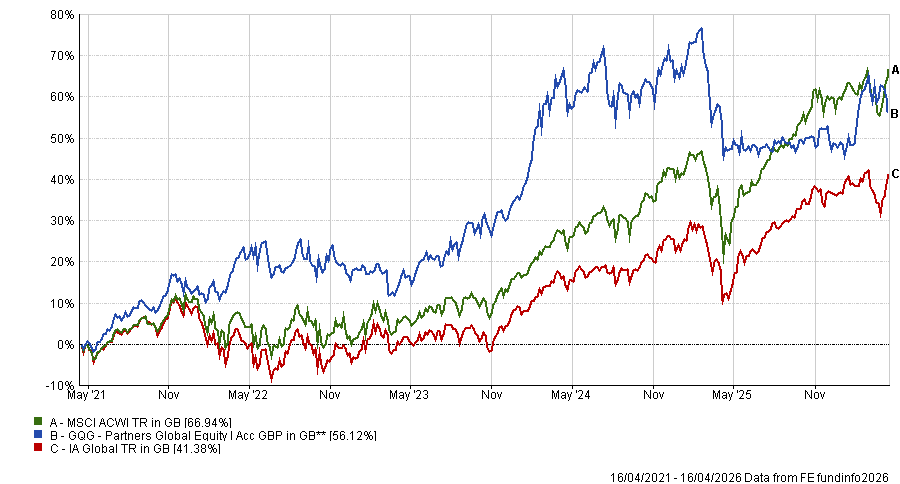

Performance of fund against sector and benchmark over 5yrs

Source: FE Analytics

What is the process behind GQG Partners Global Equity?

We are a concentrated, long-only fund, that is benchmark agnostic and, unlike a lot of our peers, we move around our book quite aggressively.

We like quality companies but most managers look at quality in a rear-view mirror – has this been a good company in the past? We phrase this as forward-looking quality.

The second differentiator is a truly flexible mandate. We’ve been anywhere from 65% tech all the way down to zero, energy up to 30%, emerging markets up to 30%.

The third is downside protection. In 2022, where most of our peers struggled, we were down low single digits because our focus is cutting losses aggressively when things change.

You’re now at around 1% in tech. What has shaped that view?

Hyperscalers today are spending more capex per dollar of EBITDA than the energy sector at the peak of the 2014 bubble and the telecom bubble in the late 1990s. It’s blown through historical levels. You’re also seeing leverage come in, the growth in private credit, trillions of dollars floating around.

We’re not permanent bears on technology. For most of our history we’ve been very overweight. In early 2023 we were one of the biggest institutional buyers of Nvidia stock – it’s the largest winner in our firm’s history. But these companies cycle and we believe you’re late in the cycle.

Where are you finding opportunity instead?

Utilities is one area. The structural story is that growth is accelerating because there has been underinvestment for decades. Regulators in the US, Europe, Brazil and India are becoming more favourable, allowing more capex and higher returns on equity.

A large position for us is American Electric Power – the largest wires company in the US, fully regulated transmission and distribution. Historically it grew about 6% a year. Now earnings per share are growing 9% and you get a 3% dividend yield, so 12% total return. Tariff or no tariff, recession or war, it doesn’t matter.

India is another significant overweight. Our internal mantra is that earnings are like gravity. We like India because it is delivering some of the best corporate earnings growth outside the US. We’re very bullish on Indian banks – earnings growth should be mid-teens, three to four times faster than US banks, but they are trading at around 13 times earnings.

What was your best call over the past 12 months?

Energy. We’ve been structurally bullish for five years and it has paid off, especially over the past 12 months. Exxon is up about 45% including dividends over the past 12 months.

And the worst?

Progressive, the US auto insurance company, is down about 27% year over year. The stock has done poorly, but earnings have been fine – the multiple has contracted, which is less concerning than if earnings were deteriorating.

We still like it. It’s one of the best-run financial businesses in the world. It’s a risk-off asset and in a strong market people don’t want to buy insurance companies. We saw the same in the late stages of the dot-com bubble, after which these stocks rebounded strongly. Progressive is trading at its biggest discount in history to the S&P 500.

When does the fund out- and underperform?

We perform best in the middle of the cycle and in bear markets. We underperform early in recoveries and late in cycles when valuations are ignored and markets become driven by momentum and speculation.

Why should investors pick this fund?

First, the 30-year track record. Many managers today started after the financial crisis and haven’t experienced multiple cycles. The ability to navigate cycles and outperform over rolling five-year periods is rare.

Second, downside protection. Markets are at high valuations with a lot of froth. Our strategies are currently uncorrelated to the broader market – recently, the beta of our global strategy has been close to zero, which is unusual for a long-only manager.

Third, the ability to adapt. The 2022 performance is a case study of exiting tech and pivoting to other areas. That ability to navigate cycles is a key differentiator.

What’s it like working alongside your father?

He’s very competitive and has high expectations for everyone, especially family. That was clear before I joined, so I knew what I was signing up for.

What do you do outside of fund management?

I enjoy hiking, especially now that the weather is improving in New York. I go hiking with my girlfriend and I enjoy outdoor sports like tennis and swimming. I grew up in Florida, so I’ve always liked the outdoors.