Since the market bottom of March 2020, Japanese equities have been on a tear. But behind these strong returns there has been a monumental shift in the types of companies that are in vogue with investors. For valuation-oriented investors, this creates a fertile hunting ground for mispriced opportunities.

Even before the pandemic, certain areas of the market looked extreme in our view. Many high-growth and stable stocks looked meaningfully overvalued, with rich valuations baking in an overly optimistic view of the future.

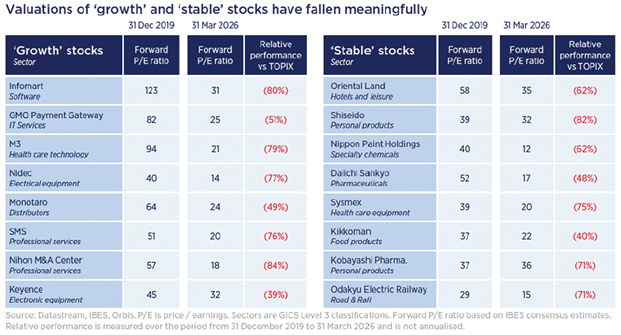

In our December 2019 quarterly report, we highlighted eight of Japan’s fastest-growing companies, as well as eight stocks in traditionally defensive industries that we felt were priced for perfection.

In particular, we highlighted GMO Payment Gateway – a payment service provider with an excellent management team, strong track record and large growth runway – that had become a growth investor darling.

Emblematic of the market’s exuberance, GMO Payment Gateway traded at over 80 times earnings – a rich multiple, even for a company with a track record of having grown earnings by over 25% per annum over the prior 10 years.

While we acknowledged the quality of the company and its management team, we also recognised that the valuation left little margin for error and huge scope for disappointment.

Initially, we were wrong. Enthusiasm around the stock continued to build and at its peak in 2021 GMO Payment Gateway traded at over 125 times earnings.

But the table below shows how the ensuing period played out for GMO Payment Gateway and the other growth and stable stocks we identified back in 2019, and just how disappointed investors in these companies would have been. Every stock failed to keep up with its demanding valuation and massively underperformed the rising TOPIX.

At the end of 2019, our portfolio’s positioning was in stark contrast to those areas of market enthusiasm – not just because many growth and defensive stocks looked nosebleed expensive to us, but because we were finding many attractive opportunities in the dirt cheap, overlooked half of the market.

Japan’s trading houses, companies such as Mitsubishi, Mitsui and Sumitomo, were emblematic of the ‘average businesses trading at excellent prices’ that we found attractive at the time.

These trading companies – complex industrial conglomerates that power Japan’s economy – traded at discounts to their book values, despite generating above-average returns on equity.

Since then, Mitsubishi and Mitsui have risen more than fivefold, with Sumitomo not far behind, up over three times. The share prices of these companies today don’t just reflect a better market appreciation of their underlying fundamentals but, in our view, now bake in over-enthusiasm around their future potential.

Undeniably, these companies have improved since 2019. All three have meaningfully stepped up shareholder returns, prompted by the Tokyo Stock Exchange’s push for greater capital efficiency.

But much of the enthusiasm also stemmed from Warren Buffett’s Berkshire Hathaway’s multi-billion-dollar investment in each of Japan’s major trading houses.

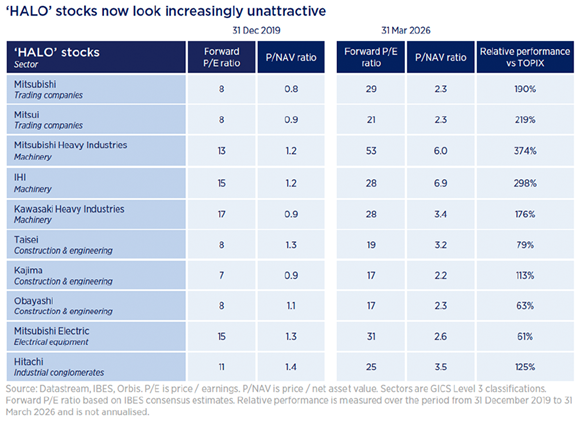

More recently, the popularity of the trading companies has surged as investors seek refuge in Japan’s so-called ‘HALO’ stocks – those with ‘High Assets’ and ‘Low Obsolescence’ that some hope will be sheltered from AI disruption.

The table below illustrates the journey that some of these HALO shares have been on since 2019. Each of these companies sits among the largest 100 companies in Japan and operates in an asset-heavy industry.

All 10 stocks now trade at multiples that one would normally associate with growth businesses, despite being inherently cyclical, and all have massively outperformed the index.

Just as in 2019, when investors crowded into the already overvalued growth and stable names, we believe that investors are now similarly at real risk of overpaying for these HALO names.

Our positioning today looks at odds with market sentiment. But we don’t take a different view just to be contrarian, we do so because of our hypervigilant focus on the price that we pay for the shares we buy.

Given the huge shift in the opportunity set, we are increasingly finding more attractive opportunities among Japan’s former growth darlings and far fewer in the popular HALO names.

In 2019, GMO Payment Gateway was a great example of market exuberance. Today it reflects the depths of market apathy. Despite growing its earnings more than fourfold since 2019, the stock has gone almost nowhere. Investors who bought shares in GMO Payment Gateway in December 2019 have seen a cumulative total return of just 17%.

Fundamentally, the business remains largely unchanged and we expect the company’s excellent track record of growth to continue, compounding earnings at 15-20% per annum over the medium term.

Yet the shares now trade at a much more reasonable 24 times our estimate of this year’s earnings. In stark contrast, Mitsubishi, which is expected to grow by just 5% per year over the next 3 years according to the latest sell-side consensus estimates, trades at 29 times next year’s earnings. It’s abundantly clear to us, at least, which stock is more deserving of investors’ capital.

GMO and Mitsubishi are symptomatic of how markets crowd into popular ideas long past the point of good value – then abandon good businesses when the narrative moves on.

The future is inherently uncertain, and markets will always swing between fear and exuberance. For disciplined, valuation-oriented investors, those swings aren't something to fear. They're the opportunity.

Alex Bowles and Brett Moshal are co-managers of the Orbis Japan Equity fund. The views expressed above should not be taken as investment advice.