UK small and mid-cap stocks are "a horror show" at the moment and the latest episode to keep them down was the increase in employer National Insurance (NI) from the latest Budget, according to Adrian Gosden, manager of the Jupiter UK Multi Cap Income fund.

In October 2024, Chancellor Rachel Reeves raised employer NI contributions from 13.8% to 15% and cut the earnings threshold from £9,100 to £5,000, with both changes taking effect from April 2025.

Poor government policy is the area where domestic companies are most at risk, with Gosden stating: “We've seen what damage it can do.”

He highlighted Whitbread, the owner of hotel chain Premier Inn, which cut 3,800 jobs earlier this year, citing the NI increase among the cost pressures behind a five-year restructuring plan.

Its management took the decision to Downing Street, which was “surprised," Gosden said. "They didn't realise that putting National Insurance up would cause this effect. That is shocking."

The new National Insurance policy also “halved the profitability of JD Wetherspoons”, the manager noted, calling the cumulative impact of NI on the hospitality sector "an absolute travesty."

However, the National Insurance issue is only the latest issue for beleaguered mid- and small-caps. The underperformance has been far longer than just the past few months.

[Removing housebuilders from here gives us a nice flow into the next section. You should always be thinking about how one sentence carries on from the last.]

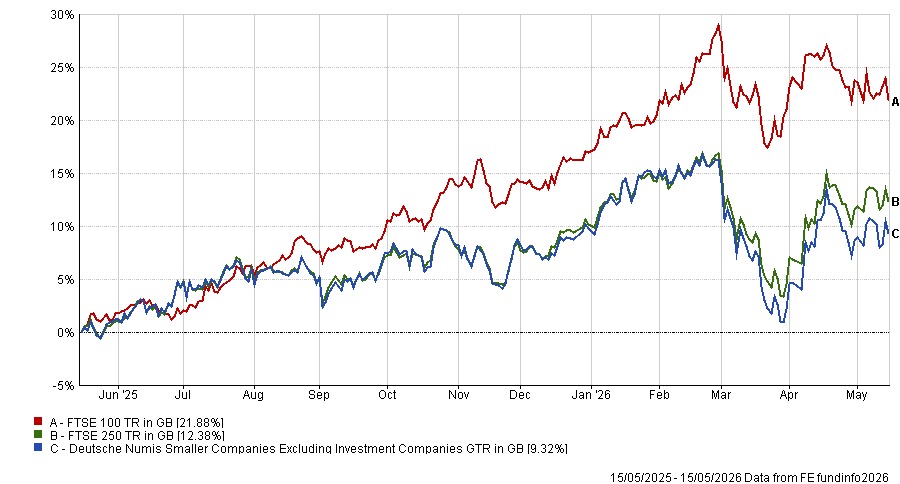

FTSE 250 mid-cap names have made just 19.6% over the past five years, while the Deutsche Numis Smaller Companies Excluding Investment Companies index is up just 14.6%.

This is compared with a 77% gain for the large-cap FTSE 100, as most of the larger UK companies are international earners whose performance has little to do with condition of the UK economy.

Names such as mining giant Rio Tinto (up 84% over 12 months) and oil major BP (50%) have thrived in the large-cap space.

Conversely, housebuilders, which tend to sit either at the bottom end of the FTSE 100 or the top end of the FTSE 250, have struggled. On average shares are also down 45% over 12 months, while companies making the roof tiles and bricks that go into those homes (commonly found in the FTSE 250 or below) are down 50%.

[Removing housebuilders from here gives us a nice flow into the next section. You should always be thinking about how one sentence carries on from the last.]

Performance of indices over 1yr

Source: FE Analytics

Disparities such as this have led to a large discount for smaller names – and that’s where the opportunity lies for Gosden, with even “a modest recovery in volumes [potentially delivering] outsized improvements in profits”.

"The SMID area below £3bn is trading at a 20-year discount to its larger brethren. I've seen it once before, and the returns the other side are spectacular," he said.

Gosden has his eye on a few SMID names, such as Marshalls – which makes paving, roofing products and solar panels. The stock trades on a price-to-earnings (P/E) ratio of just 8x.

Another is MJ Gleeson, which builds low-cost housing, which is included in the Jupiter UK Multi Cap Income fund on the basis that government housebuilding targets are being badly missed and political pressure to act is growing.

"A 1% improvement in the top line is a 20% improvement at the bottom,” Gosden said. "You would double your money as an investor, minimum”.

Hospitality is also on his watchlist. The problem here is the VAT gap: pubs pay 20% on food and drink while supermarkets pay 0% on most food, Gosden said, a point that was raised by JD Wetherspoons chief executive Tim Martin.

“Ireland levies 9% VAT on hospitality. There is the argument that if you lower the VAT on hospitality more people might actually go out and spend," Gosden said, "so you actually balance off your tax returns from the hospitality industry and don't actually lose out as a government."

Even without a policy reversal, the manager argued the businesses that have survived the cost pressure are now lean, their balance sheets intact, and they are positioned to benefit disproportionately from any recovery in volumes.

Performance of fund against index and sector over 1yr

Source: FE Analytics

To fund the SMID positions, he has been rotating out of stocks that have run ahead. SSE returned 86% over 12 months inside the fund and now yields 2.5% – well below the fund's own yield target. Defence stocks have performed similarly.

"When we see shares that do really well and no longer offer us income, the game is done for us," he concluded.

But building positions in these stocks is best done slowly. "I don't have a crystal ball," Gosden said. "We need to feel our way into these sorts of things."

Further government missteps remain the sharpest risk small- and mid-caps. Minimum wage, NI and packaging tax have already compressed margins with no sign of reversal and the operating leverage that could double profits if volumes recover works in both directions – lower volumes will hit hard too.