Fund managers carried out their largest single-month rotation into equities ever recorded in May, thanks to easing fears around the Iran conflict and a sharp recovery in profit expectations.

The May edition of the Bank of America Global Fund Manager Survey covered 170 respondents managing $461bn in assets and recorded a dramatic reversal from April’s deep pessimism.

The Iran conflict’s impact on investor sentiment lessened significantly in the new survey, with the number citing geopolitical conflict as the top tail risk more than halving. Most asset allocators also expect the Strait of Hormuz to reopen before the second half of 2026.

The macro picture improved sharply alongside the easing in geopolitical tension. Hard landing fears slipped to just 4% of respondents (down from 9%), stagflation expectations eased from 76% to 69%, and profit expectations flipped from expecting deterioration to expecting improvement.

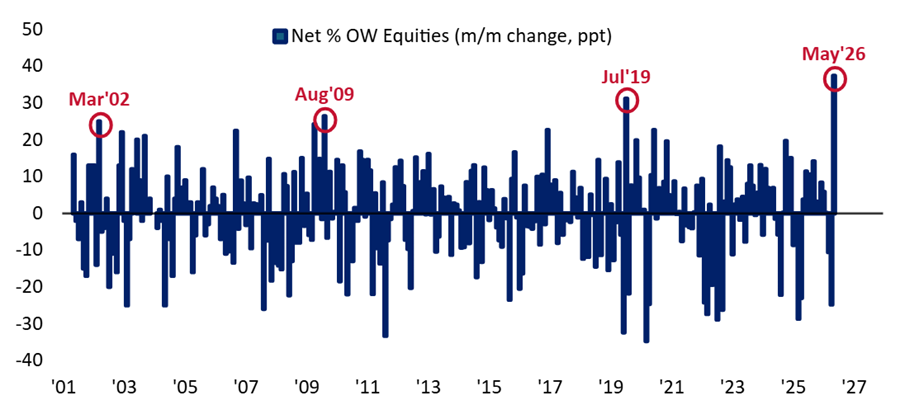

Monthly change in fund manager equity allocation

Source: BofA Global Fund Manager Survey, May 2026

Equity allocation surged from a net 13% overweight to a net 50% overweight in a single month, the largest monthly jump ever recorded in the survey’s history and the highest absolute reading since January 2022. Investors swung from net 24% taking lower than normal risk in April to net 6% taking higher than normal risk in May, while cash overweight fell from net 20% to net 3%.

Bank of America’s composite sentiment indicator, which draws on cash levels, equity allocation and growth expectations, rose from 3.7 to 6.6, recovering to its highest level since February. In April, the same indicator had fallen to its lowest reading since June 2025 as the Iran conflict dominated sentiment.

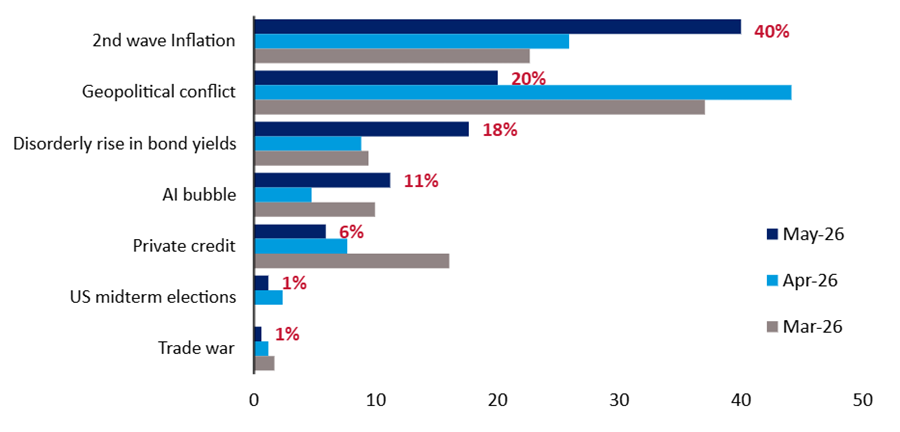

What fund managers consider the biggest tail risk

Source: BofA Global Fund Manager Survey, May 2026

Geopolitical conflict was cited by 44% of managers as the top tail risk, down from 20% last month. It held the top spot for two consecutive months before May's survey but has been displaced by a second wave of inflation, which rose from 26% to 40%.

Oil price forecasts edged marginally higher to $85 per barrel on a weighted-average basis by year-end 2026, up from $84 last month. This is a 39% increase from $61 at the start of the year.

A net 46% of investors regard oil as overvalued at current levels, the highest reading since August 2008, but only 26% expect Brent to trade at $90 or above by year-end, down from 28% in April.

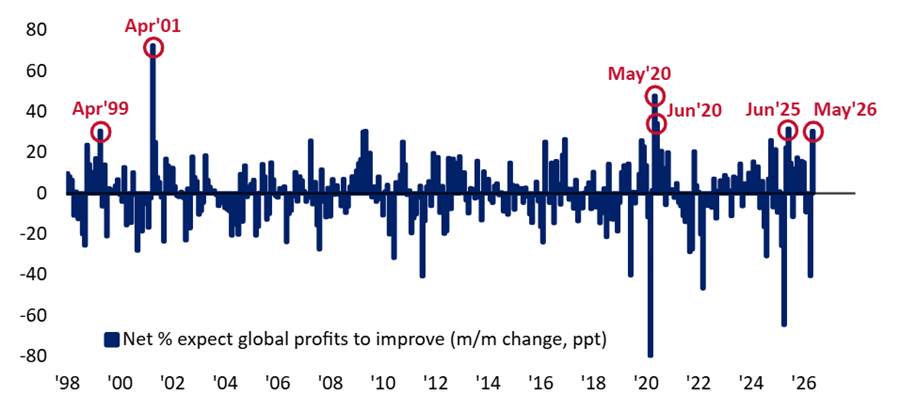

Net % of fund managers expecting global profits to improve

Source: BofA Global Fund Manager Survey, May 2026

Profit expectations recorded the sixth largest monthly swing on record in May, flipping from net 14% expecting deterioration in April to net 17% expecting improvement. Bank of America noted a record jump in the share of investors forecasting double-digit earnings per share growth.

Some 46% of respondents forecast a soft landing for the global economy and 39% expect no landing at all, although macro expectations remain negative. A net 14% of asset allocators expect the global economy to weaken in the coming 12 months, improving from a net 36% last month.

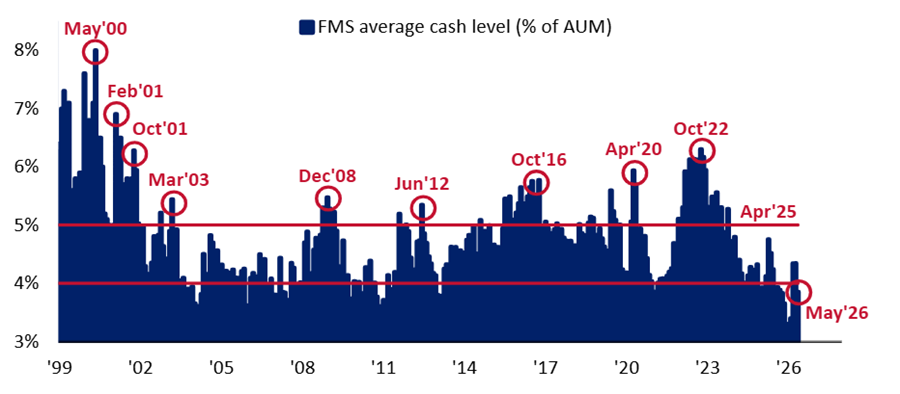

BofA FMS average cash level

Source: BofA Global Fund Manager Survey, May 2026

Cash levels fell from 4.3% to 3.9%, the biggest monthly drop since February 2024, triggering the bank’s contrarian cash-based sell signal, which activates at or below 4%. The median four-week loss from global stocks following the 24 previous sell signals since 2011 is 1%, though the largest recorded post-signal loss stands at 29%.

Bank of America’s Bull & Bear Indicator rose to 7.8, against a sell-signal threshold of 8. BofA said early June is “ripe for profit-taking”.

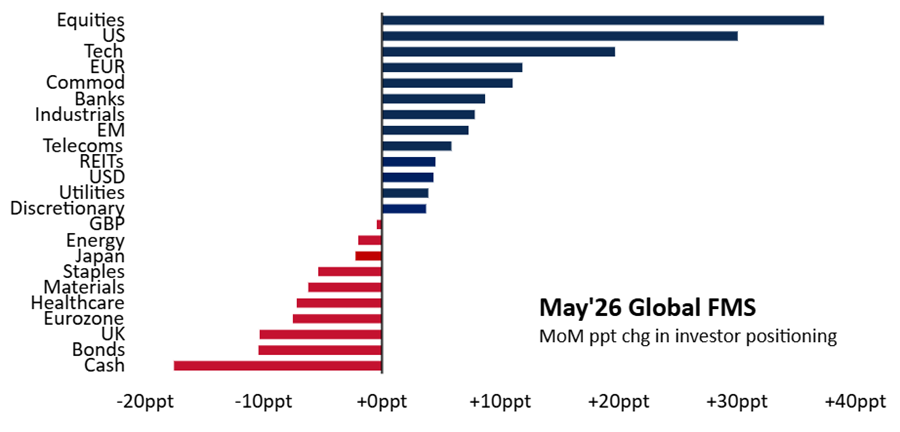

Monthly change in fund managers' positioning

Source: BofA Global Fund Manager Survey, May 2026

Managers added to equities, US stocks and tech stocks while cutting cash, bonds, UK equities and eurozone equities during May. US equities flipped from a net 10% underweight to a net 20% overweight, while eurozone allocation moved from net 4% overweight to net 4% underweight.

The allocation to tech stocks rose to a net 33% overweight from 14%, while bond allocation fell to a net 44% underweight, the deepest since June 2022.

Some 73% of respondents named ‘long global semiconductors’ as the most crowded trade, up from 24% in April, while the relative overweight in cyclicals versus defensives reached its highest level since January 2018.

Bank of America’s contrarian framework flagged that investors should consider paring length in commodities, equities, emerging markets and technology and semiconductors at current positioning levels.