This morning, Scottish Mortgage manager Tom Slater wrote in the company’s final results that its closed-ended structure means the trust is “not forced to sell companies at the point of listing", suggesting it will hold its main holding, Elon Musk’s SpaceX, “through the transition and beyond”.

Scottish Mortgage invested roughly £150m in SpaceX when it was still a private company, a position that is now worth several billion pounds. However, the fund will not sell when SpaceX lists on the stock market in mid-June.

“A listing changes the venue in which a company's shares are traded. The opportunity and our reasons for owning it remain the same,” Slater said.

SpaceX filed its IPO documentation with US regulators in April 2026. By the end of Scottish Mortgage's financial year, it had grown to more than 19% of the trust's assets – its largest single holding by some distance, and a degree of concentration Slater described as "highly unusual."

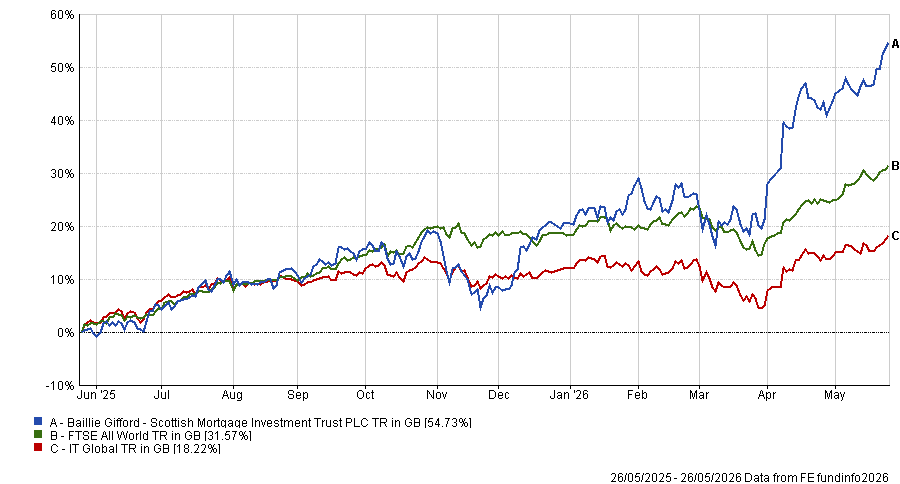

Performance of fund against index and sector over 1yr

Source: FE Analytics

As is standard ahead of a public listing, existing shareholders (including Scottish Mortgage) will be subject to a lock-up period, typically 90 to 180 days post-IPO, during which they cannot sell shares.

For open-ended fund structures, that constraint means they face redemption pressure from investors and are often required to reduce large single-stock positions well before any lock-up expires. An investment trust has no such obligation, which explains why the position was able to grow to its current size in the first place.

This outcome, Slater noted, was not available to passive investors or even some active managers “constrained by the need to stay close to an index, quarterly performance pressure or a prohibition on private companies”.

“It was available to us because of the specific structural advantages of a closed-end investment trust with a long-term mandate, patient shareholders, a board that judges the manager over years rather than quarters and the willingness to look foolish in the interim."

The manager has two reasons to keep holding SpaceX at these levels.

First, SpaceX is “the world's dominant launch provider and a global connectivity utility with the potential for software-like margins.”

The valuation, Slater said, has been driven mainly by Starlink, its satellite communications subsidiary. Starlink added 4.6 million new active customers in 2025, reaching 9 million across 35 additional countries.

A Pentagon contract for the Golden Dome missile defence programme illustrated how deeply SpaceX's infrastructure has become embedded in US national security, he argued.

The second reason is the demand for electricity to power AI, which is growing faster than grid capacity can keep up with.

Solar panels in orbit, Slater wrote, are up to 10 times more effective than those on the ground, operating outside the atmosphere and free from the day-night cycle. If Starship achieves the full reusability it is designed for, the economics of placing compute infrastructure in orbit "shift from speculative to compelling”.

“SpaceX is not just building a connectivity business,” Slater said. “It is positioning itself at the intersection of launch, energy and AI in a way that no other company on earth can replicate. That is why it is our largest holding.”

The manager does not avoid the concentration risk. A 19% position means Scottish Mortgage's net asset value will move sharply with SpaceX's share price in the months after listing, and the lock-up prevents any reduction if the stock falls.

“It would be remiss not to acknowledge the potential for volatility that comes with a position of this size,” he said. “We recognise that this makes the experience of owning Scottish Mortgage less comfortable than it would be if we managed the portfolio closer to a benchmark. The volatility is real and we do not dismiss it.”

The SpaceX IPO is also not a one-off. Scottish Mortgage holds several of the world's most valuable private companies, and Slater named Anthropic, Databricks, ByteDance and Stripe as realistic candidates for public listings in the coming years.

“We raise this not to speculate on timing but to point out that the assumption that private holdings are early-stage and speculative does not fit the reality of what we own,” Slater said.

“These are businesses operating at enormous scale, generating substantial revenues, and in several cases profits that would place them comfortably among the largest listed companies in the world.”