All markets and businesses have cycles, but when companies are going through drawdown phases it can be painful for investors and difficult to know what to do.

Kartik Kumar, part of the investment team on the Aurora UK Alpha trust, said investors tend to make mistakes when positions fall into the red, but these can be avoided.

To start with, it is important to know what a typical business cycle looks like. Kumar split it into six main sections. The first is the asset growing and a company’s price tracking higher as a result.

Next comes the start of the drawdown, usually when bad news hits. Here, the price falls far faster than the underlying value of the asset before reaching a floor, before then stabilising as investors appreciate that the news is not going to get worse – it does not necessarily have to be getting better either at this time.

Then there’s the turn, often triggered by marginally positive news that produces a disproportionate re-rating, followed by consolidation. In the last stage, the cycle begins again with price and value rising together.

This phenomenon comes from Richard Thaler's work in the early 1980s, which found that "prices fluctuate more wildly than value," Kumar said. More precisely, share prices move about 13x more than the discounted future cashflows that underpin them.

Each part of the cycle above is distinctly different and can last an unspecified amount of time. Kartik used Netflix as an example. The streaming service enjoyed rapid growth in 2021 and before tumbling just six months later. It then rebounded again quickly and enjoyed strong performance until the start of 2026.

Share price return (%) of Netflix over 5yrs

Source: Google Finance

At the opposite end of the spectrum, Phoenix holds Barratt among other housebuilders, which have long been falling and have yet to reach the floor, something that is taking “a lot longer than we would have anticipated”, said Kumar.

These episodes can mean companies get stuck at the bottom – or continue to fall – long after they perhaps should have. One reason for this is that people are “effectively wired like a smoke detector”, said Kumar. He compared investors selling at the first sign of trouble to a smoke detector bleating out when toast is burning. It is safer to take action just in case, although may not always be necessary.

Second is ‘anchoring’, where investors base their expectations on what has just happened rather than what is likely to happen next.

Kumar explained it is like driving by looking in a wing mirror: “What's in your wing mirror is a valid reflection of reality. It's just pointing in the wrong direction if you're trying to see what's coming.”

The third is career incentive: “Being wrong with the crowd is acceptable. Being wrong without the crowd is usually career-ending," he said.

Here he used the example of European banks at the start of the decade, which were viewed as capital-intensive, low-returning and uninvestable businesses.

Things have turned around in recent years and they have been one of the best-performing asset classes on the planet.

““But if you sat there in 2020 saying 'I think 13 trillion dollars of debt at a negative yield is irrational, and I think one day banks will earn a return from the spread on their deposits' – you wouldn't have had a job by 2022,” said Kumar.

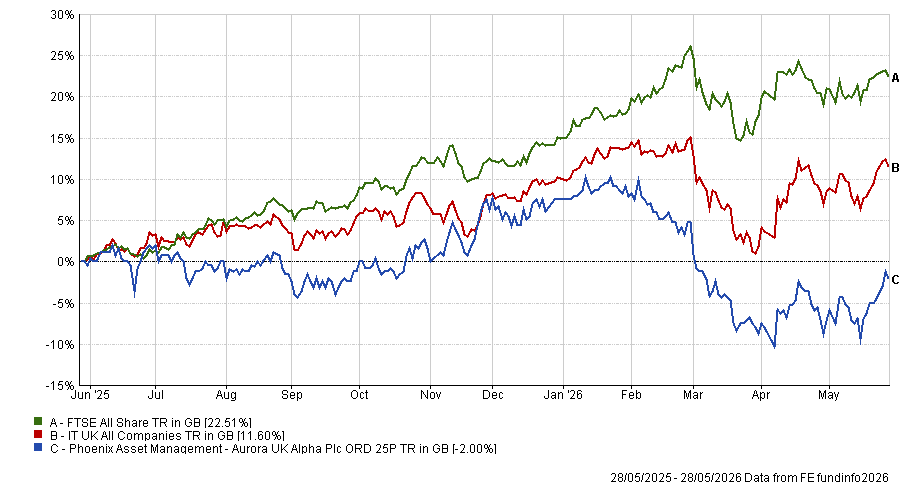

All of these are real issues for the Aurora UK Alpha trust. The fund is down 10.7% year to date and 5.6% over one year and is therefore going through its own form of drawdown.

Performance of fund against index and sector over 1yr

Source: FE Analytics

This is compounded by the trusts’ underlying holdings, such as Barratt, which have been weighed relative to the benchmark.

Yet he is content with his portfolio’s positioning, noting that he and the team are anchoring their approach to intrinsic value rather than short-term price changes, which is making it easier to hold stocks currently falling.

He used the example of Frasers, where £20,000 worth of shares currently buys around £48,000 of assets and wealth. This frame of mind has helped the team to retain conviction in Barratt despite multiple price drops. Having bought at £3, at around £2.40 he has given up 60p so far, but is “looking forward to that nine-pound gain” he expects from the company’s intrinsic value. “I can't predict when it will happen, but I know it will,” he said.

For his own portfolio, he estimated that the net asset value stands at around 243p versus an intrinsic value of 760p.

“The upside to intrinsic value on price is 220%, which is truly an extraordinary level in our history. There's a very significant margin of safety,” he concluded.