Ever since the UK voted to leave the European Union on 23 June 2016, the UK market has been beset with aftershocks, compounded by further political upheaval, a plethora of global crises and persistent investor scepticism.

Yet despite the backdrop – or rather because of it – investment trust managers speaking at a recent Association of Investment Companies (AIC) webinar argued that the UK now offers some of the most compelling opportunities in global equities.

Simon Gergel, lead manager of Merchants Trust, said: “The direct effect of Brexit on UK-listed companies is actually quite modest as there has been more of an effect on the market and on sentiment than on the companies themselves.”

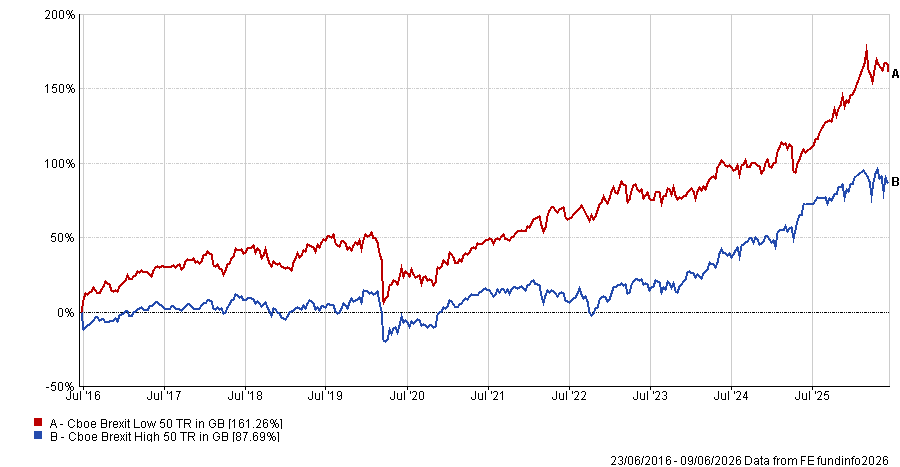

However, he did acknowledge that companies with higher international revenue streams proved more resilient. This is demonstrated in the graph below, where the 50 UK large-caps with the lowest exposure to sterling have outperformed the 50 large-caps with the highest exposure since the referendum.

Performance of Brexit Low 50 vs Brexit High 50 since 23 June 2016

Source: FE Analytics

The panellists argued that the long period of Brexit-related negativity has pushed UK valuations to levels that no longer reflect the underlying strength of British companies. The result is very attractively priced opportunities throughout the UK stock market.

Dominic Younger, lead manager of CT UK Capital and Income Investment Trust, summarised the consensus view: “The UK market is under-owned, undervalued and, in our estimation, unduly overlooked.”

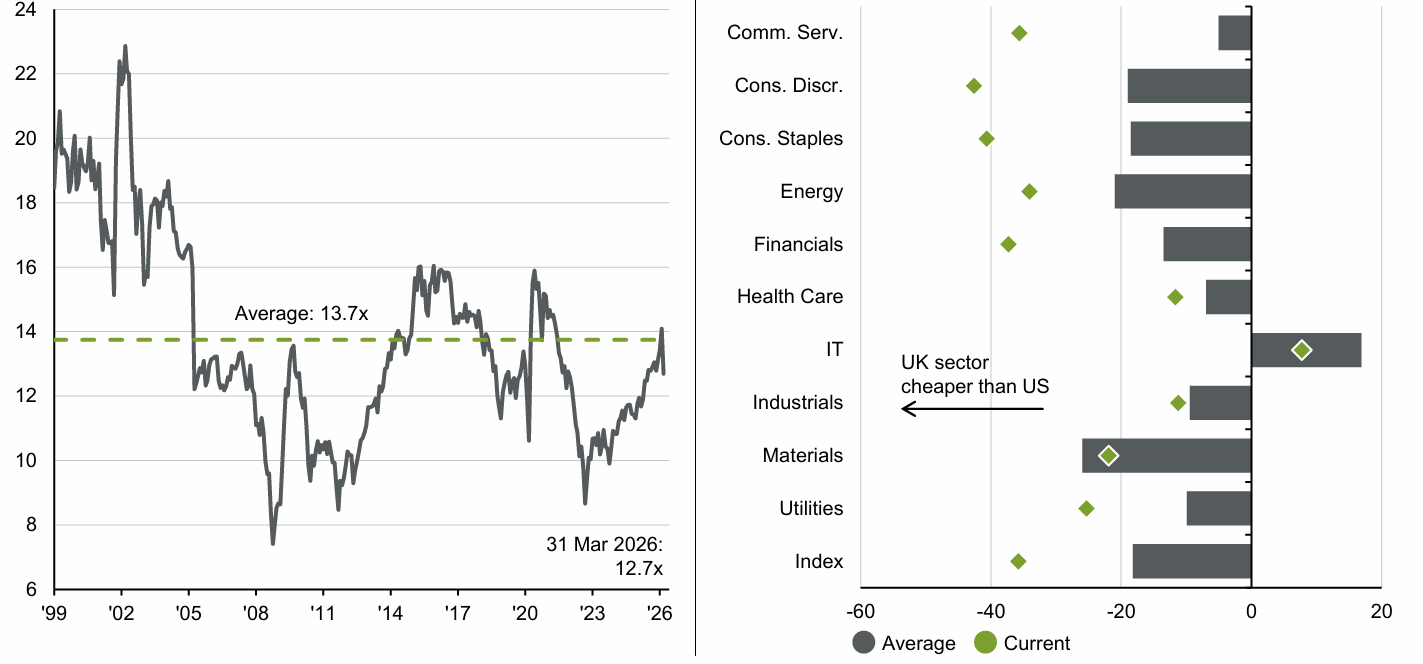

According to JP Morgan Asset Management research, the UK market was trading on a forward P/E of 12.7x as of 31 March 2026 – below its long-run average of 13.7x. In addition, the firm noted that the UK is trading at a discount to the US equivalent in virtually every part of the market.

UK FTSE All-Share forward P/E ratio (left), MSCI UK relative valuation vs the US (right)

Source: JPMorgan Asset Management. (Left) Forward P/E ratio is price to 12-month forward earnings to 31 March 2026. (Right) The percentage discount of MSCI UK on set 12-month forward P/E ratio vs the equivalent for the S&P 500, and the average since 1995.

Mark Niznik, co-manager of Artemis UK Future Leaders, said: “The median company in our portfolio is on 9x consensus P/E for next year, with consensus earnings growing by double-digits. They are returning over 20% on capital and have no debt. If that were a single company, we would be saying it is 50% undervalued.”

Investment trust managers have responded differently to the post-Brexit UK equity market.

For Gergel, the opportunity created by the sentiment gap has been most pronounced in the domestically oriented UK small- and mid-cap space, with Merchants Trust investing around 45% of its portfolio in such companies.

“If you look at our sector composition, these companies are in areas like real estate, retail and construction, which tend to be a bit more domestic and more mid-cap,” Gergel said.

Niznik said he has stuck with UK smaller companies, taking on the pain of that positioning over the decade.

Meanwhile, James Henderson, manager of Lowland Investment Company, said he has spent “several years hiding in large companies” – currently 49% of the portfolio versus a preferred 35%, although he is increasingly amenable to looking for opportunities at the smaller end of the market.

“We have got an opportunity to reduce the market cap and really make it count,” said Henderson.

“After all, we are now 10 years on from Brexit, we are getting through to the other side, getting a bit of certainty about our trading relations with Europe and the rest of the world, and so investment might be picking up again.”

The managers said the increase in merger and acquisition (M&A) activity and buybacks provides further support to the argument that the UK equity landscape is far more positive than the market perceives.

Niznik, who is also co-manager of the Artemis UK Smaller Companies fund, said it has logged 37 takeovers in the past six years at an average premium of 48%, and that the level of small-cap share buybacks is at “absolutely unprecedented” levels he has never seen in his 40-year career.

“What it tells me is three things: companies have surplus capital with which to do these buybacks, companies think their shares are cheap so are buying them back and companies think the outlook is good enough to spend that permanent capital rather than husband it for the rainy day everyone else thinks is coming,” he said.

However, while the managers said they are hopeful the UK equity market will re-rate, exactly when this will happen is open to debate. The Middle East conflict and interest rates were cited as immediate swing factors, temporarily stemming the growth in confidence that had been returning in January and February of this year.

“The benefits of the interest rate cuts we have had to date have not yet come through to the economy – these have been pushed back by what’s going on in Iran,” Gergel added.

Although these factors are keeping UK negativity high, Niznik is confident that a recovery in confidence will allow crucial market stimuli like consumer spending to bounce back.

“The trouble is that it is difficult to judge the timing – but this is why we take a three-to-five-year view,” he said.

That longer-term perspective is particularly pertinent for small-cap investors, as smaller companies have endured the second-longest and second-most severe period of underperformance since 1955, Niznik added.

Crucially, he argued that a full recovery in conditions is not required for investors to benefit.

“Our portfolio is cheaper than the UK small-cap benchmark and the investment trust is on a double-digit discount to that,” he said.

“The future does not actually have to be that good – slightly less bad would be good enough for some decent returns as that coiled spring releases.”

For now, the investment trust managers acknowledged that sentiment towards a post-Brexit UK, while improving in patches, has yet to translate into sustained inflows.

As Henderson put it: “It is about climbing walls of worry that make markets go up and we have got a long wall to climb here.”