The rapid expansion of AI has largely been an equity story, but the biggest, cash-hungry players are increasingly turning to bond markets to fund themselves, which will have implications for investors.

Damien Hill, co-manager of BNY Strategic Bond, said: “The AI hyperscalers have been borrowing probably 15-20% of all US investment-grade issuance over the year to date, which is gargantuan.”

Issuance is accelerating alongside the race to build-out data centre capacity and while it is “nowhere near the concentrations that are already there in the equity market”, Hill warned that, if hyperscalers continue at this run rate, bond markets may well reach the same levels.

“At which point, you will have a lot of investors wanting more diversified portfolios and not liking that degree of concentration,” he said.

Recent activity illustrates how quickly bond markets are changing.

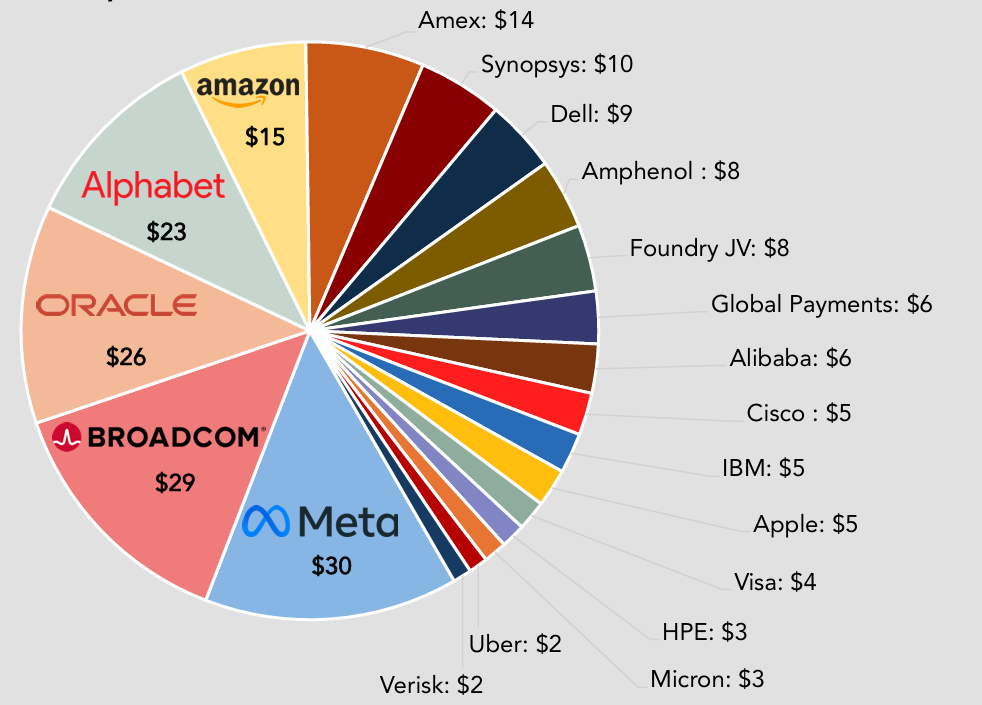

In 2025, the largest hyperscalers – including Amazon, Alphabet, Meta and Oracle – issued around $120bn in US corporate bonds versus an average of $28bn per year between 2020 and 2024.

2025 US tech stock AI bond issuance (in USD)

Source: MUFG Bank

Morgan Stanley forecast that AI-related global debt issuance will more than double in 2026 to reach $570bn, driven by sizeable increases in hyperscalers’ capital expenditure plans. As of 31 May 2026, global debt issuance linked to AI was already estimated at $236bn.

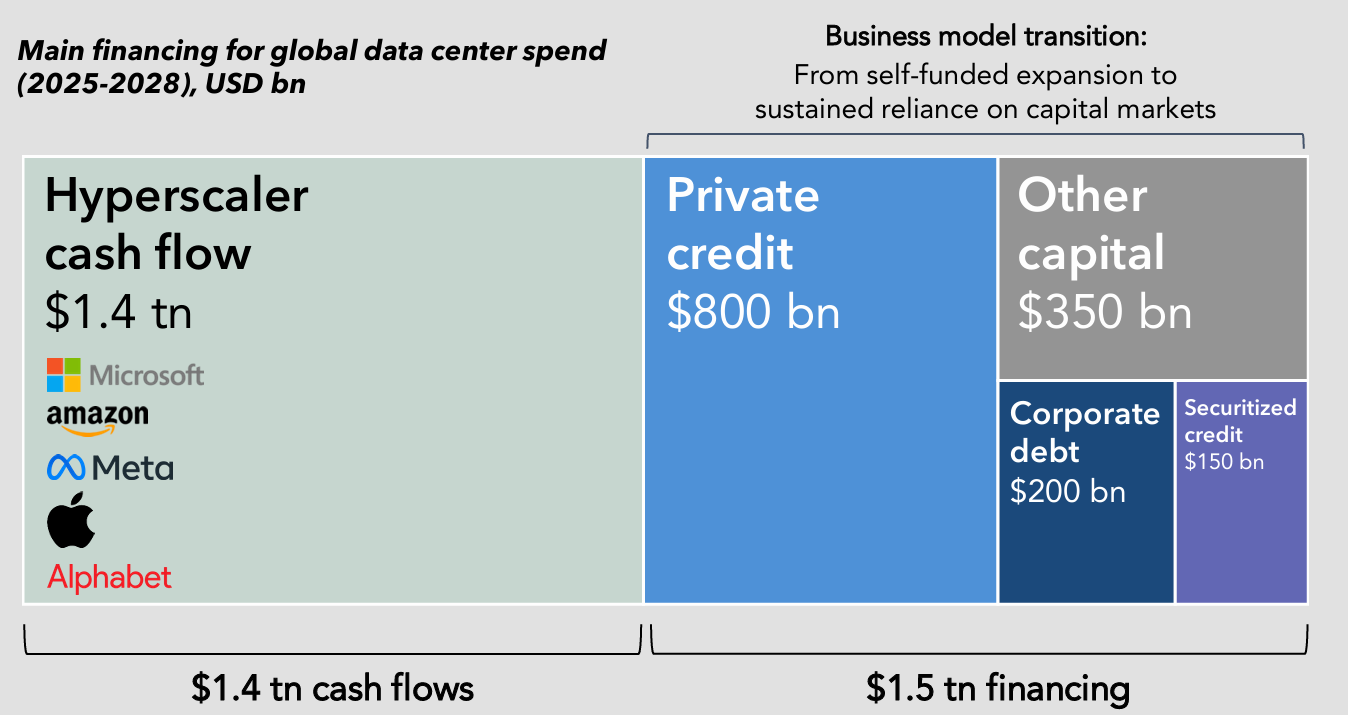

Japan’s MUFG Bank has predicted the hyperscalers will spend $1.4trn between 2025 and 2028 on global data centres, with an additional $1.5trn coming from private credit, corporate debt, securitised credit and other capital.

Data centre spend, 2025-2028

Source: MUFG Bank

This scale of debt is not only being raised in the US, with hyperscalers turning to foreign currencies too.

Amazon sold $14bn of Canadian dollar high-grade bonds and €14.5bn in euro-denominated bonds, while Alphabet sold ¥576.5bn in yen-denominated bonds and launched a 100-year bond in sterling markets. The last tech company to issue a ‘century bond’ was Motorola in 1997.

“They are borrowing at levels that are making other borrowers with similar credit ratings look expensive – because the hyperscalers are all rated ‘AA’ or ‘AA+’, which is comparable to US treasuries or the UK government – and they are coming at quite cheap levels already,” Hill said.

“There is a scenario where they could crowd out other parts of the market and create some indigestion.”

But not all AI issuers carry the same level of risk, which means closer scrutiny is essential.

Richard Jones, portfolio specialist at Insight Investment, said: “Bottom-up credit analysis is needed – investors have to be confident in their fundamentals, their management team and their business model,” he said.

“If you look closer at the hyperscalers, some of them don’t have the same fundamental strength as others. It’s not a completely even market out there.”

One big AI player that has drawn some concern is Oracle. Last September, it tapped the bond market for around $18bn to fund its planned AI-related spend and its debt-to-equity ratio surged to 500%.

“Some of these companies are flying a lot closer to the sun, given the amount of cashflow they currently generate and how much they are betting on AI,” Hill acknowledged.

“Our analysts do the stress testing to assess how narrow a path a company is having to walk to make their investment in AI work – that AI bet will clearly have to be heavily priced into their bonds, otherwise we won’t look at it.”

Hill said that Oracle’s bonds are “considerably wider” – more yield, more extra spread – than higher quality names.

“We are talking multiple notches different, and then the cashflow generation is minimal relatively, given the amount of debt they have already strapped on.”

Earlier this month, Oracle’s stock dropped by as much as 10% after the cloud giant’s higher-than-expected capex plans fuelled concerns over its already high AI-related costs.

Stock price performance over 1yr

Source: Google Finance

For diversified fixed-income investors, the question is how to position around this wave of issuance.

Jones said the answer lies in using the full breadth of the bond universe.

“Within fixed income, you have tech sectors that are incredibly exposed to this theme of AI capex issuance but on the other side you have old economy utility sectors, which are quite insulated from that and can act as a natural hedge if there is any weakness within the tech sector,” he said.

Hill agreed, noting that utilities and telecommunication companies typically lend themselves much more to a consistent cashflow to pay debt back.

He added that there are other avenues to access the AI trade. “There are more asset-backed security-style structures backing data centres, for example,” he said, though emphasised that these also require rigorous bottom-up analysis.

Hill said they are keeping their approach “tactical” rather than allocating wholesale.

“We are not saying this is a massive buy across the board because there is so much more potentially to come,” he said.