The Federal Reserve kept its benchmark interest rate unchanged at Kevin Warsh's first meeting as chair on 17 June but projections from committee members pointed to possible rate rises before year-end, catching most analysts off guard.

The rate-setting federal open market committee (FOMC) voted 12-0 to hold the federal funds rate at 3.5% to 3.75%. The accompanying statement was brief, containing no forward guidance, removing a hint it was leaning towards lower future interest rates and concluding: "The Committee will deliver price stability."

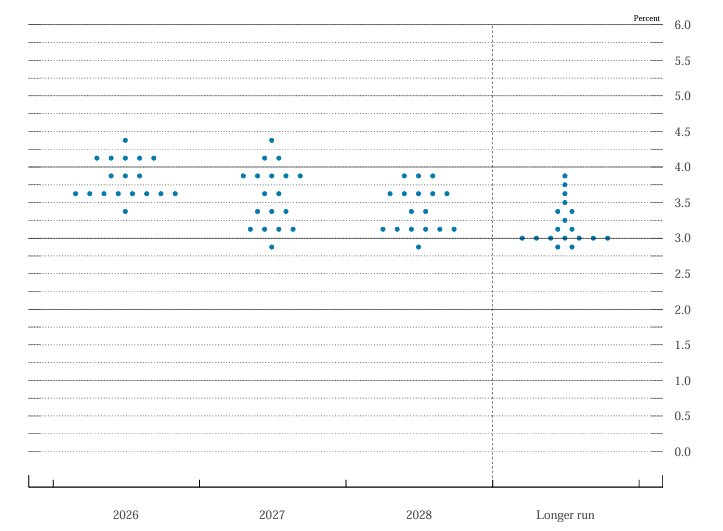

The summary of economic projections showed nine of 18 FOMC participants expect policy tightening before year-end. There should have been 19 but Warsh did not submit his own projections.

Three favour increases of 25 basis points, five favour 50 basis points and one favours 75 basis points. The median projection for the federal funds rate at end-2026 moved to 3.8% from 3.4% in March.

FOMC dot plot

Source: Federal Reserve

Neil Wilson, investor strategist at Saxo UK, said the statement's brevity and its omission of the Fed's employment mandate were significant.

"An incredibly short statement – the headline for me was that the Fed 'will deliver price stability'. No fluff. And no reference there to the labour market side of the dual mandate, which tells us a lot about where the Fed is right now. As stated today, the Fed is short one side of the dual mandate and it's not employment. That statement shows it's minded to hike. How does Trump take this?"

Wilson also pointed to the fact that Warsh had not submitted his own projections: "A missing dot on the plot... Warsh stuck to his guns and refrained from publishing his views. Otherwise the dots were hawkish, which says a lot."

The dot plot was more hawkish than Pantheon Macroeconomics had expected.

Economists Samuel Tombs and Oliver Allen had forecast only three participants would signal hiking before year-end. They said last week's inflation data was likely a factor in the shift: May's CPI and PPI figures collectively imply core PCE inflation rose 0.4% in the month.

Two-year treasury yields rose by approximately 10 basis points after the decision. Wilson said front-end rates moved higher on expectations of a tighter Fed while longer-dated yields fell, suggesting markets may already view the new regime as more credible on inflation.

"Warsh is not giving the market a heck of a lot of rope with which to hang him, which has to be a good thing," Wilson said.

Warsh did not disclose his own policy views during the press conference. He announced five new taskforces that will examine the Fed’s communications, the balance sheet, data sources, AI's impact on productivity and jobs, and the drivers of inflation.

Tombs and Allen said the decision not to submit projections made political sense. A rate cut forecast would have drawn accusations that Warsh was acting on behalf of the White House but a no-change forecast risked antagonising the administration.

Stuart Clark, portfolio manager at Quilter, said the hold was the only realistic option: "Kevin Warsh has kicked off his chairmanship of the Federal Reserve with a hold in interest rates, signalling the regime change that many expected may have to wait.

"Ultimately, Warsh and the Fed board had little choice but to keep rates where they are."

Clark noted that energy prices had not returned to pre-conflict levels following the US-Iran memorandum of understanding and were unlikely to do so.

"This situation is entirely of the US' own making and with energy prices likely to remain elevated relative to the start of the year, inflation isn't going to suddenly begin to fall," he said.

President Trump, Clark added, "will likely remain as frustrated with the new leadership as he was with the old one".

Pantheon Macroeconomics' Tombs and Allen said the hawkish projections should be read as a communications strategy rather than a commitment to act.

"Yesterday's communications are best viewed as an attempt by the FOMC to anchor inflation expectations and therefore reduce the likelihood that interest rates actually will need to be hiked," they said.

Warsh's own comments supported this view, telling reporters that FOMC participants "didn't feel bound by them six weeks from now or six days from now, in the event that their circumstances change" by their projections and that he "didn't hear tons of conviction".

Tombs and Allen also noted that the Fed's legal mandate had not changed. Section 2A of the Federal Reserve Act requires the FOMC to pursue maximum employment alongside price stability. They said most voting members would be unlikely to support rate rises if unemployment drifts above the FOMC's own median projection of 4.3% later in the year, as Pantheon expects.

But the analysts reached different conclusions on what the Fed will do next.

Wilson said a rate rise next month was possible. He noted that the new communications approach means markets will not receive advance warning of decisions: "I think it could happen as early as July and the good thing about this new-look Fed is that we won't get to know until the meeting!"

Quilter's Clark said a rate rise before year-end was a possibility. He cited inflation at a three-year high of 3.8%, alongside better-than-expected employment data and consumer spending figures released on the day of the meeting. It was, he said, "not out of the realms of possibility that the Fed will have raised rates by the end of this year, instead of cutting them as was expected at the start of 2026".

Tombs and Allen maintained their view that rates would remain on hold in 2026: "We still think, however, that the committee likely will keep rates on hold this year". They said energy prices were squeezing household incomes without driving wage growth or broader price increases. High borrowing costs and the effect of AI on hiring were also weighing on employment. Their forecast is that the Fed cuts rates by approximately 75 basis points in spring 2027 to address rising unemployment.

Clark argued that Warsh's position on artificial intelligence could shape the rate path.

"Warsh is of the opinion that artificial intelligence will usher in a disinflationary period as productivity increases and the cost of doing things falls. This is a punchy prediction and could easily end up proving wrong given the current debates around return on investment from AI, but it may just be the cover he needs to begin the move to bring interest rates down and appease the president," he explained.