The artificial intelligence rally has made many fund managers uneasy, but none more so than Julian Bishop, manager of the £637.8m Allianz Brunner Investment Trust, who is now weighing what to do with his AI exposure.

Bishop has held positions in Taiwan Semiconductor Manufacturing Company (TSMC) and ASML through the rally, watching them become exceptional contributors to performance. But that success has made him question himself.

“We are already underweight tech and we're mindful that this is a big technological revolution – we want to participate in the boom. But we're students of history. We've seen the railroad boom of 1873, 1929, the dot-com bubble, the housing crisis. We've seen frenzies before,” he said.

He did not call AI a bubble but was wary of what happens to those who did: “If you called bubble two years ago and everything keeps going up, people become embarrassed. Actually, the relatively late stage of a bubble is when the detractors are sucked in. They say ‘I was wrong’ and they buy in – and then it goes wrong.”

Below, Bishop explains the philosophy behind the trust, where he is finding value today and what it would take for him to pull the trigger on his most profitable holdings.

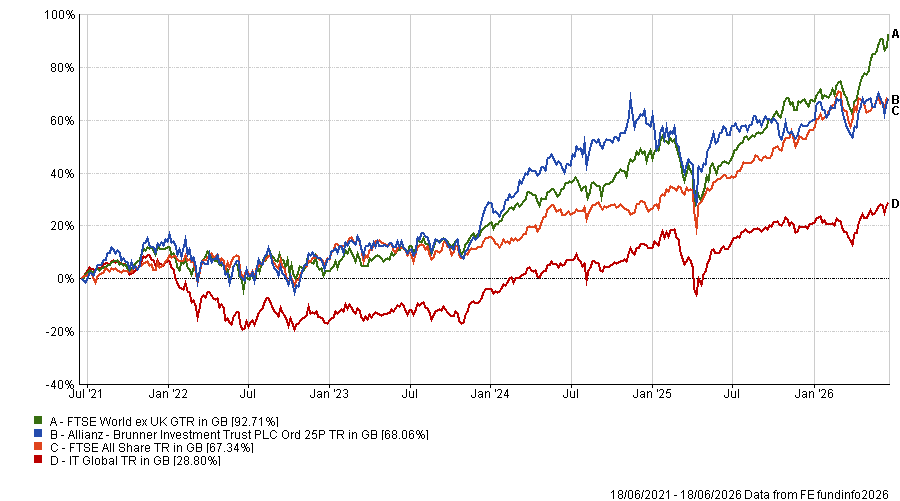

Performance of fund against sector and benchmark over 5yrs

Source: FE Analytics

Please describe your philosophy and process.

We see each of our equity holdings as a cash flow stream and we want to get to a point where, when we forecast cash flow streams and model them, everything seems realistic and prudent. We are looking for names where if markets were to close tomorrow, we'd be happy just to own them and live off the cash flow stream.

We put a lot of emphasis on diversification – making sure that the cash flow streams we buy when we buy our equities are never too correlated. There's emphasis on downside protection and risk.

The benchmark is 70% global, 30% UK. Having a 30% weight in the UK, where you have more asset-heavy, cash-interested businesses, is a very sensible place to be at the moment, when the global market is so dominated by the United States and tech.

Why should investors pick Brunner over the competition?

We want to make money without taking stupid risks. Over the last five years we've delivered around 10% per annum in NAV growth. We have not entered the realm of ludicrously valued concept stocks and we have simultaneously not just gone for very defensive companies that have struggled to grow.

We're nowhere near as ideologically extreme as the likes of a Lindsell Train, which is all about consumer staples and asset-light businesses – a lot of which have really struggled because of fear of disruption by AI – or a Scottish Mortgage, that has SpaceX.

We have this all-weather framework: a wide range of uncorrelated equity investments that are as good quality as possible, grow as much as possible and are as good value as possible.

Where are you finding the most interesting opportunities right now?

A lot of what we're doing recently is turning up the value dial. In the US we're concerned about valuations and in the tech sector about speculation. The prudent thing is to go into slightly less glamorous businesses where there's more cash flow on offer.

As tech and semiconductors and AI have roared ahead, pretty much everything else has gone either sideways or down. That's particularly acute in asset-light businesses like software where there's widespread fear of disruption. We've been nibbling in those areas.

Do you have any examples?

Booking.com is one. It’s in a strong market position, good growth tailwinds and sold off hugely. Now you get a very good free cash flow yield. The company has negligible debt and can return all that cash via large buybacks.

Similarly, credit rating agency Equifax somehow got wrapped up in the AI sell-off. We don't think it's likely to be affected at all.

We also bought a little of RELX, having previously sold it at a very high multiple. We bought it back at literally half the price. And more recently, Progressive, a plain-vanilla US auto insurer. The PE [price-to-earnings ratio] is 11 or 12x, roughly half the overall US market. They're starting to get real scale benefits from the share they've won and we think they may be developing sustainable competitive advantages.

You still hold TSMC and ASML, which are among the market's most loved AI plays. Why haven't you sold if you’re so nervous?

In both cases, they're virtual monopolists with incredible barriers to entry. We've stuck with those. We're more reluctant to get involved in other areas of semiconductors where competitive advantages may prove to be very short-lived. There's such a scramble for all things semiconductors as the AI build-out takes place and super-normal profits being made. That strikes us as far more cyclical and unlikely to sustain.

But we are nervous. They've re-rated quite a lot and their earnings are high because these businesses are correlated with the AI capex cycle. The semiconductor market has always been prone to boom and bust.

What would prompt you to sell?

If there was mounting evidence that OpenAI and Anthropic were struggling to monetise or grow revenues at a rapid pace, that would be very worrying. If any of the big tech companies said they were going to cut AI capex, that would be a real red flag: at that point you'd see a big down cycle in semiconductors. We have already seen some signs of that. Oracle recently said they think capex is going to peak in 2028 and strongly implied it will come down after that.

If evidence mounts in this direction, we're kind of ready to sell. There are no sacred cows.

What were your best and worst calls over the past 12 months?

Google has been the biggest single contributor to performance over the past year (through the end of May), contributing around 3.7% to absolute performance. The trust began acquiring shares in May 2024.

TSMC, which we’ve held for more than 15 years, has also been terrific, contributing around 3.2% to absolute performance to the end of May.

A little more unusual is Kia, the South Korean car company. It’s a very deep value name – we paid a PE of around 2x cash for that. That's been really good for us, with a 1.1% contribution.

On the negative side, by and large it's been those perceived as AI losers. It's been a very binary market. The worst was Autotrader, the UK online used-car marketplace, which cost 1.2% of absolute performance.

The market has been going from one digital business to another, de-rating them on the basis that a change in technology will somehow weaken the barriers to entry that support their economics.

We decided to keep Autotrader, and it's been very dramatically de-rated. The shares went down 40%. No huge operational problems; profit forecasts came down slightly for unrelated reasons. It was really a sentiment issue.

What do you do outside of fund management?

I like opera, classical music and football.