More than half of limited partners (LP) expect the number of private equity ‘zombie funds’ in their portfolios to rise, according to the latest edition of the Coller Capital Global Private Capital Barometer.

The barometer, which surveyed 108 LPs collectively overseeing more than $2trn in assets, found 54% of investors think their portfolio will hold more zombie funds over the next two years. A further 31% expect them to remain stable, while just 15% expect a decrease.

A zombie fund is where a general partner (GP) is prolonging a fund’s life in order to maximise management fees. This means an LP’s capital is locked in illiquid assets with limited returns.

“Private equity’s longer holding periods, plus the elevated entry valuations that some firms paid before interest rates rose, appear to be coming home to roost in investor portfolios,” Coller Capital said.

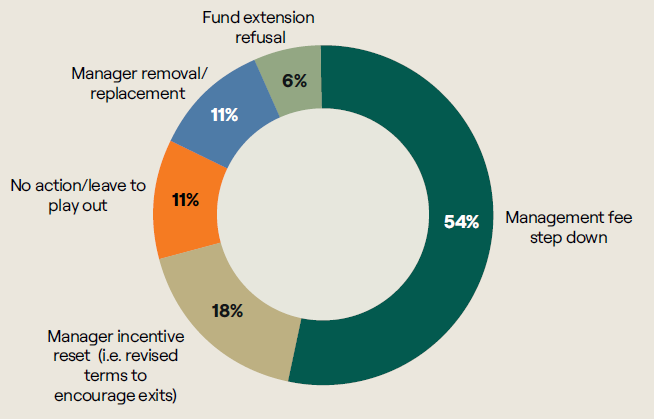

The survey found LPs hope to avoid confrontational solutions to the problem, with 54% of respondents saying the preferred response in no-fault situations is a management fee step-down. Manager incentive resets to encourage timely exits came second at 18%, while manager removal and taking no action were each favoured by 11%.

LPs’ preferred approach to no-fault zombie funds

Source: Coller Capital Global Private Capital Barometer

The zombie fund concern sits within a broader trend of increasing selectivity. Almost a quarter (23%) of LPs plan to reduce the number of GP relationships across their private markets portfolios over the next three years, up from 16% when Coller Capital last asked the question in 2020.

Despite this, LP commitment to private markets remains resilient, with a third expecting to accelerate their rate of commitments, while 57% expect their pace to remain the same over the next two years.

Geopolitics is also becoming a more significant input into allocation decisions. Just over a third (37%) of surveyed LPs said the geopolitical environment and outlook are influencing their private markets allocations more than in the past.

The effect is more pronounced outside North America, with nearly half of European (46%) and Asia-Pacific (47%) investors citing greater geopolitical influence on their decisions.

Against that backdrop, continuation vehicles appear to have become an established feature of private markets rather than a temporary response to subdued exit conditions. GP-led secondary volume reached approximately $106bn in 2025, a record level achieved even as broader exit activity remained constrained.

Some 40% of LPs expect new continuation vehicle activity to continue increasing even when traditional exit channels improve. A further 29% expect it to remain at current levels, while 31% expect it to decline.

Jeremy Coller, chief investment officer and managing partner of Coller Capital, said: "Recent high-profile public market moves have put the exit window back at the centre of the conversation. That is encouraging, but it would be wrong to see IPOs and secondaries as competing routes to liquidity. The barometer makes it clear that they are complementary.

“Secondaries have become a core route to liquidity and a central part of how LPs allocate, rebalance portfolios and retain exposure to assets they continue to have conviction in. Two-fifths of LPs in this barometer expect continuation vehicle activity to keep growing even as traditional exits recover, which tells you something about how structural this shift to secondaries has become."

LPs rank private credit as the asset class most likely to see the greatest proportional secondary market growth over the next three years, at 36%, ahead of private equity, infrastructure and venture capital. This points to a shift in how investors may seek exposure to the asset class, with greater emphasis on seasoned assets, portfolio rebalancing and active liquidity management.

After several years of rapid expansion, private credit allocation intentions have cooled. The proportion of LPs planning to increase their target allocation to private debt or credit over the next 12 months fell from 42% in the previous barometer to 29% in this edition.

But only 18% of LPs believe there is a systemic problem in private credit, while 53% see isolated risk above initial expectations and 29% are comfortable that risk is in line with expectations.

Respondents are not aligned on whether GPs are striking the right balance between providing liquidity and allowing portfolio companies more time for value creation. While 40% believe GPs are generally getting the balance right, 39% say GPs are not providing liquidity early enough and 22% say some of the best companies are being sold too early.

LPs expect artificial intelligence to reshape private markets operations but do not yet see it primarily as a source of alpha. Some 70% expect GPs to use AI mainly as a cost-efficiency tool over the next five years. Just 22% see it as a driver of return outperformance and 8% see it primarily as a risk-management tool.

Two-thirds believe AI adoption by GPs will widen return dispersion between stronger and weaker performers. Among LPs making fund and co-investment decisions, 61% said the importance of gut instinct has not changed while 22% said it is increasing.