An AI bull admitting that money is being wasted on artificial intelligence might sound like a contradiction but Stephen Yiu, manager of the WS Blue Whale Growth fund, doesn't see it that way.

“At this moment in time, I would agree that money is being wasted, but that overinvestment is more of a use-case-specific issue,” he said.

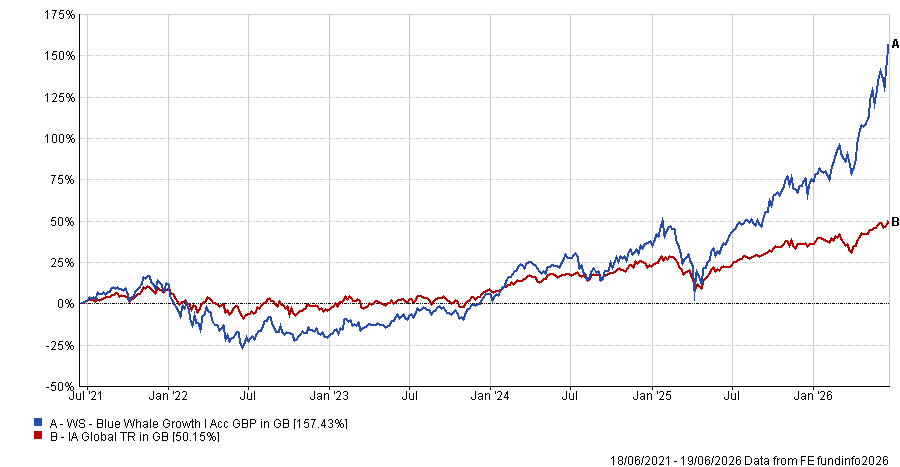

Since launch in 2017, Blue Whale has returned 402% against 125% of the average IA Global fund and maintained a first-decile performance over the past five, three and one year as well. As AI has grown, so has the portion of the portfolio that is exposed to the sector and to the infrastructure enabling its growth.

Performance of fund against index and sector over 5yrs

Source: FE Analytics

The manager’s argument is that wasting capital and opportunity are not mutually exclusive.

“Google Search was the seventh search engine created,” he said. “The other six are gone. But it doesn't make online searching unreal.”

It was the same for social media: there were dozens of platforms to begin with but then only a handful of survivors and along the way, capital was destroyed. But the market that emerged was larger than the sum of the companies that competed for it.

Yiu made an analogy with padel courts. A popular sport, new courts have been appearing across cities as supply is racing to meet demand and, in some places, outpacing it. Capital cycles behave the same way, whether the underlying asset is a tennis derivative or a data centre.

“That is a natural part of technological advancement,” Yiu said, “and ultimately the winner of tomorrow will consolidate the entire market.”

Trying to identify which AI application will win is the wrong question, however. What matters is what each of them leaves behind for others to exploit.

“If OpenAI just dropped out, whatever it has built in terms of physical infrastructure could be used by any other AI player,” he said. “So that's not an overinvestment.”

The hardware layer, made up of GPUs, high-bandwidth memory, optical networking and liquid cooling, is “fungible” because whoever wins the application race will still run on the same infrastructure.

This is also how Blue Whale has been justifying its largest portfolio positions. Holdings such as SK Hynix (South Korea) supply the advanced memory AI workloads require; Lumentum (California) enables the optical networking infrastructure that moves data between servers.

Alphabet sits at the other end of the spectrum: a full-stack position spanning AI research, custom silicon, cloud infrastructure and consumer distribution at scale.

These are the businesses where “the bottlenecks sit lower down the stack”, in hardware that is difficult to manufacture, constrained by supply and capital-intensive to build.

“Instead of picking the AI winners of tomorrow,” Yiu said, “it makes more sense to position yourself within the AI infrastructure companies that are already receiving all the spending. They are already winning.”

On the other end of the spectrum are companies such as LSEG in the UK, which have de-rated strongly after being deemed AI losers by the market. Yet a number of managers have recently came to see them in a better light, for example Finsbury Growth and Income’s Nick Train and Personal Asset’s Sebastian Lyon, as Trustnet recently reported.

Blue Whale holds a small position in LSEG: it has proprietary data, built over decades, running through financial markets infrastructure that clients depend on daily. Its Workspace terminal – a Bloomberg competitor fed by LSEG's own data – represents exactly the kind of embedded product that is difficult to displace. But Yiu argued the company is not moving fast enough to capitalise on what it has.

“LSEG could be an AI winner, because they do have the data,” he said. “But AI is moving very quickly, and they are not moving quick enough.”

For businesses like LSEG, technology has historically been an enabler rather than a threat, Yiu continued. Management teams built for that environment may not be calibrated for one where the disruption risk is real and the window to respond is narrowing.

“The management team would need to be more focused, because it's a very competitive environment,” he said. “The clock is ticking.”