Banks currently offer one of the best risk/reward trade-offs in the market, according to TM CRUX UK Core manager Jamie Ward, who says he has one of the highest weightings to the sector of any of his peers.

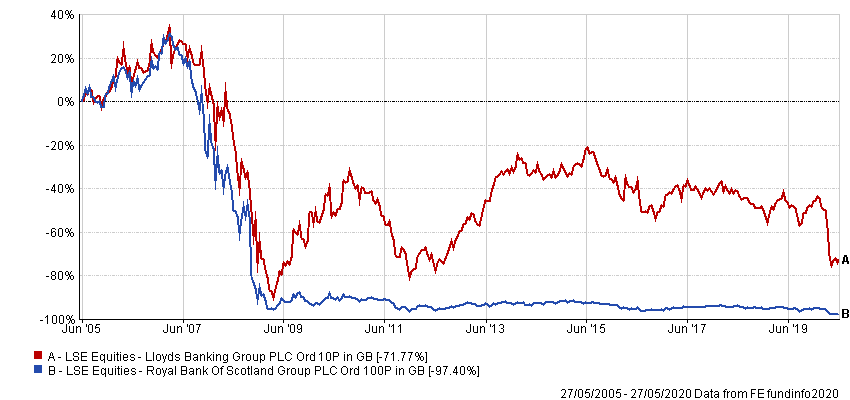

Banking stocks have plummeted this year, due to their high gearing to the economy and the decision to temporarily stop dividend payments and share buybacks. The share price of RBS is now below its post-financial crisis low, while Lloyds has only fared marginally better.

Performance of stocks over 15yrs (share price only)

Source: FE Analytics

Yet while Ward’s focus on businesses with sustainable long-term earnings has led him to avoid many of this year’s hardest-hit sectors – which he said are likely to be victims of changing human behaviour even after the lockdown is lifted – he believes the banks are being unfairly maligned.

“I'm not hugely bullish on banks, but I think they probably represent one of the best risk/reward trade-offs in the market right now,” he said.

“Consequently, I have pretty close to the highest bank exposure in the entire sector.

“I say pretty close. I don't know what most of my competition looks like, I just know that most people don't hold banks and I have quite a lot of them.”

Many fund managers continued to steer clear of the banks following the financial crisis, not only because of the low interest-rate environment, but also due to fears their business models had been crippled by more stringent regulation.

However, Ward said the regulations themselves weren’t the problem, it was more the fact that after the five years running up to 2008 when the banks were “making too much money”, they then had to divert their profits to adjust to the new requirements.

“The delta of regulation forced them to hold increasing amounts of capital, or whatever it happened to be, and they struggled to get a footing,” he continued.

“What we ended up with was this decade-long period where banks were basically dead money. But they weren't dead money because they were broken. They were dead money because they required so much capital and there were so many regulatory headwinds.

“And then on top of that, you had governments all over the world using banks like some sort of piggybank. There was a decent consumer spending surge in the UK when PPI became a big issue.

“In the last 12 years or so, no politician has ever done badly from beating up on the banks.”

Ward said that while building these higher capital ratios hampered the banks’ ability to make money over the past decade, it also meant they were well prepared for the coronavirus crisis. As a result, he has “no doubt” they will survive, adding their businesses are the safest they have been since the 1960s.

The manager holds five banks: JP Morgan and Goldman Sachs in the US (he can hold up to 15 per cent of his portfolio outside of the UK), and Barclays, HSBC and Standard Chartered in the UK. He said each bank will react differently to macroeconomic changes, spreading the risk despite the sector concentration. Ward also believes they are much better businesses than their share prices are implying.

“There's no risk whatsoever that they have to do a capital raise, they will just continue to draw down what they have and then build it back up afterwards,” he added.

“It will mean dividend payments are not going to come back for a couple of years. But there's no reason to suggest they won't come back. And when they do come back, even at the lower end, banks such as Standard Chartered or Barclays will be making 10 per cent return on equity.

“And at the high end, which will be some of the more specialist banks, ones I don't necessarily own, but things like Close Brothers might make 18 per cent. And that's a perfectly high return. Especially considering the discount you can buy them on.”

Despite his optimism on the sector, Ward said there are a couple of headwinds. The first is obvious – the government’s policy response of making money as cheap as possible is not good for businesses that rely on the interest rate spread. However, the manager believes that even if rates remain at rock-bottom levels, the banks will eventually grow accustomed to this environment and make themselves more efficient to eke out a profit.

The second also relates to the government’s response to the crisis, but in a less obvious way.

Ward believes there has been a shift in the West away from “pure shareholder capitalism” towards “stakeholder capitalism” where there is a greater emphasis on what is best for employees and society in general. And he said the pressure from this trend is even greater when there is government involvement in a business.

“We're beginning to see amongst the less bearish banking commentators that while in 2008, the banks were the problem, in 2020 banks will probably be part of the solution.

“There is however a caveat to that: it doesn't mean to say they are going to make a load of money out of it. Because if you think of how they are being part of the solution, it's largely things like small business support loans and how that's working is the government releases capital for small businesses and it gets distributed through the banking system. Effectively it is government-backed loans that go through the banking system. The government is not going to let banks make money out of those loans, not make any real money anyway.

“So the worry on banks is that the return on capital has historically been too high, and we're going to start returning to something lower like in the 1960s or the 1970s, rather than the kind of experience equity holders had in the 80s, 90s and early 2000s.”

Data from FE Analytics shows TM CRUX UK Core has made 22.76 per cent since Ward joined in January 2016, compared with 16.81 per cent from the FTSE All Share index and 11.86 per cent from its IA UK All Companies sector.

Performance of fund vs sector and index under manager tenure

Source: FE Analytics

The £62m fund has ongoing charges of 1.01 per cent.