While there have been some clear winners during the pandemic, Blue Whale Capital’s Stephen Yiu believes it is now time to begin focusing on undervalued companies that could deliver stronger performance in the near term.

Yiu (pictured), manager of the £453m LF Blue Whale Growth fund, said that even before the crisis began he had been cautious over market valuations and had been sitting on cash in the fund.

Indeed, the fund’s cash holdings stood at more than 11 per cent of the portfolio at the beginning of February, making the fund well-placed for the March sell-off.

“The reason we were running so much cash prior to Covid was because we didn’t feel as comfortable with the valuations of the holdings,” said Yiu, an FE fundinfo Alpha Manager.

“While the likes of Amazon, Adobe and Microsoft were doing very well, they weren’t as attractive as before, so we decided to reduce our position size in those names.”

Yet, by the end of March – within six weeks – most of the cash had been deployed following one of the sharpest market downturns in living memory, according to Yiu, as he added to existing holdings.

And it paid off, as the manager’s strategy of investing in high quality businesses at the right valuation generated returns.

While LF Blue Whale Growth was down 8.02 per cent in Q1, compared with a loss of 15.38 per cent for the average IA Global fund. And in Q2, the fund made 24.79 per cent versus a 19.32 per cent gain for the sector average.

“We outperformed in both the downmarket in Q1 and market recovery in Q2,” explained Yiu.

Performance of fund vs sector YTD

Source: FE Analytics

As such, the fund is up by 17.22 per cent, year-to-date, while the peer group has managed a return of just 1.87 per cent.

However, the manager said that future performance is much less certain and as such a greater focus on valuations is warranted.

“What we cannot do is call whether the markets will go up or down from here,” he explained. “But what we can do is take a view on the valuations of our companies relative to the market.”

As such, Yiu is now focused on the companies that haven’t performed so well since the March sell-off but he believes will deliver returns in the next 12 to 18 months.

Medical equipment companies Boston Scientific and Stryker are two such examples.

The performance of these companies has been tied to the elective procedures that occur in hospitals, many of which have been postponed due to backlogs of Covid-19 patients.

“Their share prices have suffered, but we don’t believe they are structurally challenged in the same way that hotels and other luxury brands are,” said Yiu.

There have been other examples in the portfolio where share prices have suffered albeit not for structural reasons, most notably in LF Blue Whale Growth’s digital payments holdings.

“Paypal has always done well for us, whereas Mastercard and Visa haven’t done so well,” said Yiu. “They have suffered as they make money from cross-border transactions which is sustained by people going on holiday and eating out at restaurants and hotels.”

This is not to ignore the larger structural trend of digital payments in an increasingly cashless world, but their performance is contingent on possible future waves of the virus.

“It’s all about rate of change,” said Yiu. “Whatever second wave there is will be nothing like the first experience, and other future waves will continue to be lessened in their impact.”

While Yiu’s bottom-up stock picking approach means that there is less attention paid to macroeconomic events, there are some that could have an impact on the portfolio.

“Let’s say in the next 12 months, there are 10 issues that might change the directions of companies or the stock market; let’s say the [US] election, Brexit or a possible trade war,” he said. “What we [will] try to do when we invest in a company is to make sure that it’s not materially exposed to these issues.”

For example, Yiu will consider whether the earnings of the fund’s tech holdings be impacted by geopolitical or macroeconomic events over the next few years.

“Does it matter whether Trump or Biden is elected? Does it matter if there is a trade war going on between the US or China? Does it matter whether Brexit happens or the entire EU breaks up?” he asked. “It does not. It does not change the trajectory of Microsoft, Paypal and Adobe.”

He said other top-down managers might prefer to flip a coin on companies within cyclical sectors, but personally would not take that risk.

“It has served us well over the last three years to avoid the kind of uncertainties that mean we can deliver outperformance,” he said. “We like certainty and finding something that will ensure we are able to outperform.

“Anything [that’s] less certain, whether its value stocks or stocks trading at a very low price-to-earnings [P/E] ratio, or those where the outlook is unclear, why would we even bother?”

He concluded: “When you have easy companies out there and the probability of them winning is say 75-80 per cent and you have another company trading at 5x P/E and survival probability is 50/50, even without a crystal ball we would go with the more certain option.”

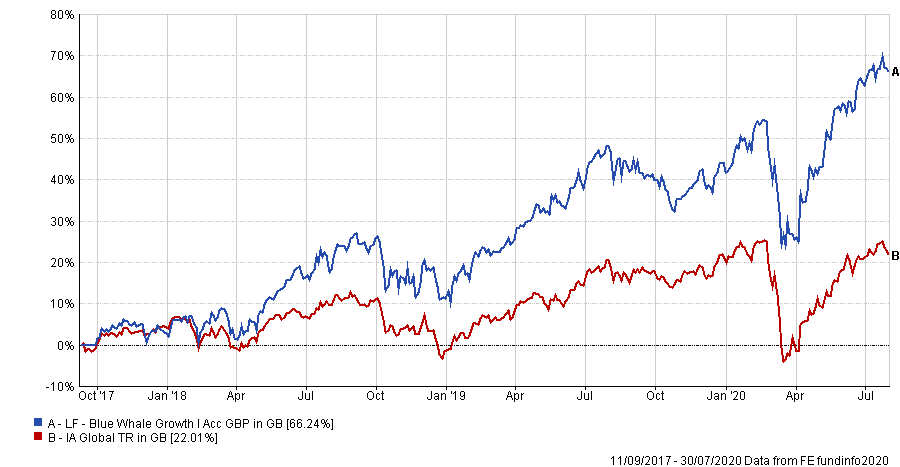

Performance of fund vs sector since launch

Source: FE Analytics

Since its launch in September 2017, LF Blue Whale Growth has returned 66.24 per cent compared to a gain of 22.01 per cent for the average IA Global peer. It has an ongoing charges figure (OCF) of 0.89 per cent.