Baillie Gifford’s Scottish Mortgage Investment Trust (SMT) could still have a place in investors’ portfolios, despite the recent headlines of clashes in the boardroom and fears over its private holdings.

Amar Bhidé, now a former non-executive director of SMT, has been outspoken in his criticism of the trust, questioning the extent of the company’s investments in unquoted businesses and publicly disagreeing with chair Fiona McBain, who has been part of the board since 2009.

McBain has since announced she will step back from her role this year, while Justin Dowley, the current senior independent director, will take over after the 2023 annual general meeting.

Baillie Gifford has also responded to criticism of SMT’s stakes in unlisted businesses via its group’s director of marketing and distribution, James Budden, who argued that it is a mistake to compare the trust’s investments with those of venture capital or private equity firms.

He said that the unquoted firms Scottish Mortgage invests in are not small, early-stage firms that need help to build up the business, but enterprises with an average size of £10bn.

Tom Slater, the manager of SMT, has also dismissed comparisons between his trust and the Woodford Equity Income fund, highlighting the differences in size and geography of the investments between the two schemes.

Recent discussions around SMT and an environment that does not favour growth investment anymore have led to it trading on a 21% discount.

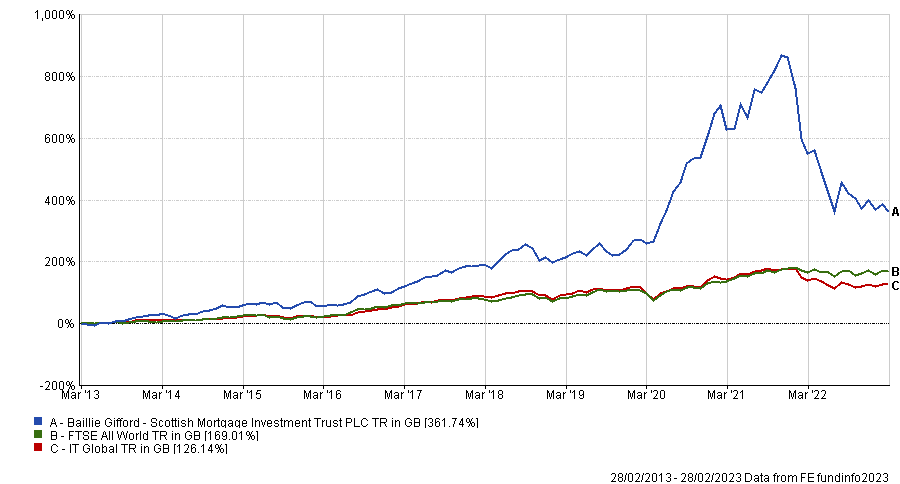

Performance of trust vs sector and benchmark over 10yrs

Source: FE Analytics

Shavar Halberstadt, equity research analyst at Winterflood, said that stakeholders are right to question the size and valuation of the private portfolio, but added that the trust’s history is in its favour.

He said: “We would posit that Baillie Gifford has set a standard for transparency in the investment trust sector regarding the frequency and methodology of private (re)valuations, and historically SMT’s private allocation has been the source of significant outperformance.

“In the medium term, a re-opening of the IPO window could assuage some concerns, as several IPO candidates in the portfolio are sufficiently large to meaningfully shift the private-public balance.”

Other were less concerned, with Sheridan Admans, head of fund selection at Tillit, calling on the trust to temporarily raise the 30% holding limit in unlisted firms.

He said: “By not allowing the managers to invest capital when companies in their portfolio undertake funding rounds risks having the trust's holdings diluted.

“It could also lead to missed growth opportunities that could benefit long-term shareholders of Scottish Mortgage.”

Overall, experts still have confidence in the managers and consider that SMT is well positioned to grow and reward long-term investors.

Dzmitry Lipski, head of funds research at interactive investor said: “The strength of their stock-picking skills combined with strong risk-adjusted performance and competitive fees make this a good choice for long-term investors.

“Managers’ expertise and their commitment to work with academia should always allow them to find modern portfolio ideas and maintain competitive edge against other players.”

Despite the recent turmoil and poor performance, DIY investors did not vote with their feet, with fund platform AJ Bell noting the trust remains popular.

Laith Khalaf, head of investment analysis at AJ Bell said: “This is a high-octane investment, and its continued popularity does suggest investors understand they have to take the very rough with the very smooth.”

The fund has generally outperformed the IT Global sector as well as the FTSE All World index, but it has been struggling since last year

Performance of trust vs sector and benchmark over 1yr

Source: FE Analytics

Although the trust is currently trading at a discount, potentially presenting a buying opportunity for a portfolio that typically trades nearer to par, Lipski warned that there could be further bumps in the road.

He said: “Investors should note that it is higher-risk investment due to high portfolio concentration, exposure to unquoted companies and exercised gearing, so works better as a satellite holding in a well-diversified portfolio.

“The style bias of the trust is toward growth, with less attention paid to valuation, meaning it can complement other funds with a core or value style orientation.”