With the performance of luxury stocks this year, investors may wonder whether luxury is the investment thematic they should have in their portfolio.

LVMH is the best illustration of the sector’s performance as this year it became the first European company to ever surpass $500bn (£404bn) in market valuation, propelling it into the top 10 of the world’s most valuable listed businesses.

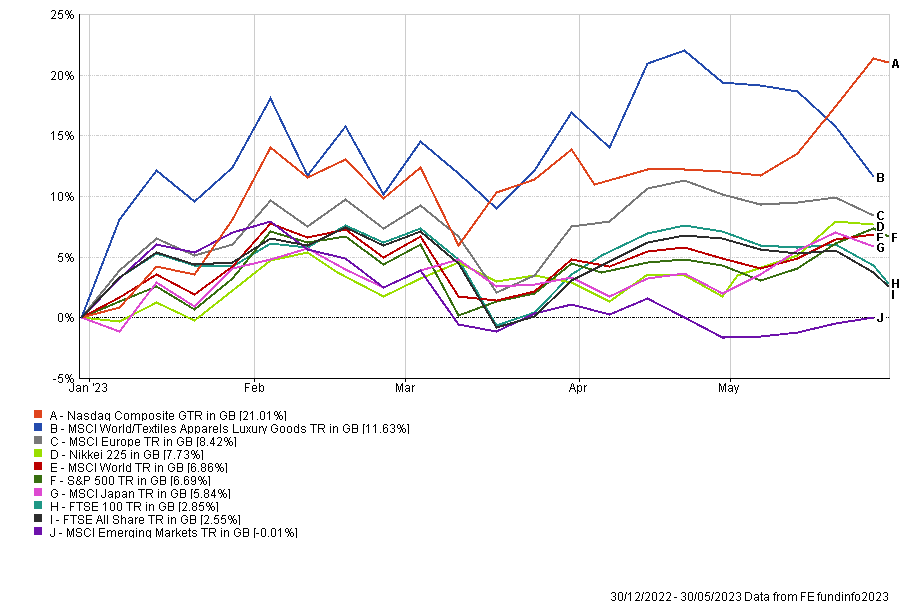

At the end of May, the MSCI World/Textiles Apparels Luxury Goods index had outperformed most of major global indices, with NASDAQ composite being the only exception.

Performance of indices since beginning of the year

Source: FE Analytics

China’s re-opening has been one of the main drivers for the luxury sector’s outperformance.

Alena Kosava, head of investment research at AJ Bell, said: “Whilst some of the macro worries are dissipating, investors remain cautious and have been hesitant to return to the country. Instead, investors have been taking an approach of allocating to China indirectly, including via luxury goods (Europe) and travel (Japan), with both equity markets outperforming year to date.”

Future prospects of the theme

While China’s re-opening has boosted the luxury sector, advocates argue it will remain a strong investment thematic over the long term with further growth thanks to the rise of the middle class in emerging markets.

Ben Yearsley, director at Fairview Investing, said: “The story isn’t about what is being bought on credit card in the UK but what the Chinese are buying. The growth in Asian and emerging markets middle class and affluent rich is what’s really driving luxury brands.

“The middle classes are estimated to grow by over 1 billion this decade with most of that growth coming in developing markets such as China.”

Beyond those growth prospects, the luxury sector can have a function in a portfolio by helping to proof it against recession. This is essentially because the consumer base is not affected by changes in the cost of living in the same way as those lower down the income scale.

Andy Merricks, fund manager at 8AM Global, said: “It is actually a play on social inequality which, as a theme, is clear and present. It is a stark fact that the world’s richest people are getting richer while the poor are getting poorer.

“The 1% wealthiest people in the world like to spend their money, and the luxury sector is a welcoming recipient for it.“

Another particularity of luxury products is that they fall into the Veblen goods category, which are goods with a status symbol appeal. Veblen goods have an upward-sloping demand curve, which means that, unlike with other goods, the demand increases as prices rise.

Moreover, luxury is a relatively narrow market with few players. Therefore, brands have a significant pricing power.

Merricks added: “Many of the biggest luxury brands are listed in Europe (predominantly in Paris) and they have been talked of as the European equivalent of the FAANGs in the S&P 500.

“Luxury brands have immense pricing power but also have fewer obvious upstart competitors than some of the technology companies past and present.”

Do you need luxury in your portfolio?

Do those positive outlooks and characteristics justify having a dedicated allocation to luxury in a portfolio? Experts offered contradicting views on it.

Some do not believe that it is an unnecessary addition because investors are likely to already have an exposure to the sector through a European or quality fund. As a result, they could be doubling up on exposure already held via more generalist funds.

Peter Sleep, senior portfolio manager at 7IM, suggested avoiding thematic investing altogether: “I think focusing trends takes investors into narrow areas like tech or narrower areas like luxury, cyber or medical cannabis.

“This means that investors are sucked into fashionable areas of the market that have already been analysed by professional investors and all you will end up with is excess volatility.”

However, Merricks said it is “increasingly difficult to ignore” the luxury sector, although this thematic might not be suitable for ethical investors.

“If you are comfortable with the underlying theme and need exposure to Europe, then it is very much worthwhile having exposure to the theme in a portfolio,” he added. “It has proven its resilience to global economic slowdown which is counter-intuitive.”

How to gain exposure to luxury

There are different ways to gain exposure to the luxury sector: directly via a thematic ETF, indirectly through a European or quality fund, or simply by buying shares of the market leaders.

For a thematic exposure to luxury, Merricks likes Amundi S&P Luxury Brands ETF, which tracks the S&P Global Luxury index. The ETF’s three largest holdings are Compagnie Financiere Richemont, LVMH and Hermes International.

For an active approach, Merricks suggested GAM Multistock – Luxury Brands Equity, which has LVMH, Hermes International and Ferrari as top holdings.

Performance of the fund vs sector and benchmark over 10yrs

Source: FE Analytics

The fund is in the top quartile in the IA Global sector over three years and one year, but has underperformed both its sector and benchmark over 10 years.

7IM’s Sleep suggested targeting Asian luxury brands specifically rather than their European counterparts.

He said: “I think new brands will emerge from Asia and they could eat into the market share of more traditional western brands. Already there are brands like Moutai (spirits) and Li-Ning (athletic shoes) in China. If new brands do emerge then an active manager may be best placed to benefit from this.”

7IM used to own Mirae Asia ESG Great Consumer Equity, which aims to achieve capital growth through investing in firms expected to benefit from growing consumption activities in Asia.

Performance of the fund vs sector and benchmark over 10yrs

Source: FE Analytics

Sleep said that the fund was severely impacted by the Chinese government actions, which has led the fund to deliver negative performance, losing 20% over three years. He added: “This is extreme but demonstrates the dangers of investing in narrow areas of the market.”

For an exposure to the luxury sector diluted in a broader fund, Yearsley suggested FTF Martin Currie European Unconstrained. “It’s got the likes of Ferrari, Moncler, and L’Oreal in the top 10 and it’s a long-term quality-growth fund.”

Performance of the fund vs sector and benchmark over 10yrs

Source: FE Analytics

Over 10 years, the fund has slightly outperformed both the IA Europe Excluding UK sector and the MSCI Europe ex UK index and has been first quartile over 5 years. The fund is having a good run this year, having been in the top 25% of the fund in its sector over six months, three months and one month.

Another example of European fund with a significant exposure to the luxury sector is BlackRock European Dynamic.

AJ Bell’s Kosava said: “BlackRock European Dynamic on our Favourite Funds list of funds has a meaningful exposure to European luxury names via LVMH and Hermes International, together accounting for c.12% of the overall portfolio.”

Performance of the fund vs sector and benchmark over 10yrs

Source: FE Analytics

Except over three months, the fund has been a regular top quartile fund in the IA Europe Excluding UK sector.

Yet, some investors might prefer to buy shares of luxury company instead. After all, why buy a Louis Vuitton bag when you could own LVMH instead?

Zhixin Shu, senior equity analyst at J. Stern & Co. World Stars Global Equity fund, likes LVMH and Hermes.

Stock performance YTD

Source: Google Finance

She said: “A rising tide lifts all boats, macroeconomic factors will drive the sector higher, but when the tide turns, only the strongest have plain sailing.”

Stock performance YTD

Source: Google Finance

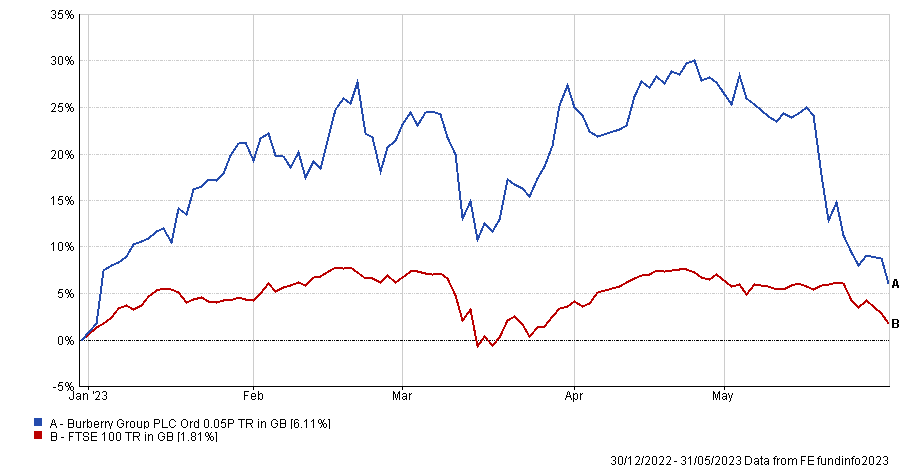

Chris Beauchamp, chief market analyst at IG Group, added Burberry to the list, although the British luxury fashion house has not experienced the same level of performance as its continental peers so far this year.

Stock performance vs index YTD

Source: Google Finance